Is the Federal Reserve Rate Outlook turning hawkish again as sticky inflation tests Kevin Warsh’s first week in charge?

What Did Kevin Warsh’s First Full Week as Fed Chair Signal?

This week marked the first full trading week under Fed Chair Kevin Warsh’s formal leadership — and it delivered a unified, unambiguous message: patience has limits. Warsh, who resigned from the Fed board during Bernanke’s QE era to protest prolonged liquidity expansion, declined to submit his own dot plot projection, reinforcing his preference for flexibility over rigid forward guidance. His stance — echoed by Governor Christopher Waller’s declaration that the Fed “will not keep rates down just to help the government finance its deficits” — crystallized a decisive break from recent accommodative rhetoric. Analysts at Citigroup noted Warsh’s “institutional credibility on inflation control” and raised their 2026 hike probability from 45% to 72%, while RBC Capital Markets upgraded its year-end federal funds forecast to 4.00–4.25% — implying two 25-basis-point hikes.

How Did Inflation Data Reshape the Federal Reserve Rate Outlook?

May’s 4.2% headline CPI — the highest since April 2023 — and Core CPI’s jump to 2.9% (a 10-month high) were the week’s dominant catalysts. Crucially, Core PCE — the Fed’s preferred gauge — rose to 3.4%, its highest reading since October 2023 and the 63rd consecutive print above target. Bloomberg’s analysis emphasized that “services inflation remains sticky,” with housing and insurance costs proving resistant to cooling. Bank of America responded by shifting its baseline forecast from one to two rate hikes, citing “the structural persistence of labor-driven service costs.” The Cleveland Fed’s Inflation Nowcasting tool projected only modest softening — to 3.49% by July — underscoring why markets now assign 68% odds to at least one hike before December, per CME FedWatch data.

Why Did the FOMC Minutes Trigger a ‘Neutral Pause’ Narrative?

The release of the June FOMC minutes midweek introduced a subtle but critical nuance: while the committee acknowledged “elevated inflation risks,” it also described its stance as “a neutral, wait-and-see posture.” This duality — hawkish data paired with dovish language — created short-term volatility in Treasury yields, with the 2-year rising 12 bps to 4.20% and the 10-year stabilizing at 4.50%. UBS interpreted the minutes as “deliberate ambiguity,” designed to avoid overcommitting before July’s PCE report. The firm warned investors not to mistake “pause” for “pivot,” noting that Warsh’s task forces on communication strategy and alternative inflation measures signal structural reform — not dovish retreat.

What Role Did Geopolitics and Fiscal Policy Play?

The Iran war’s secondary inflationary effects re-emerged as a critical theme. Though oil prices have retreated, the Strait of Hormuz disruption continues to ripple through insurance, shipping, and industrial input costs — a dynamic Jay Hatfield labeled “Trumpflation 2.0.” With $39.4 trillion in national debt and rising debt-service costs, President Trump’s public pressure for 1% rates collided head-on with Waller’s independence doctrine. Analysts at Morgan Stanley observed that “fiscal dominance is now the Fed’s most acute political risk” — and Warsh’s balance-sheet reduction plan (targeting pre-pandemic $3.5 trillion levels from $6.1 trillion today) is designed to insulate monetary policy from fiscal leakage. That effort, however, faces headwinds: the Fed’s interest-on-reserves mechanism tightly links the balance sheet to the funds rate — making orderly shrinkage contingent on higher rates, not lower ones.

What to Watch Next Week: PCE, Senate Return, and AI Task Force Updates

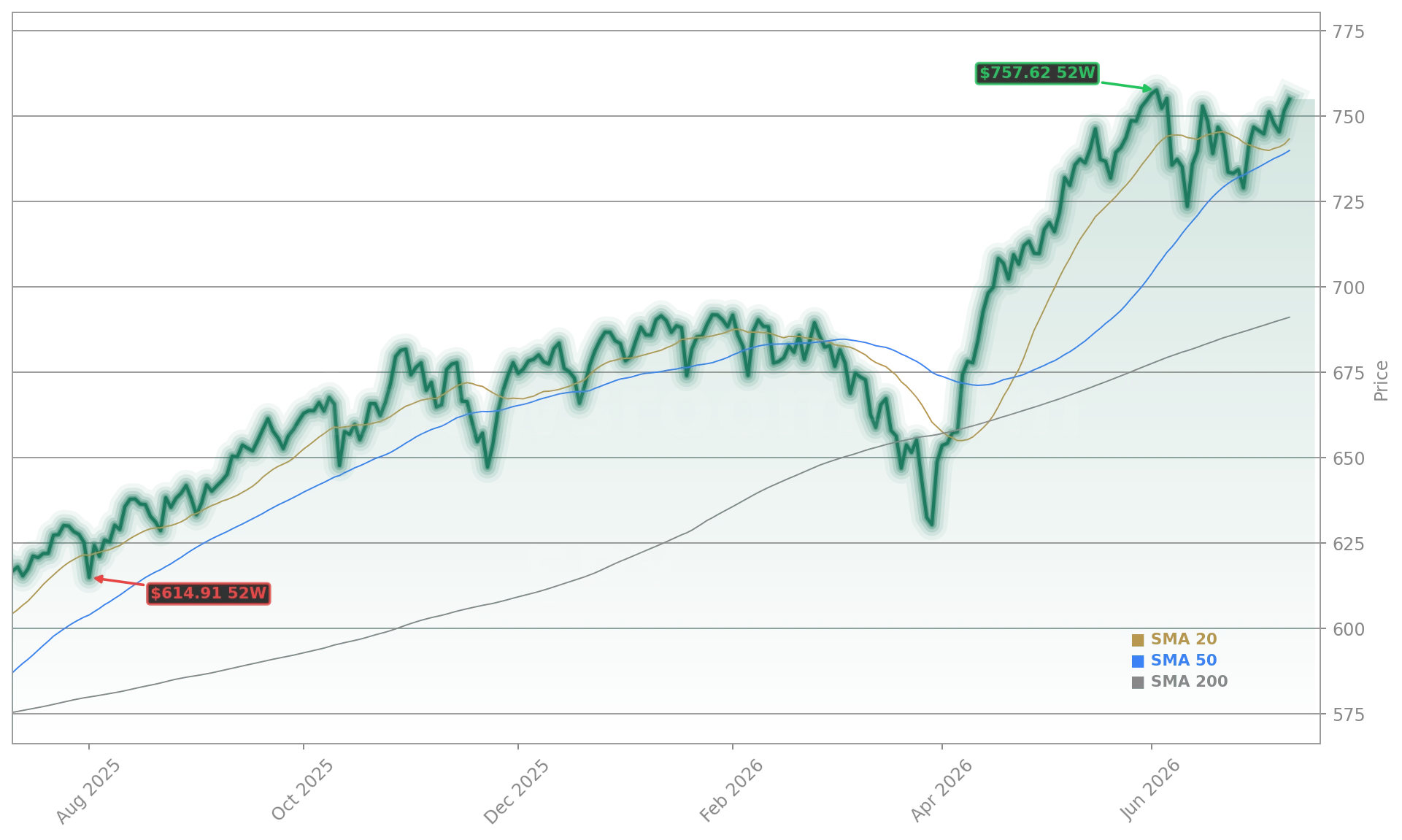

Next week brings three pivotal catalysts. First, the June Core PCE report — expected Friday — could confirm whether inflation is peaking or re-accelerating; consensus forecasts a 0.3% monthly rise, keeping the annual rate at 3.4%. Second, the Senate returns from recess on Monday, July 13, with the CLARITY Act’s fate now hanging in the balance — though analysts at Kalshi assign just a 25% chance of passage before the August recess. Third, Warsh’s AI task force — co-chaired by Nobel laureate Robert Shiller and Greg Mankiw — is expected to release preliminary findings on AI’s disinflationary potential, a theme increasingly cited by Goldman Sachs and BlackRock as a counterweight to near-term wage pressures. With the SPDR S&P 500 ETF (SPY) up 0.45% on the week and NVIDIA, Apple, and Tesla all rallying on AI optimism, the interplay between tech-driven productivity and Fed policy will define the next phase of the Federal Reserve Rate Outlook.

We are not going to keep rates down just to help the government finance its deficits… Monetary policy must remain independent, focused on our economic objectives.— Christopher Waller, Federal Reserve Governor

This week reaffirmed that the Federal Reserve Rate Outlook is no longer about timing — it’s about conviction. Warsh’s leadership, coupled with stubborn inflation and geopolitical strain, has shifted the baseline from rate cuts to hikes. For investors, the message is clear: position for higher-for-longer, prioritize quality and cash flow, and treat every PCE print as a potential pivot point. The era of easy money is over — and the Federal Reserve is now the undisputed anchor of market discipline.