Can the S&P 500 keep climbing as AI leadership wobbles and oil shocks return to the inflation debate?

What drove SPY’s +0.8% weekly gain?

This week’s S&P 500 Weekly Recap is defined by three converging forces: a sharp rotation out of AI hardware names following Samsung’s underwhelming earnings reaction, renewed U.S.-Iran hostilities that spiked oil prices and reignited inflation concerns, and a wave of bullish analyst upgrades—most notably Morgan Stanley’s $300 price target on SpaceX and Trivariate’s 8,000-point S&P 500 forecast. While the week opened with optimism—President Trump’s ‘Trump Accounts’ launch and strong memory-stock rebounds—the narrative shifted decisively on Tuesday after Samsung reported record earnings yet saw its shares plunge 7%, dragging Micron, Sandisk, and Western Digital lower. That triggered a broader chip-sector selloff, with the VanEck Vectors Semiconductor ETF falling 12% over the prior three days. The pivot accelerated Wednesday when Trump declared the U.S.-Iran ceasefire ‘over,’ sending WTI crude soaring to $74.10 and pushing the 10-year Treasury yield to 4.57%. Yet SPY held firm—rising 0.8% for the week—thanks to resilience in defensive sectors (Eli Lilly, Johnson & Johnson), a Thursday rebound in semiconductors (Arm +11%, ASML +3%), and strong breadth in the Russell 2000 (+0.27%).

Price action over the week

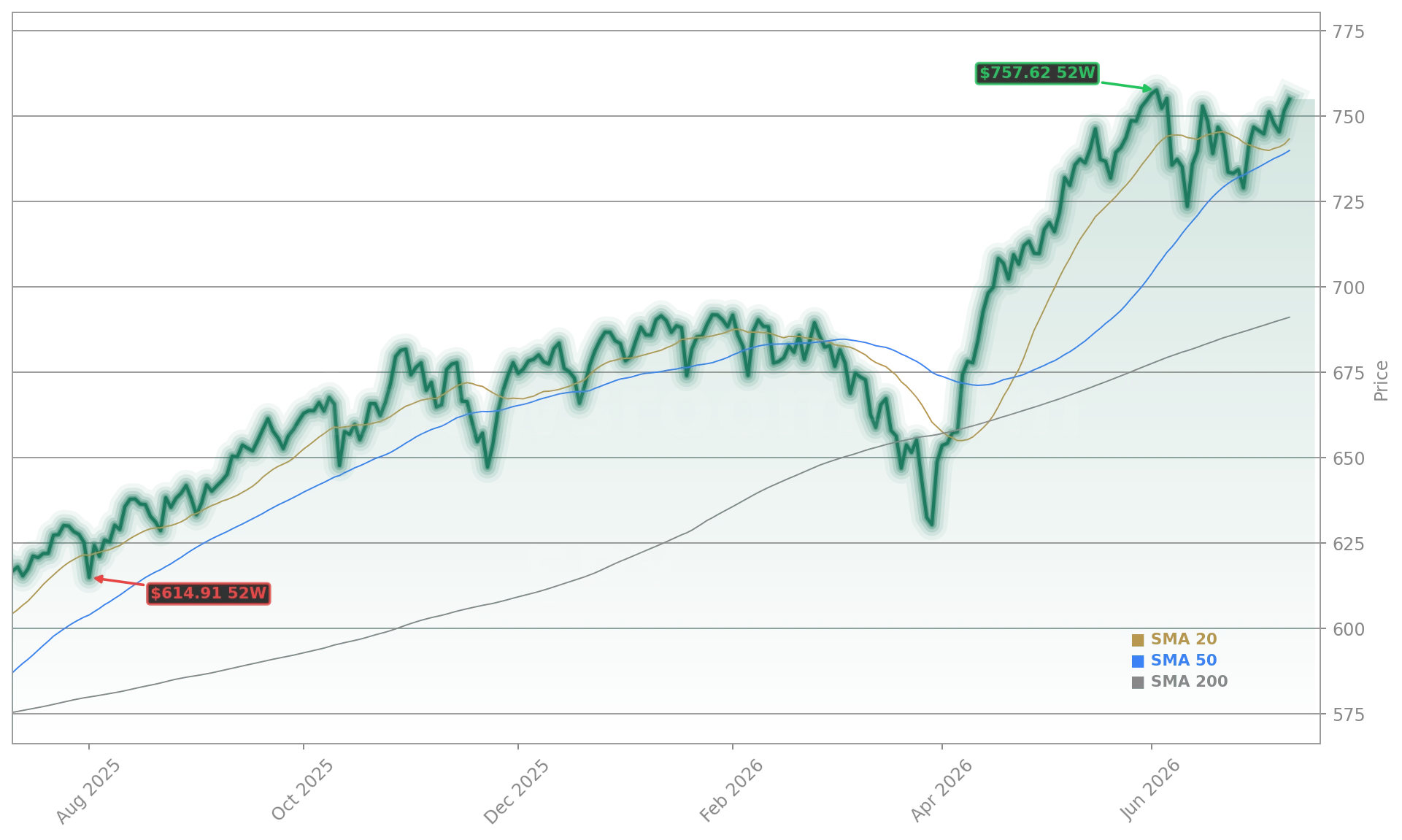

SPY delivered a +0.8% weekly performance, rising from Monday’s open of $748.74 to Friday’s close of $754.95. The weekly high was $755.42 and the weekly low $739.51. This was a low-volatility, range-bound week—no daily move exceeded 3%, and no single day stood out as an outlier. Instead, the index traced a steady upward arc: early gains on Monday’s bullish sentiment, modest pullbacks Tuesday and Wednesday amid chip and geopolitical stress, then a decisive Thursday–Friday rebound as memory stocks rallied (Micron +5% premarket Thursday) and oil eased. The trajectory reflects market discipline: absorbing shocks without capitulation, and using volatility to reposition—not retreat. SPY’s ability to hold above its 50-day moving average and close within 0.7% of its 52-week high ($760.40) signals underlying strength.

What do analysts say about the S&P 500 Weekly Recap?

Trivariate Research raised its S&P 500 target to 8,492 points, citing $386 EPS and a 22x P/E ratio driven by AI infrastructure demand—especially for memory chips. Citigroup reinforced that thesis, projecting the server CPU market to reach $132 billion by 2030 and highlighting AMD’s accelerating share gains. Meanwhile, Morgan Stanley upgraded SpaceX to overweight with a $300 price target, Goldman Sachs set $205, and UBS issued a $210 target—validating the stock’s inclusion in the Nasdaq-100. On the bearish side, Seeking Alpha cautioned that much of the S&P 500’s 27% 2026 earnings growth is an ‘illusion’ driven by intra-index spending and accounting, not organic profit expansion. Barron’s and Benzinga echoed concerns about concentration risk, noting the top 10 S&P 500 companies now account for 43% of the index’s market cap—up from 27% a decade ago.

What matters next week for SPY?

Three catalysts dominate next week’s watchlist: Delta Air Lines’ Friday earnings (a key barometer for consumer and travel resilience), Taiwan Semiconductor’s June sales release (a proxy for AI chip demand), and the Federal Reserve’s June meeting minutes—though new Fed Chair Kevin Warsh is expected to issue a ‘much-abridged’ summary, offering minimal policy guidance. Also critical: SK Hynix’s Nasdaq debut on Friday, which Benzinga flagged as a potential ‘make-or-break’ moment for semiconductor sentiment. If SK Hynix trades strongly, it could close the valuation gap with Micron and reignite the AI hardware rally. If it underperforms, SPY may test support near $748. Analysts at Yardeni Research view recent semiconductor weakness as a ‘buying opportunity,’ while BlackRock warns that index-only strategies are breaking down amid geopolitical volatility and market concentration—urging investors to add private markets and annuities to retirement portfolios.

How did AI leaders perform in this S&P 500 Weekly Recap?

AI’s leadership remained bifurcated. NVIDIA fell 2% on Tuesday but rebounded 3.65% on Thursday after Beijing approved limited H200 chip sales. Apple rose 0.7% Tuesday and gained 8.8% for the prior week, regaining key moving averages. Tesla slid 3% Thursday amid Rivian’s 15% plunge and broader EV sector pressure. Meanwhile, Dell (+5.5% Thursday) and Arm (+11%) emerged as new AI infrastructure leaders—both clearing multi-week buy points. The contrast underscores the S&P 500 Weekly Recap’s central theme: investors are no longer buying ‘AI’ as a monolith—they’re selecting specific enablers (memory, interconnects, power) while rotating away from overextended end-device names.

Related Coverage: The S&P 500 Weekly Recap: Micron’s $50B Shock and Fed Pivot explores how Samsung’s earnings reset memory valuations—and whether the Fed’s next move will validate or derail the AI trade. For deeper semiconductor context, the Nasdaq 100 Semiconductor Selloff: QQQ Falls 1.6% on Chip Rout analyzes whether this correction is a healthy reset or the first crack in tech’s foundation.

There needs to be an evolution away from this being indexed only. The markets are evolving to a point where there needs to be more oversight.— Nick Nefouse, BlackRock

This week’s S&P 500 Weekly Recap reaffirms that volatility is not the enemy—it’s the market’s mechanism for price discovery. SPY’s +0.8% gain wasn’t passive; it was earned through selective rotation, disciplined risk management, and conviction in AI’s structural tailwinds. For investors, the takeaway is clear: stay anchored to fundamentals, use pullbacks to add to high-conviction enablers like Micron and Arm, and treat geopolitical noise as a timing tool—not a strategic threat. The path to 8,000 points is open. The S&P 500 Weekly Recap shows the market is already walking it.