Can FedEx Earnings support this stock rebound, or will margin pressure keep overshadowing the company’s strategic reset?

Why Did FedEx Earnings Trigger a Selloff?

FedEx Corporation’s Q2 2026 results were a study in contradiction: robust top- and bottom-line performance overshadowed by deteriorating profitability. Operating margin fell to 8.4% — 25 basis points below consensus — with the FedEx Express segment dropping to 7.7%, down from 8.5% a year earlier. Analysts at Wells Fargo noted that rising employee compensation, outsourced transportation costs, and fuel expenses were primary drivers. While revenue rose 13% year-over-year and EPS beat by 5.7%, the margin miss became the dominant narrative — especially as investors weigh FedEx’s transformation against peers like UPS and NVIDIA-fueled logistics demand in data centers and healthcare verticals.

How Does the FedEx Freight Spin-Off Reshape the Story?

With FedEx Freight officially spun off on June 1, 2026, FedEx Corporation’s Q2 report marked its first as a streamlined entity focused on express, ground, and global logistics — not trucking. The $4.1 billion cash dividend from FedEx Freight provided immediate balance sheet flexibility, directly funding a $4.15 billion debt tender announced the same day. That tender targets 19 bond series, including long-dated maturities through 2065. Citigroup Global Markets Inc., J.P. Morgan Securities LLC, and Goldman Sachs & Co. LLC serve as Lead Dealer Managers. The move signals capital discipline, but also reflects a strategic pivot: shedding lower-margin assets to sharpen focus on high-value verticals like aerospace, automotive, and refrigerated healthcare logistics — sectors where Tesla and Apple supply chains increasingly demand precision timing and temperature control.

What’s the Outlook for FedEx Earnings and Guidance?

FedEx Corporation raised its full-year EPS guidance to $16.90–$18.10, citing improved pricing power and demand resilience — particularly in international healthcare and data center logistics. Yet the guidance shift coincides with a fiscal-year realignment, moving from a May-year-end calendar to a December-year-end, effective immediately. That change — highlighted by UBS as a cash flow and profitability enhancer — muddied year-over-year comparisons and contributed to investor uncertainty. Stiefel lowered its price target to $326 from $442 but reaffirmed its Buy rating, stating the results ‘underscore the success in their transformation strategy.’ Similarly, Wells Fargo maintained its Overweight rating and $425 price target, arguing ‘stronger profitability will outweigh softer FedEx Ground results.’

How Are Analysts Reacting to FedEx Earnings?

Despite downward revisions to price targets, analyst sentiment remains broadly constructive. UBS cut its target to $350 from $445 but retained a Buy rating. TD Cowen reduced its target to $354 (from $426), still implying 14% upside from current levels. Bank of America holds a Buy rating with a $378 target. Crucially, none of these firms downgraded the stock — a sign Wall Street views the margin pressure as transitional, not structural. As one analyst observed on Schwab Network, ‘The demand side is strong. You need revenue to produce — and that’s solid.’ That demand strength is increasingly tied to AI infrastructure buildouts: server shipments, data center expansions, and aerospace component logistics — all high-margin, high-stakes segments where FedEx Corporation is gaining traction alongside peers like Caterpillar and Meta-linked supply chains.

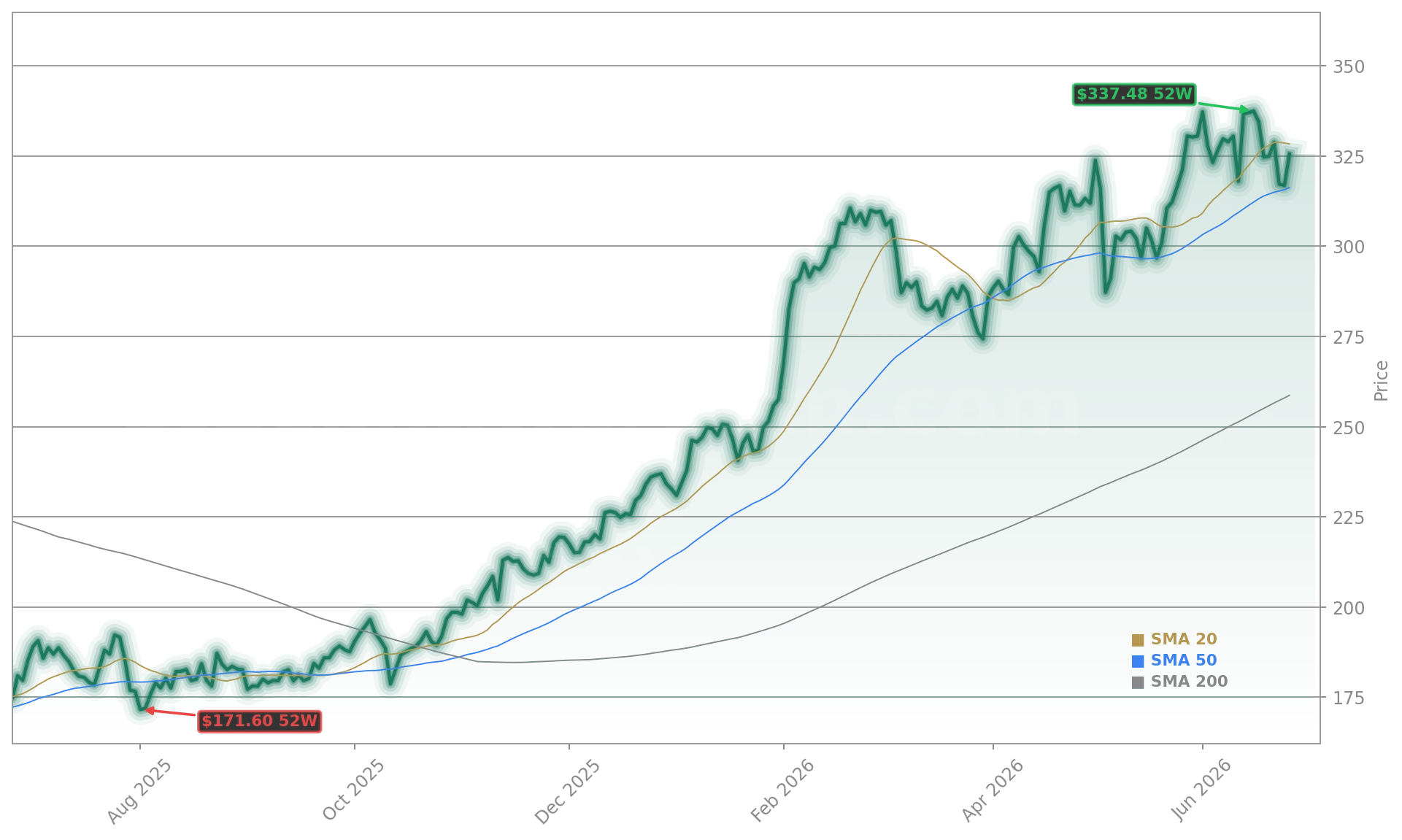

What’s Next for FedEx Corporation’s Stock?

Technically, FedEx Corporation’s stock faces a critical test near $305 — the 50% Fibonacci retracement level between its April low ($194) and May high ($413). Traders like Scott Bauer of Prosper Trading Academy see that zone as a high-conviction entry point for long positions, citing risk-defined options strategies. Meanwhile, the $4.15 billion tender — funded by FedEx Freight’s dividend — reduces long-term debt burden and improves interest coverage, supporting future margin recovery. With the S&P 500 up 23% over the past year and FedEx Corporation up 70%, the stock remains a relative outperformer — but now under pressure to prove its profitability narrative can keep pace with its growth story.

Related Coverage: For deeper analysis of how FedEx Earnings signaled both strength and structural concern, see FedEx Earnings -6.7% After Q4 Beat and Guidance Cut. On the broader industrial and AI infrastructure front, Caterpillar Record +3% as AI Power Demand Lifts CAT reveals how power infrastructure demand is reshaping traditional industrial leaders — a trend FedEx Corporation is leveraging in data center logistics.

The demand side of it is strong. And at the end of the day, you need revenue if you’re going to produce, right? And so the demand side of it is strong.— Marley Caden

FedEx Corporation’s transformation is delivering results — just not yet in margins. For investors, the path forward hinges on execution in high-value verticals and disciplined capital allocation. The next quarterly earnings will show whether the pivot is truly accelerating. For long-term portfolios exposed to AI infrastructure and healthcare logistics, FedEx Corporation remains a strategically positioned, fundamentally sound holding.