Can Lucid’s new CEO turn an $800 million lifeline into a real turnaround, or is Wall Street just pricing in delay?

What triggered the Lucid CEO Change?

After six consecutive quarters of negative gross margins and declining vehicle utilization rates, Lucid Group, Inc. announced a full executive reset in late June 2026. Founder and former CEO Peter Rawlinson stepped aside, and former Rivian executive David G. P. Smith assumed the role effective July 1. Smith, who previously led Rivian’s manufacturing and supply chain operations, inherits a company with $1.2 billion in cash but $2.8 billion in long-term debt. According to Bloomberg, Smith’s mandate is clear: stabilize production, reduce burn rate, and align product roadmap with near-term capital constraints — not aspirational range records. The board cited ‘execution gaps against strategic milestones’ as the primary catalyst for the Lucid CEO Change.

Why did Lucid scrap its 2026 production forecast?

Lucid Group, Inc. withdrew its full-year production guidance — previously set at 18,000–22,000 units — after Q1 deliveries fell 27% short of internal targets and factory utilization dropped to 41%. The company attributed the shortfall to battery supply bottlenecks, software validation delays for its Gravity SUV, and lower-than-expected dealer channel absorption. Notably, only 3,819 of the 4,774 vehicles built in Q1 were sold — a 20% inventory buildup that strained working capital. For context, Tesla delivered 451,758 vehicles in the same quarter, while NVIDIA-powered ADAS adoption continues accelerating across legacy OEMs like Ford and GM — further widening the technology and scale gap.

How are analysts reacting to the Lucid CEO Change?

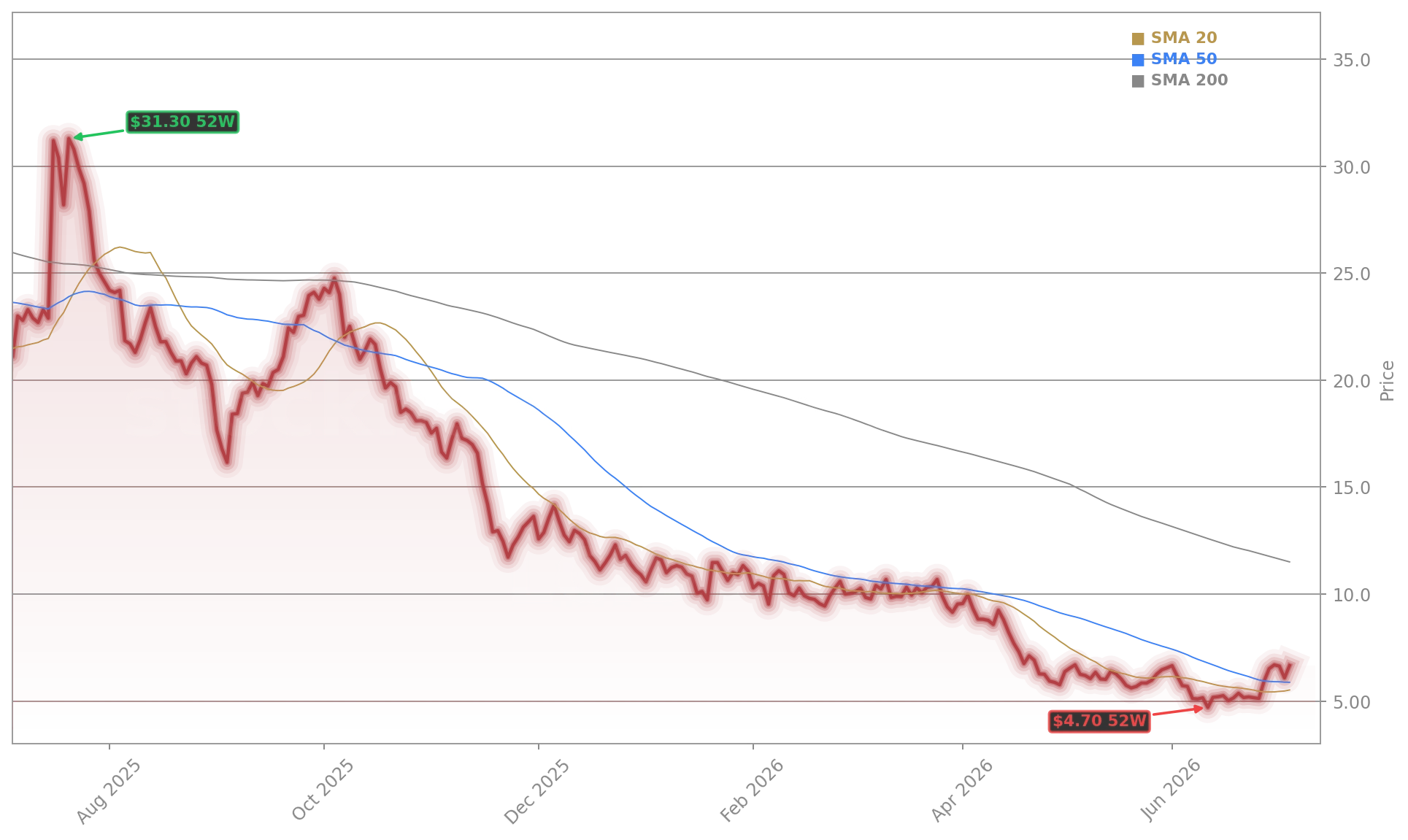

RBC Capital Markets downgraded Lucid Group, Inc. to ‘Underperform’ with a $4.25 price target, citing ‘unproven turnaround credibility’ and ‘no near-term path to gross margin breakeven.’ Citigroup maintained a ‘Neutral’ rating but slashed its 2026 revenue forecast by 38%, now expecting just $312 million — well below the $540 million implied by prior production guidance. ‘This isn’t just a leadership refresh — it’s a recognition that Lucid’s capital-light EV startup model has failed,’ wrote Citigroup analyst Itay Michaeli. Goldman Sachs reiterated its ‘Sell’ rating, warning that ‘even with $800 million in new financing, LCID’s cash runway extends only to Q1 2027 under current burn assumptions.’

Does the $800M financing buy enough time?

Yes — but only for survival, not scale. The $800 million convertible note offering, priced at a 30% premium to LCID’s 20-day VWAP, closed on July 5. While the capital infusion lifted shares 9.21% to $6.64 in pre-market trading, it comes with steep terms: 8.5% coupon, mandatory conversion by 2029, and warrants exercisable at $9.20. More critically, the proceeds are earmarked for ‘manufacturing efficiency initiatives and working capital optimization’ — not new model launches or R&D expansion. That signals a strategic pivot from growth-at-all-costs to capital discipline — a stark contrast to the playbook used by Apple-backed EV startups or legacy automakers investing billions in software-defined vehicles.

What’s next for Lucid Group, Inc. on Wall Street?

Investors now await Smith’s first investor call on July 15, where he’s expected to outline revised 2026 delivery targets, gross margin timelines, and potential asset-light partnerships. The S&P 500’s broader EV sentiment remains fragile: the SPDR S&P 500 Electric Vehicle ETF (DRIV) is down 14% year-to-date, and NASDAQ’s EV sub-index has underperformed the broader tech index by 22 percentage points. With LCID trading at just 0.3x forward sales — versus Tesla’s 3.8x — valuation isn’t the issue. Execution is. The Lucid CEO Change is the first step — but without demonstrable Q3 delivery improvement and gross margin expansion, Wall Street will likely treat the $800 million as a delay, not a solution.

This isn’t just a leadership refresh — it’s a recognition that Lucid’s capital-light EV startup model has failed.— Itay Michaeli, Citigroup analyst

Related Coverage: Can Lucid Financing buy enough time for a real turnaround, or is Wall Street just cheering another expensive lifeline? Lucid Financing $800M Sends LCID Stock Soaring 9.2%. The draw reflects our disciplined capital strategy — as noted by Maik Kemper, Editor in Chief.