Can Marvell AI Strategy turn custom silicon and AI networking into the next must-own data center growth story?

What’s Driving Marvell’s AI Infrastructure Momentum?

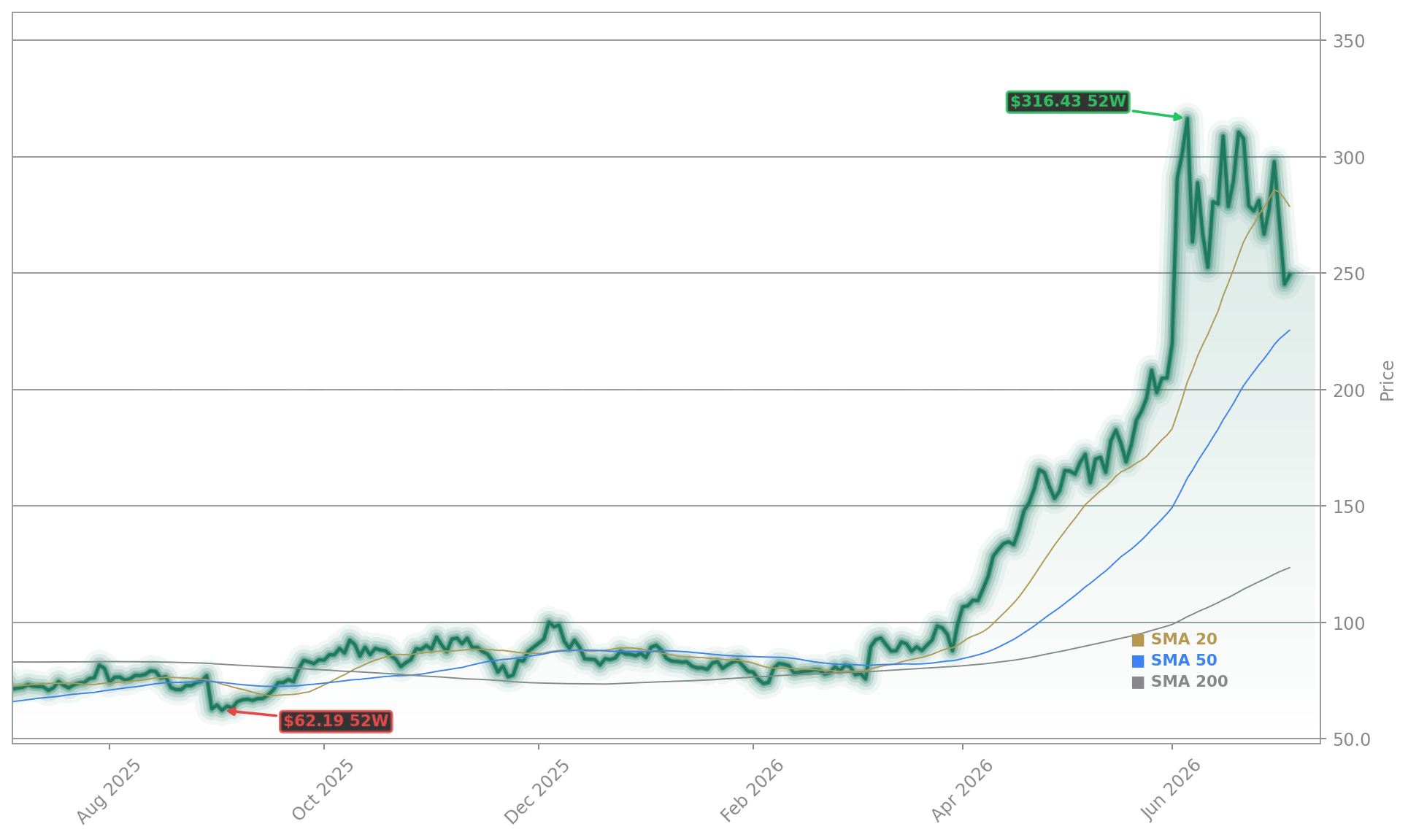

Marvell Technology, Inc. isn’t chasing AI—it’s building the plumbing. While NVIDIA delivers the compute engines, Marvell supplies the high-speed optical interconnects, DPUs, and custom silicon that move exabytes of data between GPUs at sub-microsecond latency. That distinction has propelled MRVL to a 250% gain over the past 12 months—and a 3.39% jump on July 6 alone, as reported by TradingKey, citing production delays in competing AI chip architectures that are widening Marvell’s window for custom silicon adoption. UBS analyst Timothy Arcuri just raised the price target to $340—up from $230—citing the Teralynx T100, a 102.4 Tbps switch silicon engineered specifically for AI cluster scaling. That chip cuts power consumption by 35% and latency by 40% versus prior-gen solutions, directly addressing the thermal and bandwidth bottlenecks that constrain next-gen LLM training.

How Does Marvell AI Strategy Compare to Broadcom and Intel?

Marvell Technology, Inc. is quietly closing the valuation and execution gap with Broadcom—long the gold standard in custom data center silicon. While Broadcom leans heavily on its VMware and mainframe legacy, Marvell’s AI strategy is purpose-built: 82% of its Q1 2027 revenue now flows from data center infrastructure, versus just 12% from legacy mobile and IoT. In contrast, Intel (INTC) continues to grapple with foundry delays and AI chip ramp uncertainty, and its Gaudi 3 adoption remains narrow. Meanwhile, Marvell’s NVLink integration with NVIDIA—including co-developed silicon photonics—positions it as a core enabler in NVIDIA’s AI stack, not just a peripheral supplier. Cantor Fitzgerald recently upgraded MRVL to $300 with a ‘Neutral’ rating, while Stifel lifted its target to $350 on ‘Buy’, citing ‘multi-year visibility into AI infrastructure capex cycles.’

Who’s Buying—and Who’s Selling—Marvell Shares?

Institutional conviction is intensifying. Tensor Edge Capital LLC just acquired 515,400 shares—valued at $51.1 million—making MRVL its fourth-largest holding. PFG Investments LLC and QRG Capital Management both increased stakes by over 23% in Q1. Yet insider activity shows complexity: CEO Matthew J. Murphy and COO Chris Koopmans collectively sold $26.8 million in shares over 90 days. That divergence reflects confidence in long-term execution—not short-term price timing. With 83.51% institutional ownership and a ‘Moderate Buy’ consensus from 22 analysts (per MarketBeat), the stock trades at 19x forward sales and 50x adjusted EBITDA—but analysts project 41% CAGR revenue growth from fiscal 2026 to fiscal 2029. That justifies the multiple, especially as AI data center capex is forecast to grow 27% annually through 2029.

What’s Next for Marvell AI Strategy in Q2 2026?

Q2 2026 earnings—due in early August—will test whether Marvell’s AI strategy is scaling beyond design wins into revenue execution. Guidance issued in May pointed to sequential growth of 8–10%, driven by Teralynx ramp, DPU deployments at Tier-1 cloud providers, and optical interconnect orders from AI chipmakers beyond NVIDIA. The company also raised its quarterly dividend to $0.06—a signal of cash flow durability. With NVIDIA’s $2 billion strategic investment now fully operational and NVLink-CX integration accelerating, Marvell’s role is no longer ‘enabling’—it’s indispensable. As one Wall Street strategist put it: ‘If AI is the new electricity, Marvell is building the grid.’

Related Coverage: Can Marvell AI Infrastructure turn networking hardware into the real power center of the AI boom? Marvell AI Infrastructure +50% Surge in Data Center Growth explores how Jensen Huang’s endorsement—and Meta’s multi-year procurement—signals a structural shift in AI hardware hierarchy.

If AI is the new electricity, Marvell is building the grid.— Wall Street strategist

Marvell Technology, Inc. remains the most underappreciated AI infrastructure play on Wall Street—not because it’s small, but because its impact is invisible until it’s missing. Its Marvell AI Strategy has moved decisively beyond theory into revenue-generating execution, with Q2 2026 poised to confirm durability. For investors seeking exposure to AI’s physical layer—not just its algorithms—Marvell Technology, Inc. is no longer optional. The next quarterly earnings will show whether the trend continues—and whether the $340 UBS target becomes a floor, not a ceiling.