Will Marvell S&P 500 Inclusion unlock lasting institutional demand, or is the stock already priced for perfection?

What Does Marvell S&P 500 Inclusion Mean for Index Investors?

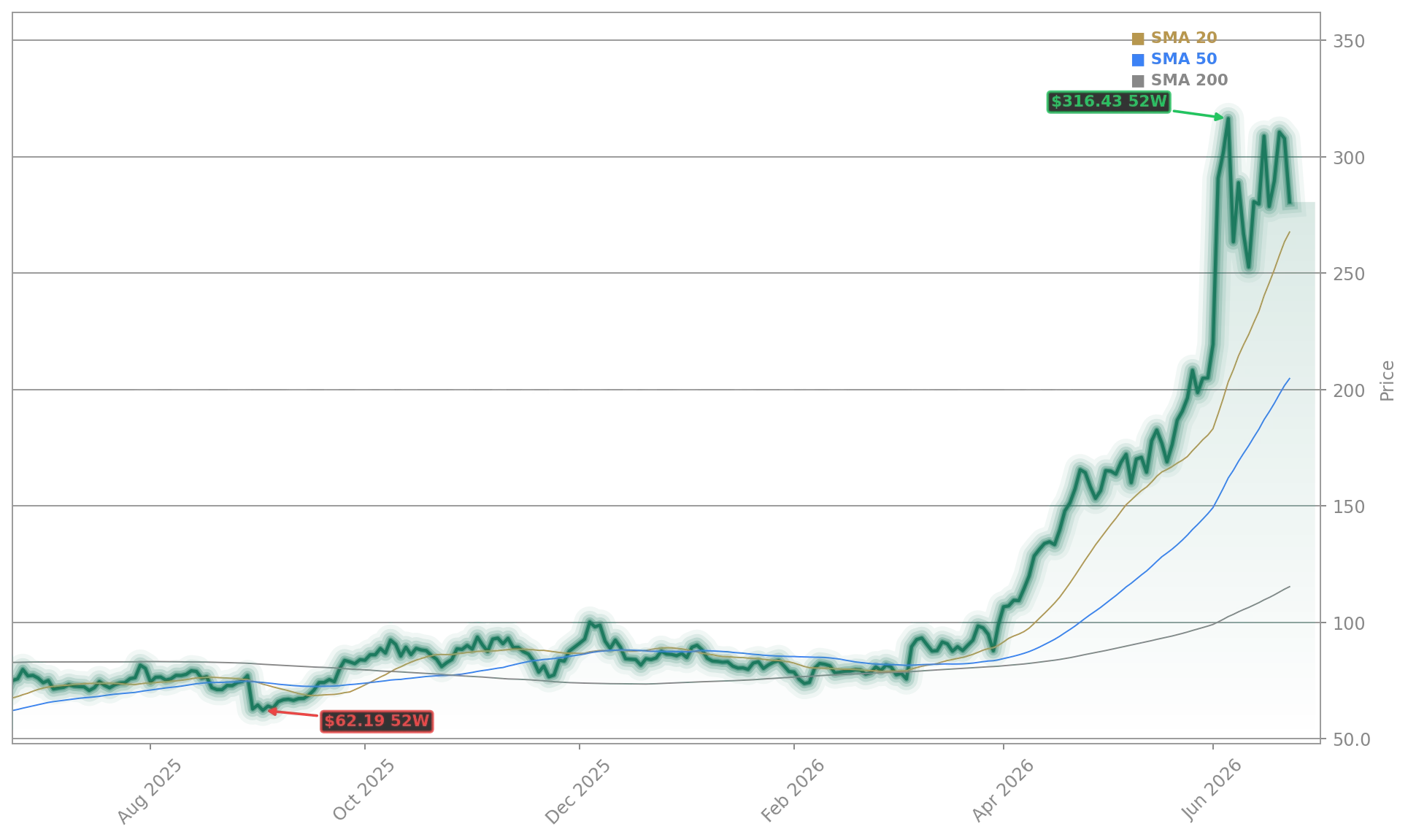

Effective before market open on Tuesday, June 23, 2026, Marvell Technology, Inc. officially enters the S&P 500 — the most widely tracked U.S. equity benchmark. This Marvell S&P 500 Inclusion triggers automatic rebalancing across trillions in passive assets, including SPDR S&P 500 ETF (SPY) and Vanguard 500 Index Fund (VFIAX). Unlike sector-specific ETFs, S&P 500 mandates force broad institutional adoption — a tailwind that historically adds 2–4% in incremental buying pressure over the first 10 trading days. With Marvell’s market cap now near $272 billion, the inclusion ranks among the largest S&P 500 additions of 2026, underscoring how deeply AI infrastructure has reshaped Wall Street’s valuation hierarchy.

Why Is Marvell Outpacing Traditional Semiconductor Peers?

While NVIDIA and Broadcom dominate headlines, Marvell Technology, Inc. is capturing disproportionate growth in two mission-critical AI infrastructure layers: optical interconnects and custom AI accelerators. Goldman Sachs projects the optical networking market will grow ninefold to $154 billion by 2033 — and Marvell is now the only pure-play supplier with silicon photonics, DSPs for 800G/1.6T transceivers, and its newly launched 102.4 Tbps Teralynx switch. Crucially, its custom chip business — powering Amazon’s Trainium and Microsoft’s Maia — is expected to nearly triple revenue from FY2027 to FY2029, reaching over $10 billion. That durability separates it from cyclical memory players like Micron and provides a structural edge over more diversified peers.

How Are Analysts Pricing Marvell’s AI Infrastructure Edge?

KeyBanc lifted its price target on Marvell Technology, Inc. to $385 from $260 — a 48% increase — citing heightened conviction in scale-up data center networking, the Celestial AI acquisition, and silicon photonics differentiation. B. Riley followed with a $345 target and Buy rating, while Oppenheimer raised its target to $250 and reiterated Outperform, citing ‘upside in AI ASIC bookings and interconnect strength.’ Notably, all three firms emphasize optical networking as the more durable growth vector versus custom XPUs — a view reinforced by Marvell’s 70% interconnect revenue growth forecast for fiscal 2027. With a forward P/E near 50 and P/S of 31, valuation remains aggressive — but analysts argue it’s justified by 41% revenue CAGR through FY2029 and near-zero exposure to consumer or mobile end markets.

What’s Driving the Surge — Hype or Hard Fundamentals?

We are seeing exceptional AI-related bookings, and as a result, we are significantly raising Marvell’s revenue outlook for both fiscal 2027 and fiscal 2028 compared with the guidance we provided last quarter.— Matt Murphy, CEO of Marvell Technology, Inc.

The 340%+ 12-month rally isn’t just sentiment-driven. Marvell Technology, Inc. reported 28% YoY revenue growth in Q1 FY2027, with guidance implying 35% YoY growth in Q2 — and CEO Matt Murphy confirmed ‘exceptional AI-related bookings’ are accelerating across all major hyperscalers. Its data center segment now accounts for 76% of revenue, up from just 35% five years ago. Strategic acquisitions — Cavium ($6 billion), Inphi ($10 billion), Celestial AI — have transformed the company from a legacy storage controller vendor into a full-stack AI infrastructure partner. That shift is now quantifiable: interconnect revenue is on track to double from $500 million in FY2026 to $1 billion by FY2028, while switching revenue jumps to $1.1 billion — all while maintaining a conservative 0.29 debt-to-equity ratio and industry-leading financial flexibility.