Can Marvell’s AI infrastructure pivot turn custom silicon and optics into a lasting edge over bigger semiconductor rivals?

What’s Driving Marvell’s AI Infrastructure Shift?

Marvell Technology, Inc. has executed a decisive pivot away from consumer IoT and mobile chips — businesses with volatile demand and compressed margins — toward high-value data center infrastructure. Today, over 85% of its revenue flows from AI-adjacent segments: high-speed optical connectivity, custom ASICs for Meta and Microsoft, Ethernet switches, and data processing units (DPUs). The company’s Teralynx T100, a 102.4 Tbps switch silicon launched in Q2 2026, is already being deployed in next-gen AI clusters across major cloud providers. Its lower latency and 30% reduced power draw versus prior-gen solutions make it a critical enabler for large language model training at scale — a direct competitive counterpoint to NVIDIA’s own networking stack and a complementary accelerator to Apple’s custom silicon roadmap.

How Does Marvell AI Strategy Compare to Broadcom and NVIDIA?

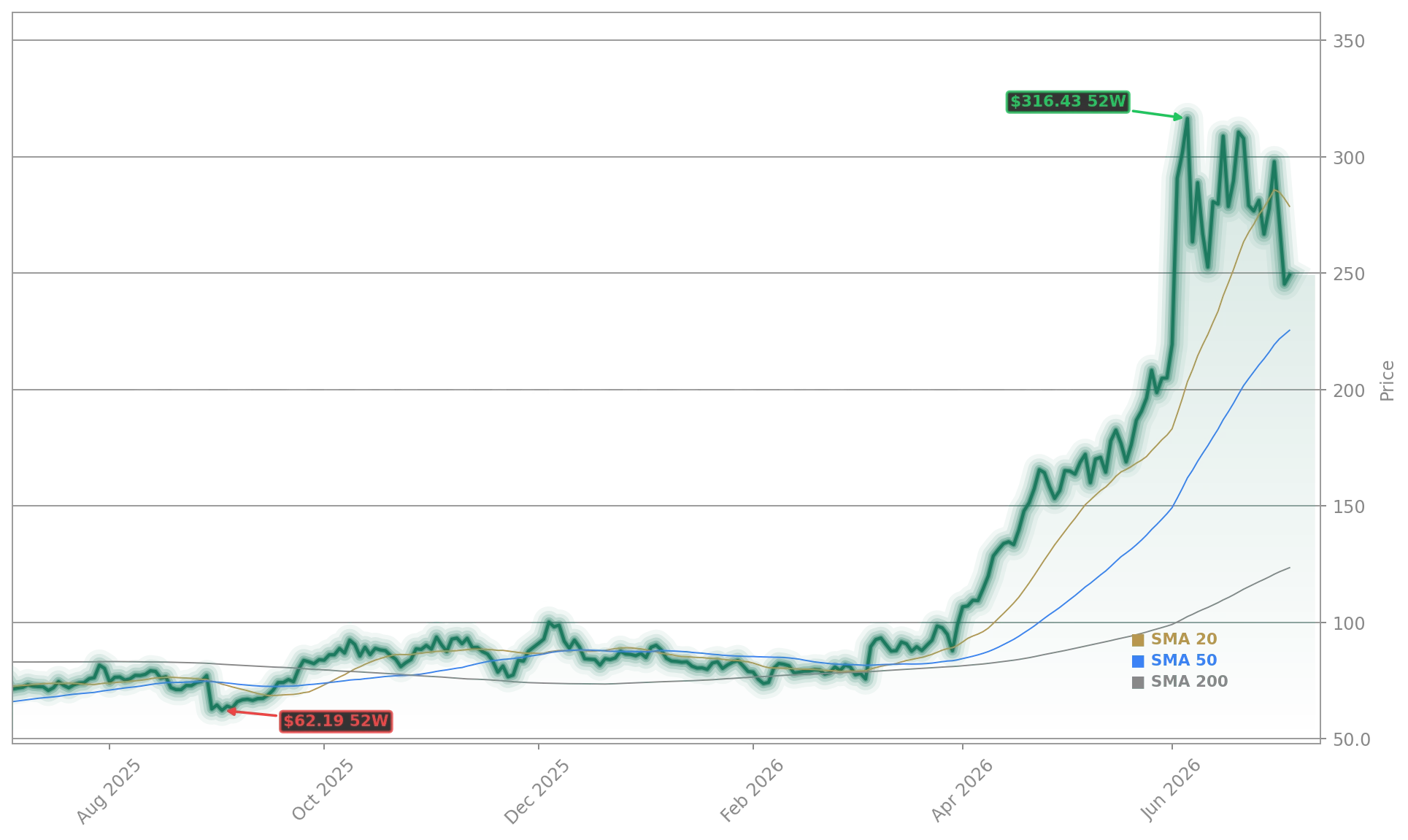

Unlike Broadcom — whose AI growth is anchored in server CPUs and AI accelerators — Marvell’s edge lies in the physical layer: analog, mixed-signal, and silicon photonics that move exabytes of data between GPUs and memory. Its collaboration with NVIDIA goes beyond licensing: the $2 billion strategic investment earlier in 2026 funds joint development of NVLink-integrated optical interconnects, designed to eliminate the bandwidth wall that constrains AI cluster scaling. UBS analyst Timothy Arcuri recently raised Marvell’s price target to $340 — up from $230 — citing this ‘infrastructure moat’ as a structural differentiator versus peers. Meanwhile, Cantor Fitzgerald upgraded its target to $300 and Stifel to $350, both emphasizing Marvell’s analog and photonic IP as irreplaceable in AI data centers.

Are Institutional Investors Buying the Narrative?

Yes — and aggressively. Tensor Edge Capital LLC initiated a $51.1 million position in Q1 2026, acquiring 515,400 shares — now its fourth-largest holding. PFG Investments LLC and QRG Capital Management both increased stakes by over 23%, while Sierra Summit Advisors launched a new $9.4 million position. Even amid $26.8 million in insider sales over 90 days — led by CEO Matthew J. Murphy and COO Chris Koopmans — institutional ownership remains at 83.51%, signaling deep conviction in the long-term Marvell AI Strategy. The company also declared a $0.06 quarterly dividend, its first payout in over two years, reinforcing financial discipline amid rapid reinvestment.

What Do Q2 2026 Results Reveal About Momentum?

Marvell Technology, Inc. reported Q2 2026 revenue of $1.62 billion — up 38% year-over-year and 8% sequentially — beating consensus by $47 million. Adjusted EBITDA surged 51% YoY to $612 million, pushing margins to 37.8%, up 320 basis points. Management reaffirmed full-year fiscal 2027 guidance and raised long-term targets: 41% CAGR revenue growth and 43% CAGR EBITDA growth from fiscal 2026 through fiscal 2029. Notably, data center revenue now comprises 72% of total sales — up from 39% in fiscal 2022 — validating the strategic reallocation. With the NASDAQ up 12% YTD and semiconductor stocks correcting in early July, Marvell’s +3.39% gain on July 6 — driven by reported delays in NVIDIA’s next-gen chip architecture — underscores its role as a key beneficiary of AI infrastructure supply chain diversification.

What’s Next for Marvell in the AI Hardware Stack?

Marvell is quietly building the physical layer of AI — the optical grid that makes GPU clusters viable at scale. This isn’t incremental; it’s infrastructural.— Timothy Arcuri, UBS

Marvell Technology, Inc. is now embedded in the foundational layer of AI infrastructure — where bandwidth, power efficiency, and signal integrity determine scalability. Its co-development with NVIDIA on silicon photonics and optical interconnects positions it to capture share in the $3.5 trillion semiconductor market projected for 2030. With new design wins at Google Cloud and Amazon Web Services expected to ramp in Q3 2026, and its custom ASIC business growing at 65% YoY, the Marvell AI Strategy is transitioning from promise to profit. Analysts project Marvell will outperform the S&P 500 tech sector over the next 18 months — not as a cyclical play, but as a structural infrastructure play akin to how semiconductor equipment makers like Applied Materials (AMAT) benefited from prior capex cycles.