Can Marvell’s AI networking momentum justify rising expectations, or is too much future growth already priced into the stock?

How strong were Marvell Earnings?

Marvell Technology, Inc. posted record fiscal Q1 revenue of $2.418 billion, up 28% year over year, while non-GAAP diluted EPS came in at $0.80, ahead of the company’s own midpoint outlook. Data center revenue rose 27% to $1.83 billion, and the communications segment increased 29% to $585 million, showing broad momentum across Marvell’s AI infrastructure exposure.

The latest Marvell Earnings matter because the company is increasingly positioned in the AI buildout layer rather than the application layer. Its custom silicon work and optical interconnect portfolio place it alongside major beneficiaries of hyperscale spending, including NVIDIA, Amazon, and Microsoft. Management also said AI-related bookings remain strong, reinforcing the view that networking and connectivity are becoming just as important as accelerators in modern data centers.

Why is Marvell lifting guidance?

The biggest market-moving takeaway was the new outlook. Marvell now expects fiscal Q2 revenue of about $2.7 billion, which would represent 35% year-over-year growth, with adjusted EPS of $0.93 versus $0.67 a year earlier. For the full fiscal year, the company raised its revenue target to nearly $11.5 billion, up from a prior goal of $11 billion.

More importantly for growth investors, Marvell also increased its fiscal 2028 revenue target to $16.5 billion from $15 billion. The company expects data center revenue to grow 50% in fiscal 2027, while interconnect revenue is now forecast to surge 70%. Management also sees its custom AI chip business doubling next year, a sign that hyperscaler demand is broadening beyond GPUs into application-specific silicon.

That longer runway helps explain why Marvell Earnings have drawn renewed attention from Wall Street. In a market that has rewarded infrastructure suppliers, Marvell is making the case that optical links, switching, and custom chips can remain a durable growth engine even if AI workloads evolve.

What is Wall Street saying about Marvell?

Analyst sentiment turned more bullish after the report. Deutsche Bank, Barclays, and Jefferies all raised their price targets following the quarter and the stronger Q2 outlook. Stifel also lifted its target to $210 from $140 earlier in the week, while Citi and Wells Fargo increased their targets as well, citing strength in Trainium 2-related ASIC demand and continued interconnect momentum.

HSBC had already upgraded the stock ahead of the report, pointing to what it described as an AI networking supercycle. That framing matters because Marvell is not trying to outcompete NVIDIA on flagship accelerators. Instead, it is building exposure to the connective tissue of AI clusters, a part of the market that has also helped Broadcom attract investor enthusiasm.

Still, valuation is becoming harder to ignore. Commentary tied to forward earnings estimates suggests MRVL is trading at a premium multiple, and some investors remain cautious about customer concentration and the long-term share of IP content tied to Amazon’s Trainium roadmap.

Can Marvell keep the AI trade alive?

The bull case rests on sustained hyperscaler capital spending, stronger optical adoption, and rising custom silicon revenue. Marvell has intellectual property tied to Amazon’s Trainium and has also worked with Microsoft on Maia, while its SRAM-related IP could become another growth lever in inference systems. If cloud spending remains elevated, the company has multiple ways to participate.

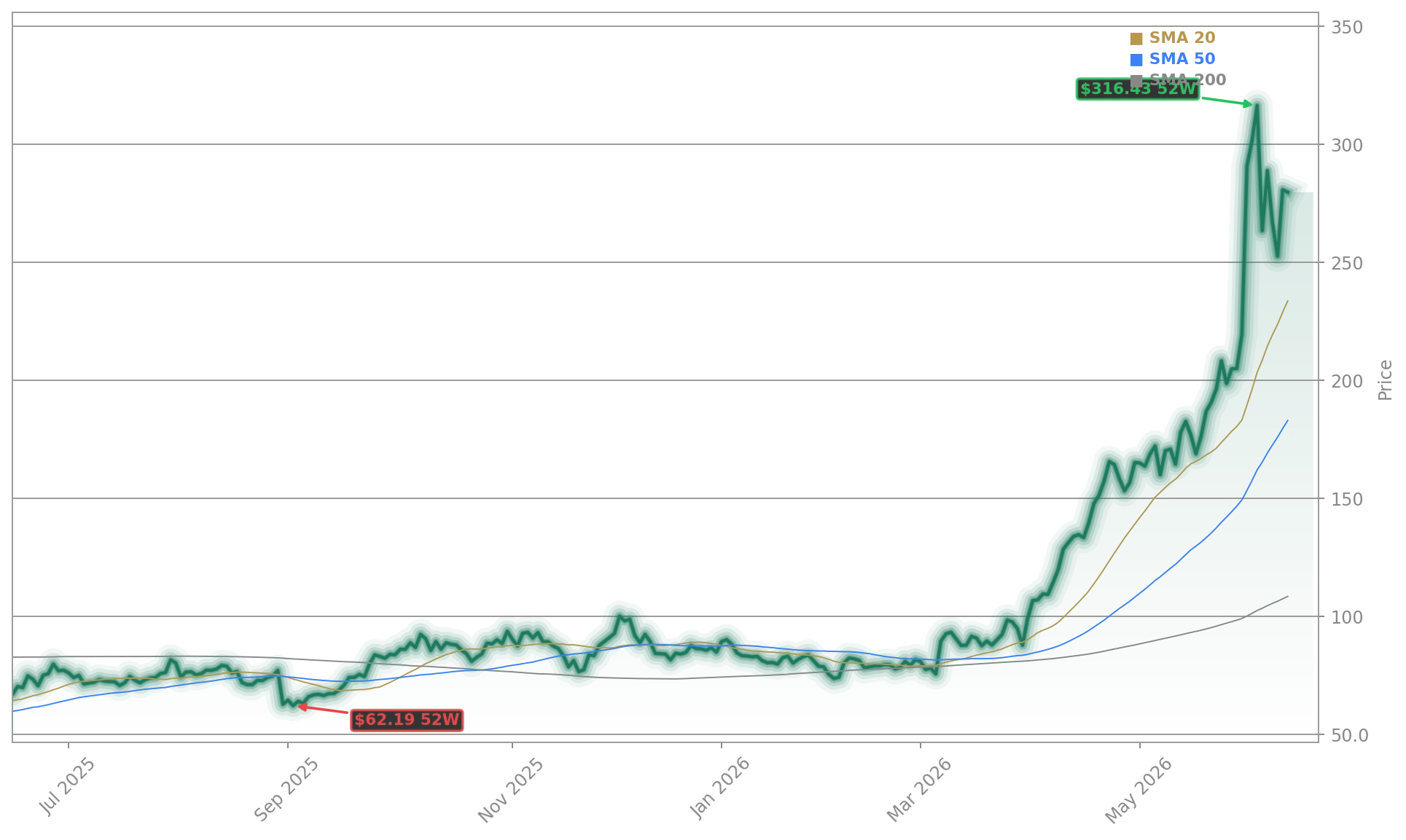

The risk is that expectations have risen almost as fast as the stock. At $205.00, MRVL is only modestly above its prior close and lower in after-hours trading, suggesting investors are still testing how much future growth is already priced in. Even so, Marvell Earnings showed that revenue acceleration is not just a near-term story but increasingly a multi-year AI infrastructure thesis.

Related Coverage: Investors looking for a deeper read on the immediate market reaction can also review Marvell Earnings +2.2% as AI Demand Lifts Outlook. That report looks at whether the post-earnings move above $200 can hold as Wall Street recalibrates expectations around AI demand, valuation, and execution.

Marvell Earnings strengthened the company’s standing as a key AI infrastructure player, not just a chip supplier with cyclical upside. For investors, the next test is whether custom silicon and optical growth can keep outrunning valuation concerns, but the raised outlook gives the bull case fresh support.