Are McDonald’s Earnings strong enough to justify the latest pre-market rally and keep the fast-food giant ahead of its rivals?

How did McDonald’s Earnings surprise Wall Street?

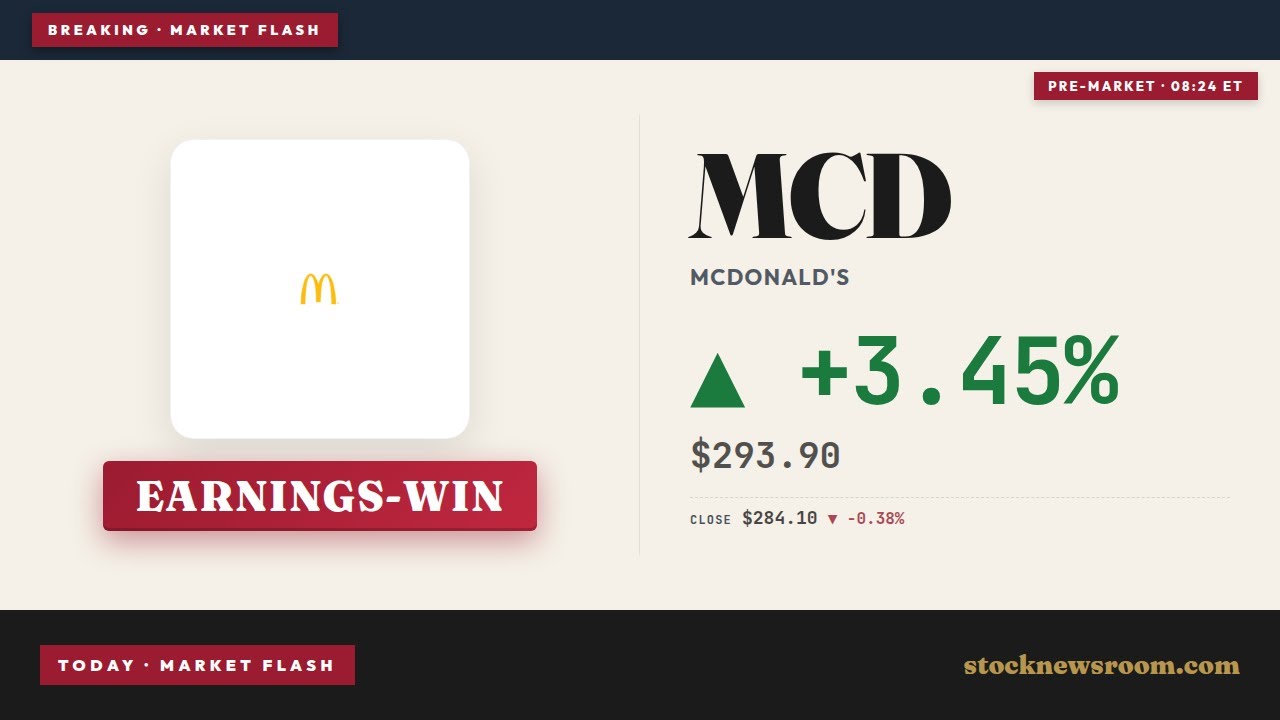

McDonald’s Corporation reported first-quarter 2026 diluted EPS of $2.78, with adjusted EPS at $2.83 after excluding restructuring costs related to internal modernization. That comfortably exceeded the consensus estimate of $2.74 per share. Revenue rose 9% year over year to $6.52 billion, also ahead of expectations around $6.47 billion. Global comparable sales increased 3.8%, supported by a 3.9% gain in the United States and 3.9% in international operated markets, while developmental and franchise markets added 3.4%.

Systemwide sales climbed 11% to more than $34 billion in the quarter, or 6% in constant currency, underscoring the strength of the franchised model. Net income rose 6% to roughly $1.98 billion, showing that the company was able to expand earnings despite higher interest costs and ongoing cost inflation in food and labor. Investors looking at McDonald’s Earnings are likely to focus on the combination of solid top-line growth and margin resilience.

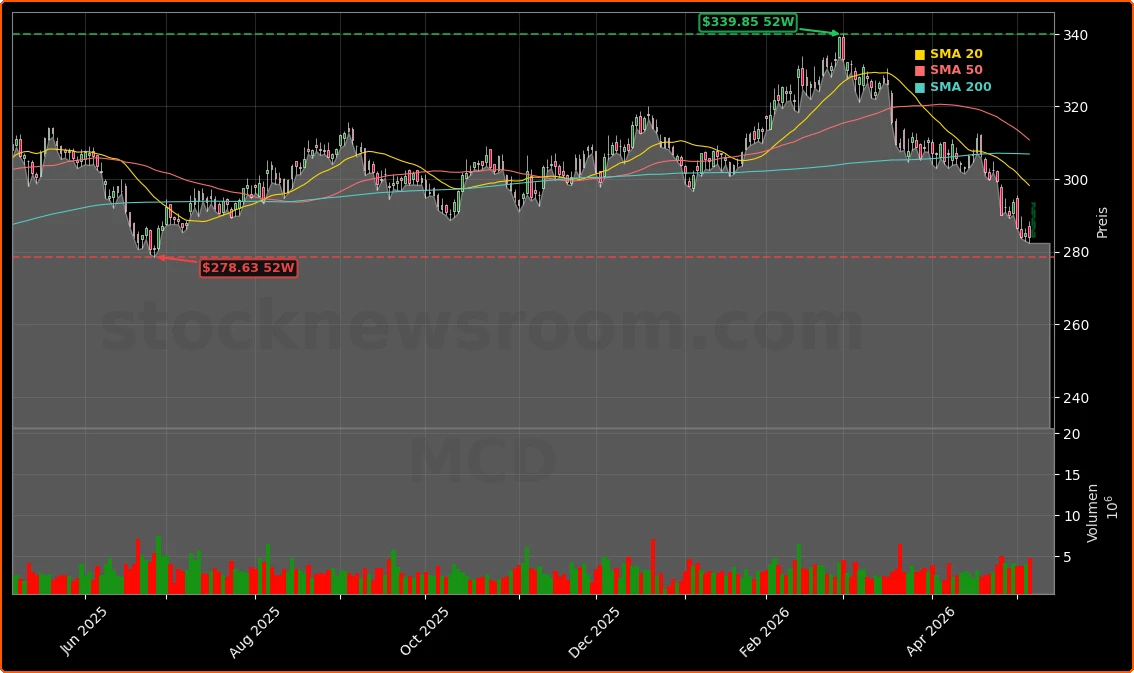

On the market side, MCD closed the previous session at $286.90 and finished down modestly at $284.10 (-0.38%). In early trading ahead of the U.S. open, the stock rebounded strongly, recently indicated around $293.32, up more than 3% in pre-market action as traders digested the upbeat quarterly numbers.

What is driving sales and traffic at McDonald’s?

Management highlighted three familiar pillars behind the quarter: perceived value, marketing scale, and menu innovation. U.S. comparable sales of 3.9% were supported by targeted price increases, stronger digital engagement, and popular promotions, including recurring campaigns such as Monopoly and limited-time menu items. The company continues to lean on higher-margin offerings like the Big Arch burger platform as a profit driver.

The loyalty ecosystem remains a key growth engine. Over the past twelve months, McDonald’s loyalty members generated more than $38 billion in systemwide sales across 70 markets, with more than $9 billion coming in the latest quarter alone. That loyalty and app-based ordering base helps the chain maintain traffic even as lower-income consumers feel pressure from higher gas prices, lingering inflation, and weak confidence.

Menu innovation is increasingly centered on beverages, where the brand is pushing against specialty drink lines from competitors such as Starbucks and Dunkin’. New “Refreshers” and crafted sodas, part of a revamped drink menu rolling out across U.S. restaurants, are designed to capture incremental afternoon and snack-daypart spending with relatively attractive margins. The company is also reshaping in-store operations by phasing out self-service soda machines in favor of crew-managed beverage stations and a dedicated “beverage specialist” role, aiming to improve consistency and the overall guest experience.

How do McDonald’s Earnings compare with fast-food peers?

The latest McDonald’s Earnings arrive as the broader quick-service sector is leaning heavily on value menus to defend traffic. Restaurant Brands International, parent of Burger King, recently posted better-than-expected same-store sales growth of around 3.2%, while Yum Brands reported solid trends at Taco Bell. These peers, along with others in the space, underscore that lower-priced, convenience-oriented offerings remain a rare bright spot in consumer discretionary spending.

However, McDonald’s scale and digital reach still set it apart. The $34+ billion quarterly systemwide sales figure dwarfs many rivals, and its loyalty program is now one of the largest in global food service. For U.S. investors benchmarking against the S&P 500 and Dow Jones Industrial Average, the stock’s pre-market jump puts MCD back among the key defensive names benefitting from a steady consumer trade-down dynamic.

At the same time, competition is intensifying around beverages and snacking occasions. Chains like Starbucks, smaller specialty players, and even convenience stores are offering a growing range of iced coffees, flavored sodas, and energy-style drinks. McDonald’s answer, backed by its nationwide footprint and drive-thru network, is to broaden its drink lineup while keeping pricing below many specialty competitors.

What are analysts and investors watching next?

Before the report, derivatives and prediction markets were already leaning bullish on McDonald’s Earnings, with traders pricing in a high probability of an EPS beat and a near-term upside move in the shares. Fundamental analysts at major firms such as UBS have maintained a “buy” rating and a price target around $365, pointing to the company’s value-led strategy, global brand strength, and cash-return profile as reasons to stay constructive despite the stock’s recent pullback.

Going forward, investors will pay particular attention to trends among lower-income consumers, a group that has become more cautious as inflation persists and fuel prices tick higher. Management has emphasized the importance of targeted value offers, including bundle deals and chicken-focused menu options, to keep visits frequent without compressing margins. The success of these initiatives will show up in traffic counts and same-store sales over the coming quarters.

Our global sales growth and expanding loyalty base show we can deliver results even in a challenging environment.— Chris Kempczinski, CEO of McDonald’s Corporation

Another focus will be the pace of cost inflation, especially for beef and wage expenses, and how effectively McDonald’s offsets it with menu pricing and productivity gains. With higher interest rates still weighing on financing costs across corporate America, the company’s ability to grow earnings faster than revenue will remain a key metric for portfolio managers comparing MCD to other defensive consumer names like Apple or growth leaders such as NVIDIA and Tesla in diversified U.S. equity portfolios.