Is the latest Micron Record rally a sign of a lasting AI memory supercycle or just another peak before a downcycle?

Is Micron Technology rewriting the AI playbook?

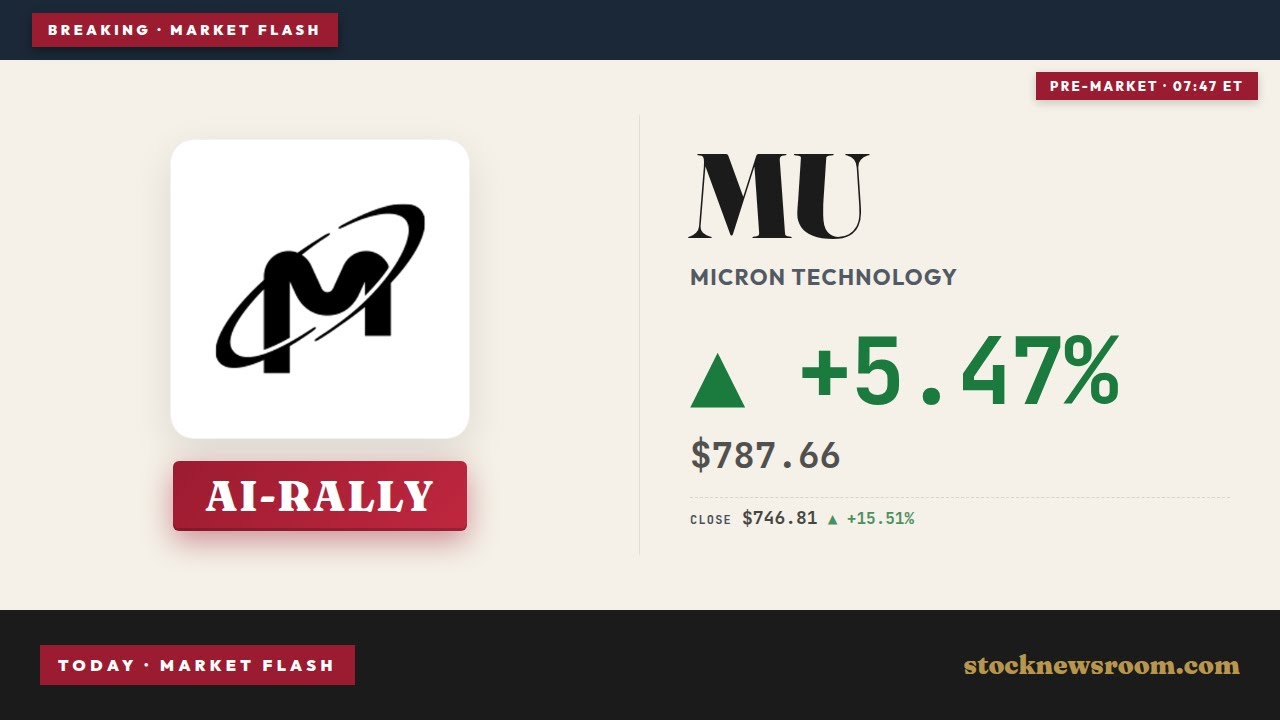

Friday’s surge added tens of billions of dollars to Micron Technology, Inc.’s market value in a single session, lifting the company to roughly $853 billion and cementing its status as one of the most important AI infrastructure plays in the NASDAQ 100. The move capped Micron’s best week since 2008, with the share price jumping close to 30% as investors scrambled for exposure to high‑bandwidth memory (HBM) and AI data‑center DRAM.

The latest Micron Record comes on the back of blockbuster fundamentals. Micron recently reported fiscal second‑quarter revenue of about $23.9 billion and guided for roughly $33.5 billion in the current quarter, underscoring how AI demand is turning memory into a strategic bottleneck. HBM capacity is reportedly sold out through 2026, and memory shortages across hyperscale data centers are fueling expectations of sustained pricing power.

This puts Micron in the same AI critical‑path conversation as NVIDIA, with its GPUs, and CPU providers like AMD and Intel. For diversified U.S. investors, MU is no longer just a cyclical memory name; it has become a core expression of the AI infrastructure trade within the S&P 500 and NASDAQ.

How extreme is the Micron Record valuation?

Despite the parabolic chart, Micron still trades at what many consider a surprisingly low multiple for an AI leader. Recent estimates put the stock at around 7–8 times forward 12‑month earnings, making it one of the cheapest high‑growth names in the Nasdaq‑100 on an earnings basis. That apparent disconnect is a big part of why the Micron Record run has captivated Wall Street: earnings revisions are surging faster than the stock itself.

Goldman Sachs has highlighted that Micron has logged more positive EPS estimate revisions than virtually any peer since late 2023, as analysts scramble to catch up with AI‑driven demand. Sector‑wide, memory producers are now trading at mid‑ to high‑single‑digit price‑to‑earnings ratios, but the underlying earnings power has changed dramatically as HBM and data‑center DRAM displace lower‑margin legacy products.

From a portfolio construction perspective, the risk is two‑sided. If AI workloads and agent‑based systems scale as aggressively as bulls expect, Micron’s current valuation could look conservative in hindsight. If AI capex normalizes or over‑ordering leads to a familiar memory downcycle, today’s Micron Record peak might mark a painful turning point.

Why are analysts so divided on Micron Technology?

The analyst community is nearly unanimous on one point: very few want to be outright bearish. Roughly 49 analysts rate Micron as a buy and only a handful recommend holding, while none currently carry a formal sell rating. Yet underneath that apparent consensus, price targets span an unusually wide range.

On the cautious side, Pierre Ferragu at New Street Research rates the stock Neutral with a $265 target, implying roughly 65% downside from Friday’s close. Bernstein’s Mark Li maintains an Overweight rating but still sees room for a one‑third pullback with a $510 target. The average target around $600 suggests nearly 20% downside versus the latest print, reflecting concerns about overheating sentiment and the classic cyclicality of memory.

Bulls, however, see the Micron Record as a waypoint, not a peak. Deutsche Bank analyst Melissa Weathers and D.A. Davidson’s Gil Luria both rate Micron a Buy with $1,000 price targets, implying about 25–35% upside from current pre‑market levels. They argue the industry is entering a long AI memory supercycle in which structurally higher margins and disciplined capacity additions will keep earnings elevated.

Where does Micron stand versus other AI leaders?

For U.S. investors who already hold heavy positions in NVIDIA, Apple or other mega‑caps, the question is how Micron fits into the broader AI stack. Recent commentary from Wall Street framed a “changing of the guard” in AI leadership, with capital rotating from the most crowded GPU trade toward alternative beneficiaries like Micron, AMD and Intel. Memory has emerged as a gating factor for training and inference workloads, giving Micron leverage to nearly every major AI platform.

Unlike GPU vendors that face intensifying competition from custom accelerators and in‑house silicon, Micron benefits from industry consolidation and limited high‑end HBM suppliers. At the same time, the company’s exposure to PCs, smartphones and autos means it still carries cyclical baggage that pure‑play AI investors need to respect. The current Micron Record rally is being driven overwhelmingly by data‑center and AI‑server demand; any slowdown in that segment could expose the more traditional parts of the business.

Related Coverage

For a deeper dive into whether this Micron Record surge marks the beginning of a sustainable AI memory supercycle or just another euphoric spike, readers can review the earlier analysis “Micron Record: +12.7% Rally as AI Memory Demand Explodes”. That piece explores how rapidly tightening HBM supply and hyperscaler capex trends set the stage for today’s dramatic moves, and lays out key risk factors long‑term investors should continue to monitor.

The Micron Record rally underlines how central AI memory has become to the next leg of the technology bull market, while sharp disagreements among top analysts highlight both substantial upside and meaningful downside if the AI build‑out stumbles. For U.S. investors, Micron has evolved into a core barometer of the AI infrastructure trade, and the coming quarters will show whether booming HBM demand can justify talk of $1,000 targets or if this Micron Record proves to be a short‑lived peak.