Is the MicroStrategy Bitcoin Strategy a visionary $63 billion balance-sheet play or a leveraged time bomb for crypto markets?

How is MicroStrategy positioning after the latest rally?

MicroStrategy Incorporated has transformed itself from a traditional enterprise analytics vendor into the largest corporate holder of Bitcoin worldwide. As of April 19, the company disclosed holdings of roughly 815,061 BTC, representing close to 4% of the circulating supply and more than 76% of all Bitcoin held by publicly listed treasury companies. Between April 13 and April 19 alone, the group acquired 34,164 coins for about $2.54 billion at an average price near $74,395 per Bitcoin, underscoring that the MicroStrategy Bitcoin Strategy remains firmly in accumulation mode even as other corporates step back.

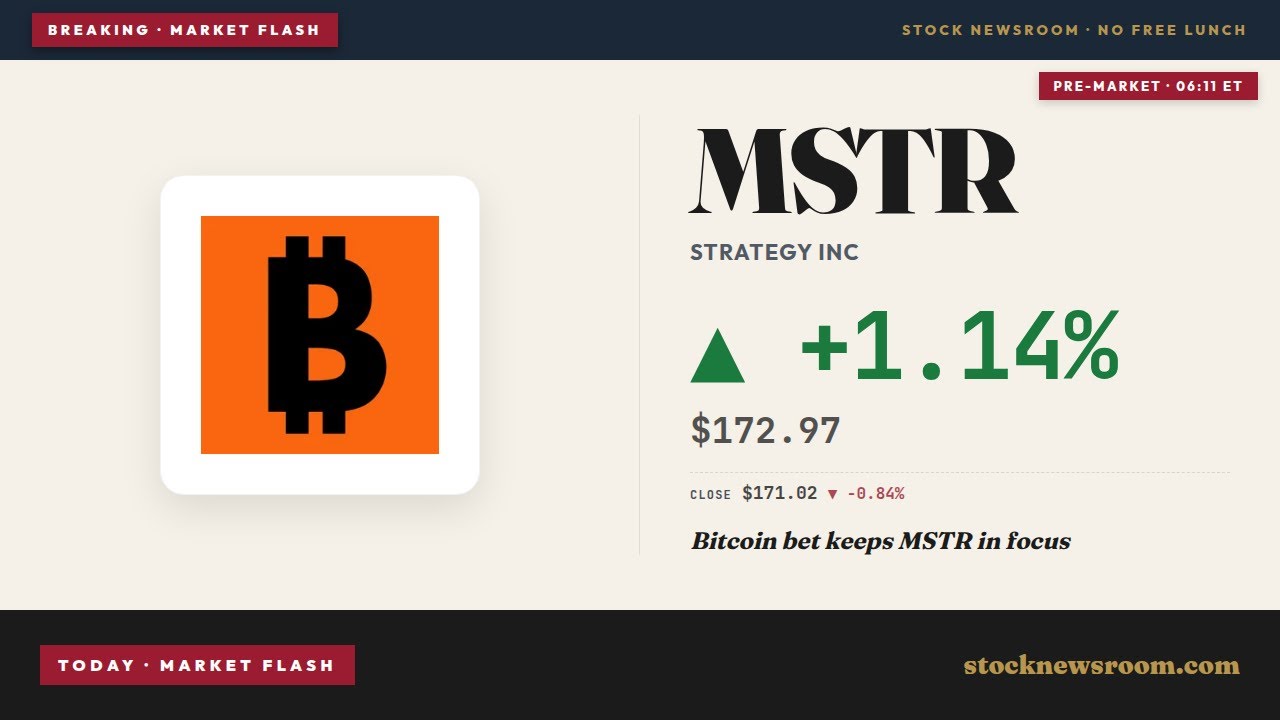

On the equity side, MSTR shares finished the last session at $171.02, just above the prior close of $170.87, and were indicated modestly higher in pre‑market trade near $172.76. The stock has become a high‑beta proxy for Bitcoin on the NASDAQ, often amplifying moves in the underlying coin as traders use it for listed exposure instead of, or in addition to, spot BTC or ETFs. That dynamic has drawn in both institutional buyers and short‑term traders who treat the name as a leveraged Bitcoin vehicle rather than a classic software stock.

What defines the MicroStrategy Bitcoin Strategy today?

The core of the MicroStrategy Bitcoin Strategy is simple: raise capital through equity, convertible notes, and preferred instruments, then deploy nearly all proceeds into additional Bitcoin. The company has now spent more than $61 billion to $63 billion on its stack at an average cost in the mid-$75,000 range per coin. Instead of distributing excess cash or prioritizing conventional R&D and M&A, management under Executive Chairman Michael Saylor is effectively using the balance sheet as a long‑term, leveraged Bitcoin treasury.

That approach distinguishes MicroStrategy from spot Bitcoin ETFs such as the iShares Bitcoin Trust, where coins are held on behalf of millions of investors who can exit without triggering immediate forced selling of the underlying BTC. In contrast, MicroStrategy’s holdings sit on a single corporate balance sheet backed by a concentrated capital structure. If the company were ever forced to unwind a meaningful portion of its position, selling pressure would hit the market in a much more focused wave than redemptions from diversified ETF holders.

For now, the debt stack — about $8.2 billion of unsecured convertible senior notes — is not collateralized by Bitcoin, avoiding the risk of margin calls on downside volatility. Management has argued that only an extreme price decline, toward roughly $8,000 per coin, would make a forced liquidation scenario realistic, a level that would also be deeply disruptive to broader crypto markets. In addition, MicroStrategy holds around $2.2 billion in cash, enough to cover more than two years of fixed obligations without needing to sell BTC.

How are analysts and capital markets reacting?

On April 21, Cantor Fitzgerald raised its price target on MSTR from $192 to $212 and reiterated an Overweight rating, citing the durability of U.S. consumer spending and arguing that sector‑wide macro fears look overstated. The firm still sees Q1 2026 targets as achievable and flagged potential S&P 500 index inclusion as a medium‑term catalyst. That upgrade followed a sharp 9.4% jump in the stock on April 22, when bulls highlighted the latest $2.54 billion Bitcoin purchase, growing institutional interest in MSTR shares, and a firmer Bitcoin price as key drivers.

At the same time, insider filings show some selling by company executives via Form 144 notices in late March and early April, a reminder that management is actively managing personal exposure even as the corporate treasury leans harder into Bitcoin. The company also continues to tap preferred equity via its STRC instrument, which pays an 11.5% annual yield backed by ongoing Bitcoin acquisitions. Critics, including long‑time gold advocate Peter Schiff, have attacked STRC’s sustainability and payout math, warning that if issuance grows faster than Bitcoin’s price, pressure could build to cut the dividend — a step that could hurt STRC, MSTR, and potentially Bitcoin sentiment.

What does this mean for crypto and tech investors?

For U.S. investors comparing options across the tech and crypto landscape, MicroStrategy’s approach stands in stark contrast to mega‑caps like NVIDIA, Tesla and Apple, all of which have, so far, kept digital assets peripheral or entirely out of their corporate treasuries. Whereas those names monetize AI, EVs, and hardware ecosystems to drive cash flows, MicroStrategy is increasingly monetizing capital markets access in order to scale its Bitcoin exposure. That makes the stock less comparable to traditional software peers and more akin to a publicly traded, leveraged BTC holding company with a legacy analytics business attached.

Correlation to Bitcoin remains high, which is why many technical analysts on platforms such as TradingView treat MSTR as a speculative vehicle that can overshoot both to the upside and downside relative to spot BTC. The prospect of S&P 500 inclusion further complicates the picture: if added, the stock could see incremental forced buying from index funds, potentially deepening its role as a bridge between traditional equity portfolios and the crypto asset class.

Related Coverage

Investors looking for a deeper dive into funding dynamics can review how rising interest costs and complex debt structures are reshaping leverage in the MicroStrategy Bitcoin Strategy in this analysis of MicroStrategy’s Bitcoin financing and recent share price surge. For a broader context on the underlying asset, the article on Bitcoin market analysis after a 52% crash examines whether the current consolidation phase is a launching pad for another leg higher or a warning that the post‑crash rebound is losing steam.

The MicroStrategy Bitcoin Strategy has turned a mid‑cap software vendor into one of the most influential corporate players in crypto, offering equity investors high‑octane exposure to Bitcoin’s upside and downside. For U.S. portfolios, the stock can act as a tactical satellite holding rather than a core tech position, especially given the leverage embedded in its capital structure and maturity wall starting in 2028. As Bitcoin and funding markets evolve, the next chapters in MicroStrategy’s accumulation campaign will help determine whether this bold strategy continues to reward risk‑tolerant shareholders.