Will the upcoming Netflix Earnings release finally rescue the beaten-down streaming giant from its painful 43% plunge?

Can Netflix Earnings Revive the Beaten-Down Stock?

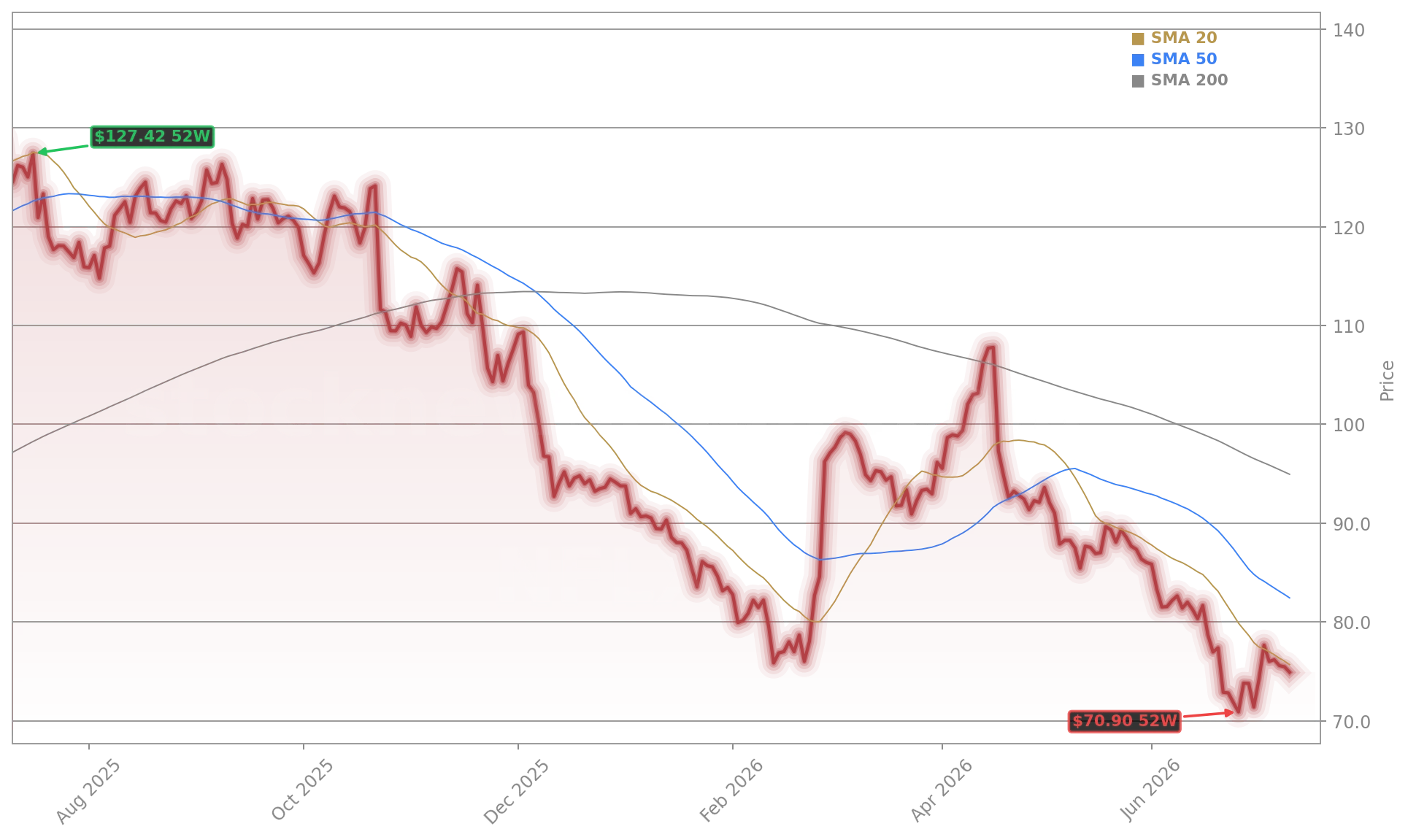

In intraday trading on Monday, Netflix (NFLX) shares climbed 2.29% to $75.12, recovering slightly from a Friday close of $73.37. Despite this short-term bounce, the broader picture remains challenging. The stock is down roughly 19% year-to-date and has plunged about 43% from its recent record high of $134. This severe correction has left investors wondering whether the upcoming Netflix Earnings release will act as a positive catalyst or trigger another leg down.

For the second quarter, Wall Street consensus estimates project quarterly earnings of 79 cents per share, up from 72 cents per share in the year-ago period. Revenue is expected to reach $12.58 billion, representing growth from the $11.08 billion reported in Q2 of last year. However, the bar is relatively low, and the market remains highly sensitive to forward guidance and subscriber engagement metrics.

Why Are Analysts Cutting Price Targets?

Ahead of the Q2 update, major Wall Street institutions have been adjusting their models, leading to a wave of price target cuts. Keybanc analyst Justin Patterson maintained an Overweight rating on the stock but slashed the price target from $115 to $92. Patterson warned that currency headwinds and a temporary lack of hit programming could lead to a downward revision of full-year numbers. He noted that the current sentiment around the company mirrors the challenges of 2022, when subscriber growth stalled.

Similarly, Oppenheimer analyst Jason Helfstein maintained an Outperform rating but lowered his price target from $120 to $100. Despite the cut, Helfstein argued that the stock’s multi-year low valuation is highly attractive and that short-term concerns regarding ad bookings and viewership are overblown. Other historical ratings include Citigroup analyst Jason Bazinet, who previously cut his target to $100, while B of A Securities analyst Jessica Reif Ehrlich holds a more bullish target of $125.

What Strategies Will Drive Future Growth?

To combat slowing engagement growth, which has slipped to 1-2%, Netflix is aggressively diversifying its business model. The company is exploring live sports and entertainment, securing events like the MLB Home Run Derby, and considering bids for future World Cups. Furthermore, a partnership with Spotify to expand into podcasting aims to capture mobile users during daytime hours, counteracting competition from YouTube.

The competitive landscape has intensified significantly. Paramount recently pulled off a major acquisition of Warner Bros. Discovery assets, expanding its library, while Disney and Fox have strengthened their streaming and distribution footprints. To maintain its dominance, the Los Gatos-based giant is leaning heavily into ad-supported subscription tiers, paid sharing, and potential price hikes, which could be announced alongside the next Netflix Earnings update.

Related Coverage

Given currency movement and a lack of hit programs, we believe more investors are expecting Netflix to lower full year numbers.— Justin Patterson, Keybanc Analyst

The strategic shift toward alternative content formats is not without hurdles. For a deeper analysis of the company’s latest distribution moves, read about the Netflix Strategy and how its pivot to live TV bundles introduces new operational risks. Meanwhile, as tech giants spend heavily to capture digital audiences, check out how the Meta AI Strategy is driving massive market gains through the launch of its new Muse platform.