Can Netflix Strategy revive engagement growth, or is the streaming giant drifting into a costlier and riskier phase?

Why is Netflix Strategy shifting now?

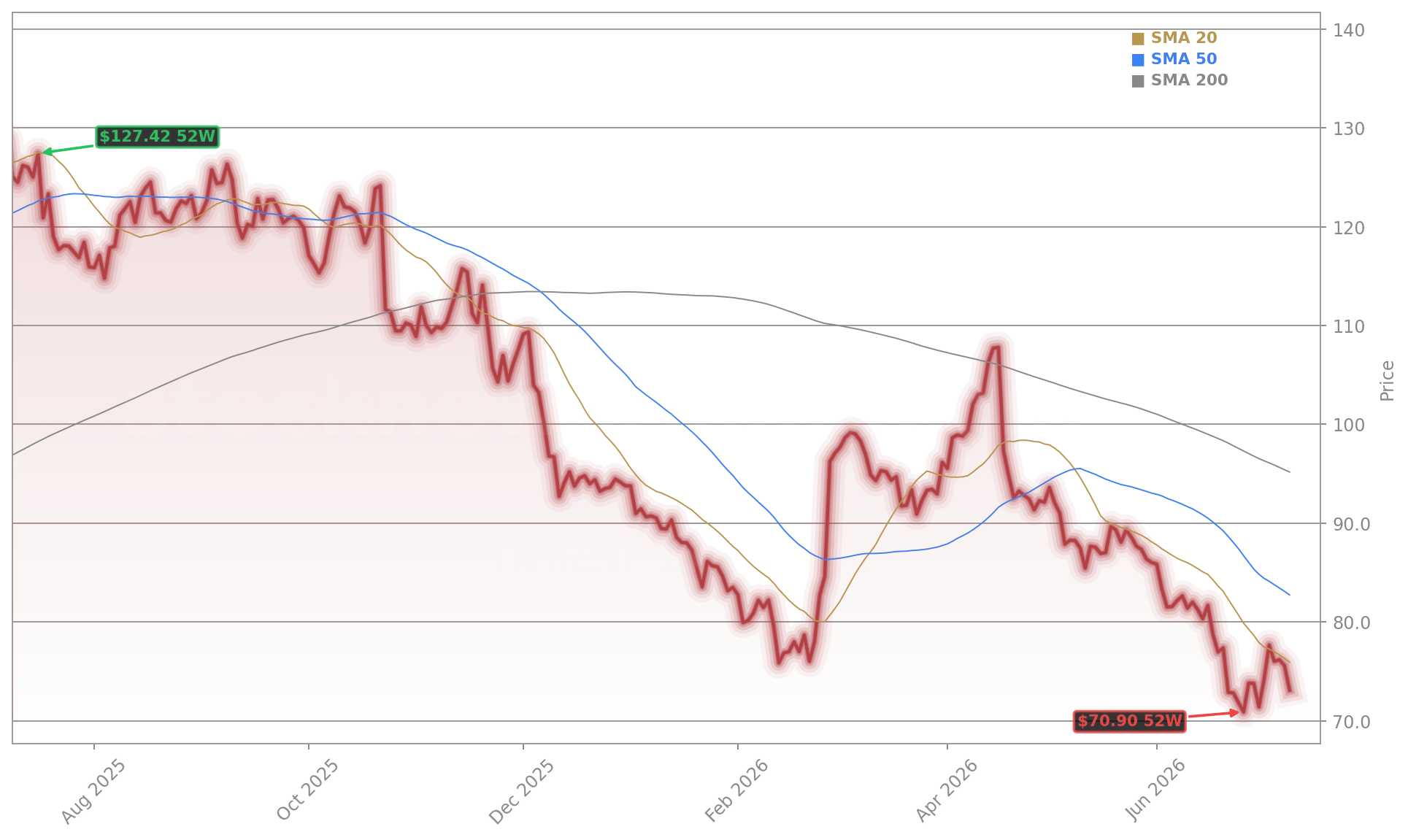

Netflix (NFLX) shares dipped 2.99% to $73.11 on Friday, July 10, 2026 — extending a nearly 24% three-month decline ahead of its July 16 earnings report. According to The Wall Street Journal, the company is actively exploring live linear channels and bundling third-party services like Peacock to counter decelerating engagement. Unlike its early days as a DVD-by-mail innovator, today’s Netflix Strategy must contend with saturated markets, rising content amortization costs, and intensifying competition from vertically integrated tech giants. While Netflix still streams 200 billion hours annually, its engagement growth has slowed dramatically — from double-digit gains to just 1–2% — prompting structural experimentation.

What’s in Netflix Strategy’s live-TV push?

Live TV isn’t just about sports — though Netflix’s reported bid for FIFA World Cup rights (2030 and 2034) alongside Disney and YouTube underscores its ambition. A $2 billion package could serve as both a subscriber acquisition lever and a global branding play, especially in emerging markets. But analysts remain wary: Barron’s warns this pivot “points to dangers ahead,” citing execution risk and capital intensity. Meanwhile, Barclays Bank PLC recently filed market-linked securities tied to Netflix’s performance — signaling institutional interest, but also hedging against volatility. The move into live channels also raises questions about infrastructure, rights licensing, and operational complexity — areas where traditional broadcasters and newer entrants like YouTube have deeper expertise.

How do bundles and short-form content fit into Netflix Strategy?

Netflix Strategy now includes three parallel initiatives: live channels, service bundling, and short-form video integration. Starting August 3, Netflix will debut three- to 20-minute clips from top digital publishers — including Variety, The Hollywood Reporter, BuzzFeed, Condé Nast, and People Inc. — directly on its homepage. This is a deliberate play for TikTok- and YouTube-style attention, targeting users who prefer ‘snackable’ content. Unlike Meta or Tesla, Netflix lacks a native social or hardware ecosystem — so these licensing deals are low-cost, high-velocity engagement tools. Jefferies maintains its ‘Buy’ rating on Netflix with a $110 price target, citing long-term upside, but notes “limited near-term catalysts” — especially given flat subscriber guidance and margin pressure.

What do analysts say about Netflix Strategy’s valuation?

Morningstar pegs Netflix as fairly valued at $80 per share — just $6.89 above its current trading level — and projects 10% compound annual revenue growth through 2030. That outlook hinges on international expansion, ad-tier monetization, and successful execution of the new initiatives. Citigroup, meanwhile, recently raised its price target to $85, citing “stronger-than-expected ad-tier uptake and early traction in short-form licensing.” However, RBC Capital Markets rates Netflix as ‘Sector Perform’, cautioning that “content spend remains elevated at $20 billion annually, and second-season viewership erosion — highlighted by The A.V. Club — remains a material risk to long-term retention.” The S&P 500’s tech-heavy composition makes Netflix’s success crucial for broader index momentum — especially as NASDAQ volatility persists.

How does Netflix Strategy compare to peers?

Netflix Strategy diverges sharply from Meta’s AI-driven ad monetization — recently highlighted by its Muse Spark 1.1 launch — and Apple’s hardware-anchored ecosystem. While Meta leans into AI-native advertising and NVIDIA-powered inference infrastructure, Netflix is doubling down on content aggregation and distribution innovation. That makes it more comparable to YouTube (Alphabet) than to pure-play tech firms. Yet unlike YouTube, Netflix lacks a robust creator monetization engine or search-driven discovery. Its bundling experiments — potentially combining ad-tier access with news, sports, and podcasting via Spotify — resemble early-stage convergence seen at Comcast and Verizon. With Wall Street increasingly focused on cash flow sustainability over subscriber count alone, Netflix Strategy must prove it can convert engagement into durable margin expansion — not just incremental hours watched.

Related Coverage: Netflix’s pivot away from M&A speculation toward live sports appears confirmed — ‘Netflix Merger +5% as Sports Push Replaces M&A Buzz’ details how the FIFA bid and live-event infrastructure are now central to its growth thesis. Meanwhile, ‘Meta AI Monetization +5.2% Rally After Muse Spark Launch’ offers a contrasting view of how AI-native platforms are monetizing attention — a benchmark Netflix Strategy may eventually need to match.

Netflix Strategy represents a high-stakes inflection point — not just for the company, but for the streaming sector’s broader evolution. For U.S. investors, it’s a test of whether content-first platforms can reinvent distribution without sacrificing profitability. The Q2 2026 earnings report on July 16 will be the first real stress test of this new direction. With engagement metrics, ad-tier growth, and live-content rollout timelines all under the microscope, Netflix remains a pivotal name for NASDAQ and S&P 500 portfolios.