If Paychex Earnings beat expectations, why did investors still send the stock lower?

Did Paychex Earnings Beat Expectations?

Yes—decisively. For the quarter ended May 31, 2026, Paychex, Inc. reported adjusted diluted earnings per share of $1.32, exceeding the consensus estimate of $1.30–$1.31. Revenue rose 12% year over year to $1.61 billion, topping analyst forecasts of $1.60 billion. GAAP EPS surged 43% to $1.17, while net income jumped 41% to $420.6 million. Management Solutions revenue grew 14% to $1.18 billion—fueled by organic acceleration, pricing gains, and an estimated 8 percentage points of lift from the April 2025 Paycor HCM acquisition. PEO and Insurance Solutions rose 9% to $369.7 million, and interest on client funds climbed 15% to $52.2 million. Operating margin expanded to 37.7% from 30.2% a year ago, while adjusted operating margin improved to 42.1%—a 170-basis-point gain reflecting disciplined cost management and integration progress.

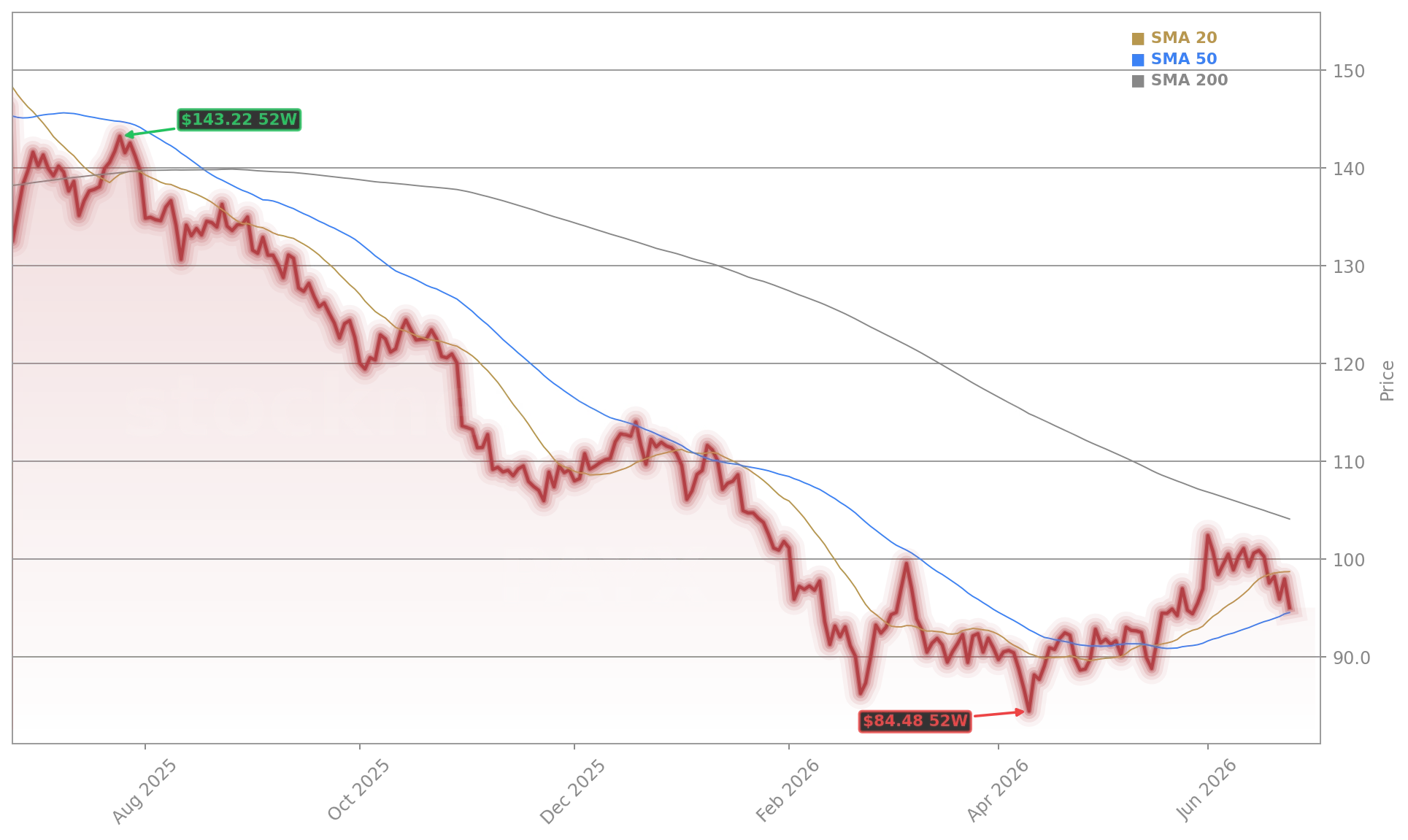

Why Did PAYX Shares Drop Despite the Beat?

Because the fiscal 2027 outlook muted enthusiasm. Paychex, Inc. projected total revenue of $6.84–$6.90 billion—within the $6.87 billion consensus but at the low end—and adjusted EPS of $5.90–$6.01, matching only the lower bound of analyst estimates. More critically, the company cited flat employment levels, no further Federal Reserve rate changes, and stable macro conditions as key assumptions—highlighting sensitivity to labor market softening. The guidance implies just 5%–6% total revenue growth, down sharply from fiscal 2026’s 17% surge. Investors interpreted this as a signal that Paychex’s post-acquisition growth inflection may be peaking—especially as peers like ADP and Workday face similar headwinds in HR tech adoption velocity. Citigroup analysts noted that ‘the guidance reflects prudent conservatism, not weakness—but it removes near-term catalysts for multiple expansion.’

How Is AI Driving Paychex’s Strategy?

Artificial intelligence is no longer a feature—it’s the foundation. Paychex, Inc. launched WISE, its AI-powered intelligence engine, across HCM platforms and internal operations. Leveraging 26 trillion data points, WISE automates tasks like payroll submissions, policy handbook updates, and compliance alerts. The company reports early monetization: over 10,000 customers are in a soft launch for AI timekeeping, and WISE-powered reporting enhancements are already generating revenue. CEO John Gibson emphasized that ‘organic growth accelerated throughout fiscal 2026—reaching double the pace seen at fiscal 2025’s close—driven by AI-enabled productivity and deeper client engagement.’ This positions Paychex, Inc. closer to the infrastructure layer of enterprise software, akin to how NVIDIA powers AI compute or Apple embeds intelligence into OS-level workflows—though at a smaller scale and slower monetization curve.

What Does the Balance Sheet Say About Resilience?

Very strong. Paychex, Inc. ended fiscal 2026 with $1.2 billion in cash, restricted cash, and corporate investments—and $4.6 billion in total borrowings. It reduced leverage by half a turn and repaid a $400 million debt tranche tied to the Oasis acquisition. Shareholder returns remained robust: $2.2 billion returned in fiscal 2026, including $1.6 billion in dividends and $611 million in buybacks. That’s a 115% payout ratio on adjusted net income—underscoring management’s confidence in cash flow durability. RBC Capital Markets recently reiterated its ‘Outperform’ rating on PAYX, citing ‘best-in-class free cash flow generation and a fortress balance sheet that supports both strategic M&A and consistent capital return.’

How Does Paychex Earnings Compare to Broader Market Trends?

We finished fiscal 2026 with strong momentum, delivering double-digit revenue and earnings growth while accelerating organic revenue growth throughout the year.— John Gibson, CEO of Paychex, Inc.

In a market where the S&P 500 trades near all-time highs and the NASDAQ reflects AI optimism, Paychex Earnings stand out for their operational precision—not hype. While companies like Tesla and Meta navigate volatility around AI deployment timelines, Paychex, Inc. delivered double-digit growth with 44% adjusted operating margins and zero reliance on speculative capex. Its fiscal 2026 revenue growth (17%) outpaced the S&P 500’s 12% total return and the NASDAQ’s 22% gain—yet its stock underperformed both indices year-to-date. That divergence reflects Wall Street’s current preference for growth optionality over predictable execution. Still, Goldman Sachs maintains its $105 price target, noting ‘Paychex, Inc. remains a rare compounder in the payroll space—its AI roadmap and PEO scale create durable defensibility in uncertain labor markets.’