Can Qualcomm Acquisitions turn software ambition into real AI growth, or is Wall Street still unconvinced?

Why Two Qualcomm Acquisitions in One Week?

Qualcomm Incorporated executed two targeted acquisitions within 72 hours: first, Modular — developer of the Mojo programming language and MAX platform for portable AI model deployment — and second, SAM Seamless Network, an Israel-based provider of software-defined security for unmanaged IoT devices. Together, these deals close critical capability gaps in Qualcomm’s AI and edge infrastructure stack. Modular strengthens Qualcomm’s ability to deliver agentic AI workflows across heterogeneous hardware, while SAM Seamless bolsters security for the 5G-connected car, industrial, and smart home ecosystems. Neither acquisition involved massive valuations, but both align tightly with Qualcomm’s stated goal of becoming a full-stack provider — not just a chip vendor — for AI at the edge and in the cloud.

How Do Qualcomm Acquisitions Compare to Rivals?

Unlike NVIDIA’s $100 billion-plus acquisition of Arm — a move designed to lock in IP control — Qualcomm Acquisitions are surgical, software-first, and integration-ready. Modular’s Mojo language, for example, directly competes with NVIDIA’s CUDA ecosystem by enabling AI developers to deploy models across Snapdragon, x86, and RISC-V hardware without rewriting code. Meanwhile, SAM Seamless fills a void that Apple and Samsung have yet to address at scale: zero-trust security for low-power, resource-constrained devices. This contrasts sharply with Intel’s stalled AI software strategy and AMD’s reliance on third-party frameworks. Citigroup analysts note that ‘Qualcomm’s acquisition velocity reflects a disciplined, use-case-driven approach — rare among legacy semiconductor players.’

What’s Next After Qualcomm Acquisitions?

The Snapdragon Summit 2026 — set for September 22–24 in Hawaii — will serve as the first major validation point for these moves. Qualcomm is expected to unveil the Snapdragon 8 Elite Gen 6, reportedly built on TSMC’s 2-nanometer process and optimized for on-device generative AI. Early leaks suggest the chip will power Immersed’s Visor headset — a device boasting 2 million more pixels than Apple’s Vision Pro at 70% lower cost and weight. Partnerships with Meta and Samsung further reinforce Qualcomm’s centrality in the AR/VR and automotive AI stacks. RBC Capital Markets recently reaffirmed its ‘Outperform’ rating on Qualcomm Incorporated, citing ‘the inflection point in automotive silicon and AI infrastructure monetization.’

Are Institutional Investors Buying the Narrative?

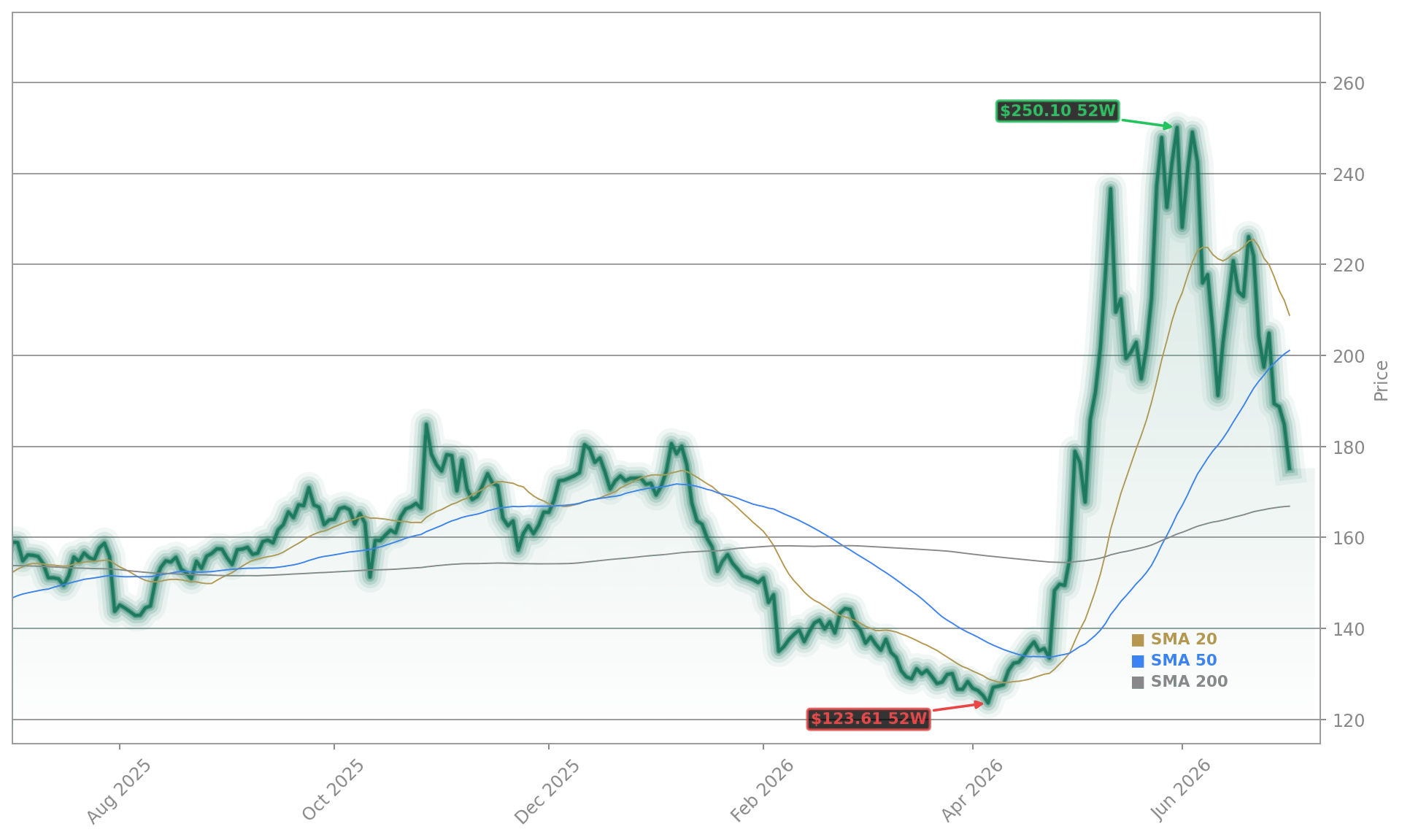

Yes — but selectively. Palouse Capital Management increased its stake in Qualcomm Incorporated by 78.1% in Q1 2026, making it the fund’s 10th-largest holding. Meanwhile, Benchmark and Robert W. Baird maintain $300 price targets, implying 72% upside from current levels. Yet the consensus remains ‘Hold,’ with a $220.45 median target — still 26% above today’s $174.74. The stock trades 8.42% above its 200-day moving average ($145.44), but the RSI at 38.9 suggests oversold conditions. Notably, Qualcomm’s non-smartphone revenue grew 22% year-over-year in Q2 2026, reaching $5.1 billion — evidence that diversification is already bearing fruit, even as smartphone revenues decline.

What Do Analysts Say About the AI Pivot?

Goldman Sachs analysts highlight ‘meaningful traction in automotive and data center design wins,’ but caution that ‘revenue conversion remains lumpy and backend-loaded.’ Morgan Stanley notes that Qualcomm’s $40 billion non-handset target by 2029 is ‘ambitious but credible,’ especially given its design wins with major OEMs and hyperscalers. Still, the firm lowered its near-term earnings estimates by 4% to reflect slower-than-expected cloud AI adoption. The disconnect between strategic clarity and market reaction remains stark: while Qualcomm Incorporated’s long-term roadmap is arguably its strongest in a decade, short-term execution risk and macro headwinds — including the broader chip sell-off that dragged the SOX index down 7% — continue to pressure sentiment.

Qualcomm’s acquisition velocity reflects a disciplined, use-case-driven approach — rare among legacy semiconductor players.— Citigroup analysts

Related Coverage: The challenges facing Qualcomm’s AI strategy are explored in depth in Qualcomm AI Strategy -7.7%: Warning Signs on AI Pivot, which questions whether investor patience can hold until data center chips deliver material revenue. Meanwhile, Micron Earnings -7.3% After Record Quarter and AI Boom reveals how even record-breaking AI memory demand failed to lift sentiment — a cautionary parallel for Qualcomm’s own high-expectation AI transition.