Can Qualcomm’s AI roadmap justify investor patience before its data center chips generate meaningful revenue?

What Does Qualcomm’s AI Data Center Roadmap Actually Deliver?

Qualcomm Incorporated’s Investor Day on June 24, 2026 delivered a clear, quantified target: $15 billion in annual data center AI chip revenue by fiscal 2029 — up from an estimated $5 billion in 2027. That target assumes successful deployment of the Dragonfly C1000 CPU (slated for 2028 production) and the Dragonfly AI300 inference chip, still in design. Crucially, no data center chips have shipped yet. Per Q2 FY26 filings, hyperscaler engagement remains ‘on track for initial shipments later this calendar year’ — language that falls short of ‘shipping’ or ‘revenue-generating.’ The gap between roadmap and reality is wide: NVIDIA (NVDA) posted $75.25 billion in data center revenue in a single quarter — more than five times Qualcomm’s entire 2029 target. Morningstar acknowledges Qualcomm is ‘not expected to unseat NVIDIA’s dominance in AI’ but sees a path to meaningful share — especially on efficiency metrics like dollars per token or per kilowatt.

How Does the Modular Acquisition Fit Into Qualcomm AI Strategy?

The $3.92 billion stock-based acquisition of Modular — an AI software infrastructure startup — is central to Qualcomm’s AI ambitions. Unlike pure-play chipmakers, Qualcomm is betting that vertical integration of silicon, system-on-chip architecture, and AI runtime software will differentiate it in the data center. Modular’s stack is expected to accelerate benchmark performance for Qualcomm’s upcoming chips and enable faster deployment across Meta’s infrastructure. DZ Bank upgraded Qualcomm to ‘Buy,’ citing ‘increasing confidence in the company’s expansion beyond handsets,’ though the firm noted the stock remains down 1.6% from its pre-announcement level. The acquisition also complements Qualcomm’s earlier Alphawave Semi purchase — though data center revenue from that deal remains unreported separately in Q2 FY26 results.

Can Qualcomm Offset Smartphone Weakness With Non-Handset Growth?

Q2 FY26 revenue totaled $10.60 billion, down 3.46% year over year — with handset sales at $6.02 billion, down 13%. That weakness stems from memory supply constraints and softness among Chinese OEMs. Meanwhile, non-handset revenue — including automotive, IoT, and emerging data center lines — is targeted to reach $40 billion by fiscal 2029. That implies a near-tripling of current non-handset sales, a dramatic shift away from Qualcomm’s legacy business. Competitors like NVIDIA, AMD, and Apple are all investing heavily in AI silicon, but Qualcomm’s dual focus on edge AI (via Snapdragon) and cloud AI (via Dragonfly) creates a unique, if unproven, moat. Still, the transition is not without risk: Micron Technology’s explosive Q3 earnings — driven by AI memory demand — highlights how quickly adjacent markets can outpace chip design timelines.

What’s the Real Competitive Threat to Qualcomm AI Strategy?

The dominant competitive reality is NVIDIA’s technical monopoly. As Bloomberg Tech’s Ed Ludlow observed, ‘NVIDIA absolutely dominates the market and whatever’s left, AMD kind of comes up and gets the rest.’ NVIDIA holds over 70% of the AI accelerator market, ships new architectures annually, and is scaling faster than any peer. AMD is cementing its position with Meta’s MI450 deployment — a direct competitor to Qualcomm’s Dragonfly roadmap. Qualcomm’s efficiency narrative may gain traction only when power costs — not silicon costs — become the limiting factor in data centers. That shift is coming, but not yet here. RBC Capital Markets recently reiterated its ‘Sector Perform’ rating on Qualcomm, noting ‘strong execution on mobile is no longer sufficient — data center credibility must be earned in 2027–2028.’

How Are Wall Street Analysts Pricing This Transformation?

NVIDIA absolutely dominates the market and whatever’s left, AMD kind of comes up and gets the rest.— Ed Ludlow, Bloomberg Tech

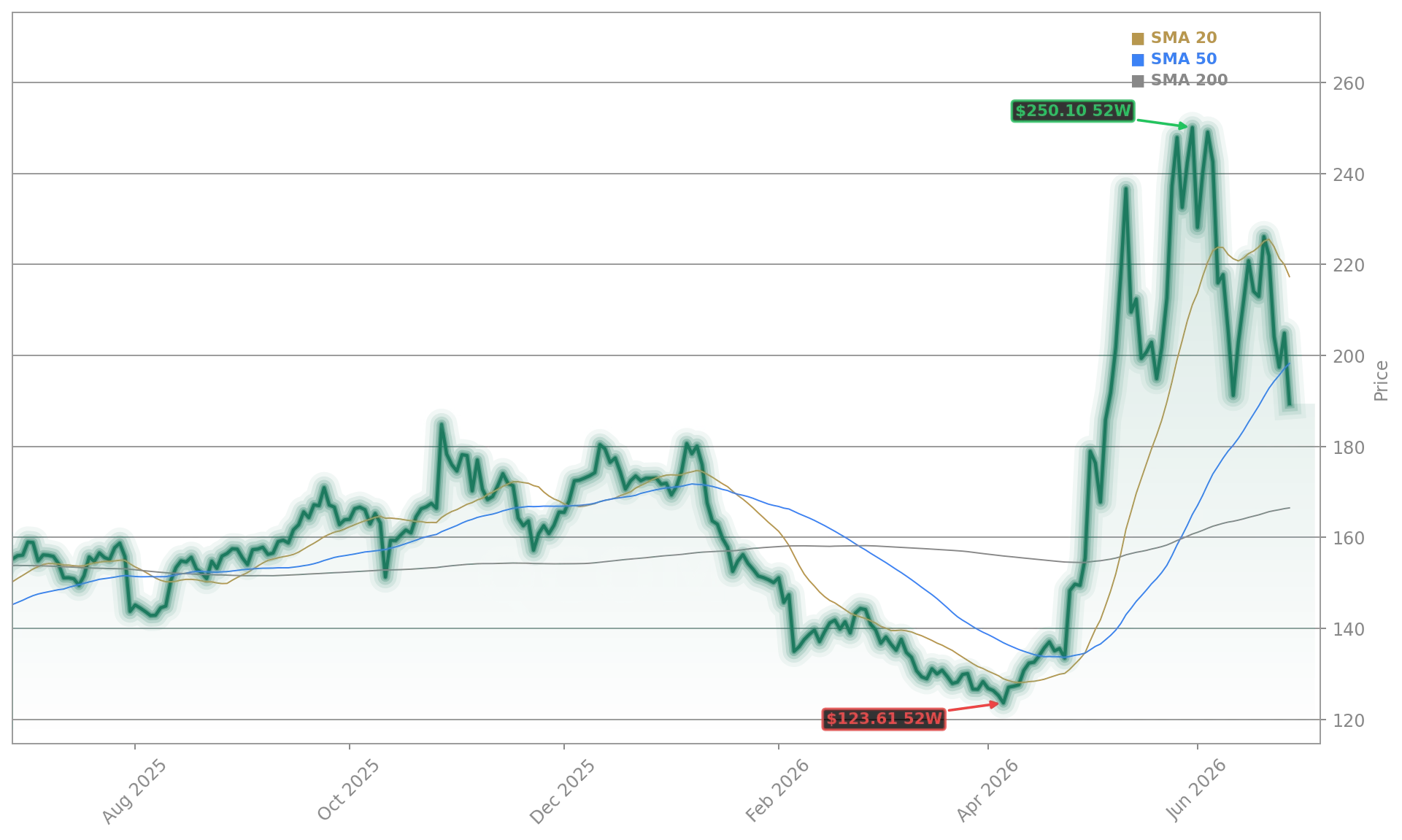

Analyst sentiment is cautiously constructive. Citigroup raised its price target to $225, citing ‘increased conviction in non-handset margins and hyperscaler traction.’ Goldman Sachs maintains a ‘Neutral’ rating but lifted its 2029 EPS forecast to $18.25 — aligning with Qualcomm’s guidance. Yet the stock’s volatility tells another story: after surging 13–15% in after-hours trading post-Investor Day, QCOM gave back most of those gains, closing June 25 at $204.90 — down 9.38% for the week. Options activity confirms investor bifurcation: over 12.7 million shares’ worth of options traded on June 26, with heavy volume in the $200 strike call — a clear bet on near-term upside, but also a sign of elevated uncertainty. The Qualcomm AI Strategy is now fully priced into the stock — and every shipment delay or benchmark miss will carry outsized weight.