Can Roku’s latest earnings surge and guidance hike turn its connected TV scale into lasting profit power for shareholders?

How strong were Roku Earnings in Q1?

Roku, Inc. generated roughly $1.25 billion in Q1 2026 revenue, up about 22% year over year and ahead of the mid‑teens growth management had signaled going into the quarter. That marked the company’s fastest quarterly top-line expansion in four years, driven by renewed strength in its high‑margin platform segment. GAAP net income reached about $85.7 million, far above the earlier outlook of $50 million, extending Roku’s streak to four consecutive profitable quarters.

Adjusted EBITDA surged more than 160% versus the prior year, and trailing free cash flow climbed more than 80%, underscoring that Roku Earnings quality is improving, not just the headline growth rate. On the back of this performance, management raised full‑year 2026 revenue guidance to roughly $5.535 billion, with about $5.0 billion expected from the platform business and $535 million from devices. Adjusted EBITDA guidance moved to approximately $675 million as Roku continues to target $1 billion in annual free cash flow by 2028 or earlier.

User engagement remained healthy, with 38.7 billion streaming hours in the quarter, up 8% year over year, and more than 100 million streaming households now using a Roku‑powered device worldwide. That scale is increasingly vital as advertisers shift budgets from linear TV to connected TV (CTV), where Roku aims to be the primary gatekeeper.

What is driving Roku’s platform momentum?

For investors dissecting Roku Earnings beneath the surface, the key story is the mix shift into higher‑margin platform revenue. Roku recently began breaking out this segment into advertising and subscriptions. In Q1, advertising revenue grew 27% to about $612.6 million, roughly half of total sales, as video ad growth outpaced broader U.S. OTT and digital ad markets. Subscription and related distribution revenue jumped 30% to roughly $518.5 million, helped in part by last year’s acquisition of the Frndly TV app. Excluding that deal, subscription revenue still climbed a robust 23%.

The Roku Channel has emerged as the platform’s second‑most‑engaged app in the U.S., reinforcing Roku’s role not only as an operating system but also as a content destination. The company is layering in new offerings like the low‑priced, ad‑free Howdy service at $2.99 per month, which has already surpassed one million subscribers despite being launched only in August 2025. Meanwhile, the devices segment—streaming sticks and Roku TVs—declined about 16% and now accounts for less than 10% of revenue, highlighting that Roku is increasingly a software and data‑driven ad business rather than a hardware vendor.

For U.S. investors comparing the stock with other streaming and CTV players such as Apple, Amazon and Alphabet, Roku’s advantage lies in being platform‑agnostic and tightly focused on CTV monetization, rather than bundling video inside a broader e‑commerce or mobile ecosystem. That niche focus, however, also means Roku remains highly sensitive to advertising cycles and competition for TV operating system share.

How did Wall Street react to Roku Earnings?

Roku Earnings triggered an unusually synchronized wave of analyst upgrades and price‑target hikes across Wall Street. Needham analyst Laura Martin reiterated a Buy rating and lifted her price target from $110 to $140, while Rosenblatt’s Barton Crockett maintained a Buy and took his target from $118 to $150. Benchmark’s Daniel Kurnos stayed at Buy and raised his target from $130 to $160, and KeyBanc’s Justin Patterson kept an Overweight rating while moving his target from $140 to $150.

The bullish tone extended further: Citizens analyst Matthew Condon reaffirmed a Market Outperform rating and pushed his target from $160 to $170, and Wells Fargo’s Steven Cahall maintained an Overweight rating while increasing his target from $137 to $167. Additional firms, including Pivotal Research, Susquehanna, JPMorgan, Guggenheim, and Piper Sandler, also raised price targets, generally positioning Roku as one of the best‑placed names to capture the CTV ad opportunity.

Despite the rally—ROKU is up more than 70% over the past 12 months—consensus on Wall Street still leans positive, with the average target price clustered in the low‑to‑mid $130s and many recent revisions running materially higher. The Benzinga Edge framework characterizes the shares as a classic high‑flyer: strong momentum and growth scores, offset by weak value metrics, reflecting a premium multiple that could amplify any downside if execution slips.

What risks and catalysts should investors watch?

Roku’s valuation remains demanding, with the stock trading at more than 50 times forward earnings by some estimates and an even richer multiple on free cash flow. That leaves little room for disappointment if ad spending slows or competitive pressure intensifies from tech heavyweights like Amazon’s Fire TV and Google TV. Recent insider selling by senior executives, including CEO Anthony Wood and Roku Media President Charles Collier under 10b5‑1 plans, may raise eyebrows among cautious investors, even though large pre‑scheduled sales are common after strong rallies.

At the same time, institutional ownership trends remain supportive. Vanguard Capital Management recently disclosed a passive 5.26% stake, signaling ongoing interest from large index and active managers. On the legal front, Roku faces a class action lawsuit alleging defective operating system updates that degrade TV performance, along with separate patent‑related scrutiny—headline risks that could weigh on sentiment if they escalate but have not yet derailed the fundamental growth story.

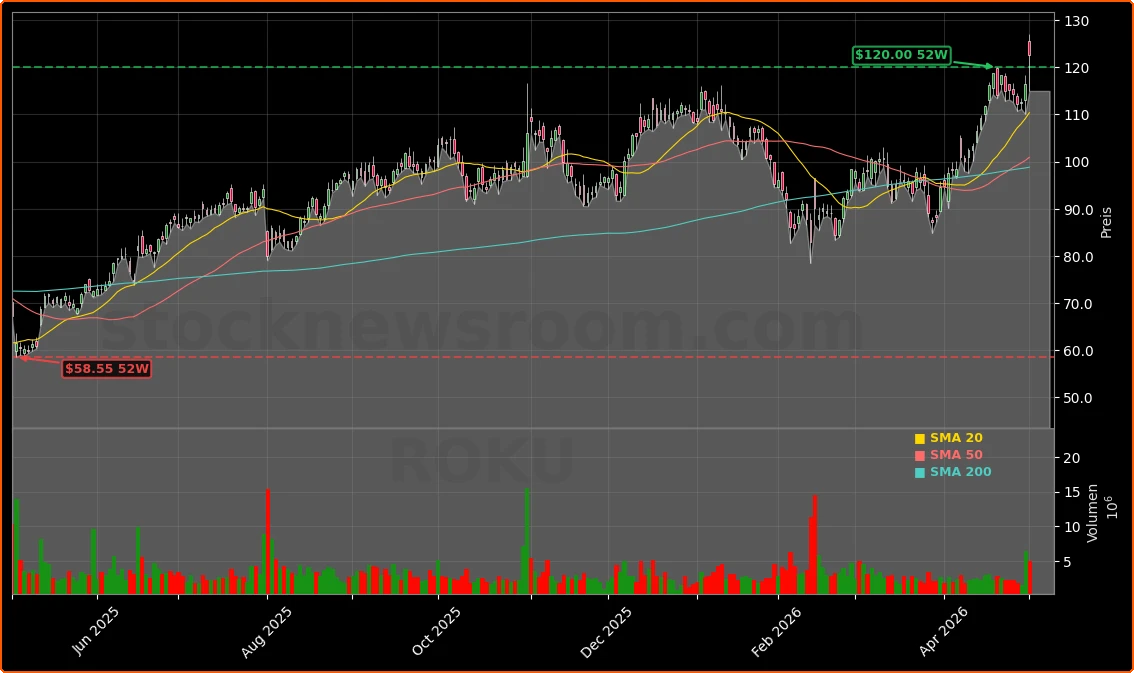

Technically, ROKU is trading well above its 20‑day and 100‑day moving averages, having broken into new 52‑week high territory in late April before the latest pullback to the $120s. Key support appears near $108, while resistance zones cluster around the mid‑$120s to high‑$120s, where traders will watch whether buyers can sustain the uptrend. For long‑term shareholders, the core thesis hinges on Roku turning its CTV scale—over 100 million households—into durable ad pricing power, much as NVIDIA did in GPUs and Tesla in EVs within their respective niches.

Related Coverage: What about insider selling?

Investors focused on the behavioral side of Roku Earnings can find a deeper dive into recent executive share sales in “Roku Insider Selling +2.3% Warning As Executives Cash Out”. That analysis examines whether the latest 10b5‑1 plan disposals by top management are routine portfolio moves or a potential yellow flag as the stock rallies. It also weighs insider behavior against the company’s strengthening fundamentals and growing buyback capacity, helping readers decide how much weight to give these signals in their own risk management.

Overall, Roku Earnings underscore a business that is finally scaling profitably, with advertising and subscription growth outpacing modest usage gains and offsetting hardware softness. For U.S. investors, the combination of raised guidance, broad‑based analyst upgrades, and deepening CTV moat keeps Roku on the radar as a higher‑beta growth play. The next quarterly report will show whether the company can sustain this momentum and turn today’s premium valuation into a long‑term advantage.