Are Seagate Earnings signaling the start of a long AI-driven storage supercycle or just a spectacular spike in sentiment?

Why did Seagate stock jump so sharply?

Wall Street is reacting to a near-perfect combination: accelerating growth, rising margins and a bullish AI narrative. In its latest quarter, Seagate Technology Holdings plc posted revenue of about $3.11 billion, up roughly 44% year over year and well ahead of consensus estimates around $2.95 billion. Adjusted earnings per share came in at $4.10, beating expectations by more than half a dollar.

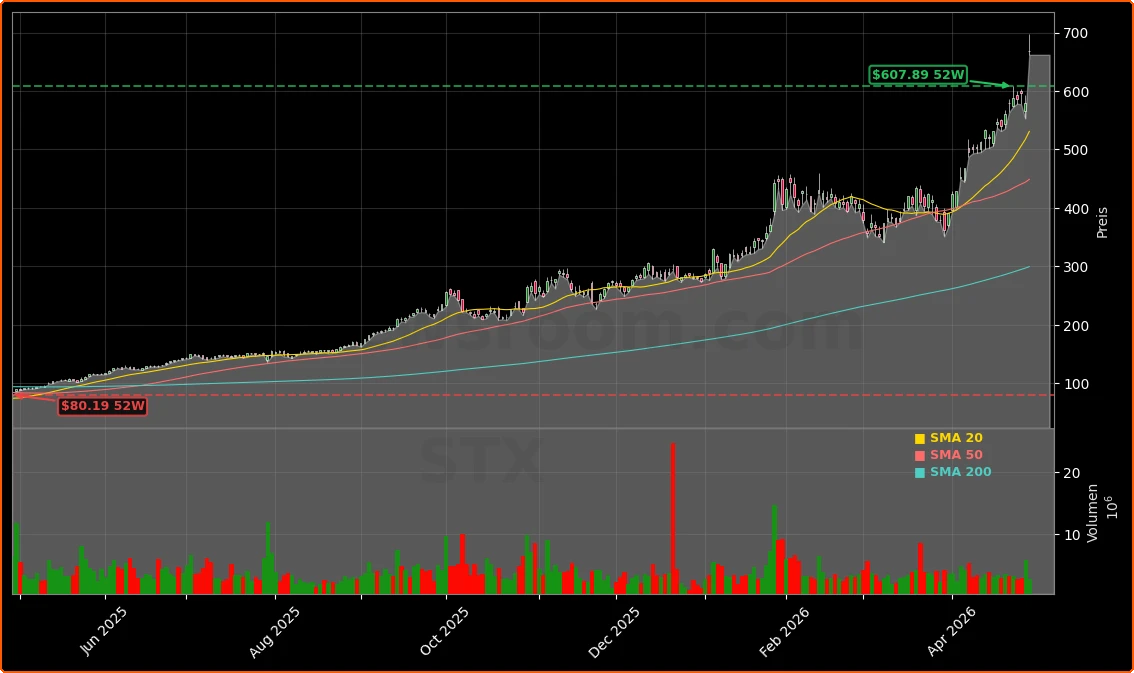

The beat matters because Seagate is no longer just recovering from a cyclical downturn; it is showing signs of a structural upswing driven by AI data center demand. The stock, which has already surged more than 100% year to date, traded near a record area around the high-$600s after the report. Even after a prior-day pullback that left the stock a few percent below its 52-week high, Wednesday’s intraday gain of more than 16% underlines how aggressively traders are repricing the AI storage story.

Cash generation was equally impressive. Seagate reported about $1.1 billion in operating cash flow and roughly $953 million in free cash flow, using the strength to pay down $641 million of debt while still returning $191 million to shareholders through dividends and buybacks.

What do Seagate Earnings say about AI demand?

Management tied the beat squarely to AI workloads. CEO Dave Mosley highlighted surging demand for high-capacity hard disk drives (HDDs) used in training and storing large language model datasets. While GPUs from players like NVIDIA crunch the numbers, HDDs remain the most cost-efficient way to store petabytes of data for cloud providers such as Amazon, Microsoft and Google.

The industry backdrop is unusually favorable. Major HDD manufacturers have kept a tight lid on capacity additions, creating what Bank of America describes as an oligopolistic market with limited new entrants and meaningful pricing power. With demand from AI data centers now outpacing supply, Seagate is benefiting from higher average selling prices and richer gross margins.

That strength showed up in the outlook embedded in the latest Seagate Earnings. The company lifted its long-term annual revenue growth target from “low to mid teens” to at least 20%, effectively telling investors that AI is turning mass-capacity storage into a multi-year secular growth story rather than a short-cycle spike.

How bullish is Seagate’s new guidance?

For the current quarter, Seagate guided to revenue of around $3.45 billion, plus or minus $100 million, with non-GAAP EPS of about $5.00, plus or minus $0.20. Those numbers are comfortably ahead of what Wall Street was modeling heading into the release and imply further margin expansion as volumes scale.

On a full-year basis, Seagate reported fiscal 2025 revenue of roughly $9.10 billion, up 39% year over year, but the bigger story is what comes next. The upgraded growth outlook signals that the company expects AI-related orders to remain strong even if more traditional enterprise and PC storage markets stay choppy. Investors looking at Seagate alongside AI beneficiaries like NVIDIA or hyperscale cloud providers can now see storage as a critical, and increasingly scarce, piece of the infrastructure stack.

Importantly, the balance sheet is improving as earnings ramp. Paying down debt while funding capex for next-generation platforms such as its HAMR-based Mozaic 4+ drives should give Seagate more flexibility to invest through the cycle and defend share against Western Digital and Toshiba.

What are analysts saying after the beat?

Wall Street strategists quickly moved to catch up with the new reality implied by Seagate Earnings. Morgan Stanley raised its Seagate price target to $767 from $582 and kept an Overweight rating, citing stronger-than-expected pricing power, gross margin upside and the durability of AI-driven data growth. Mizuho also boosted its target to $700 after the report, pointing to Seagate’s execution in high-capacity cloud drives and the potential for earnings to compound as utilization improves.

Bank of America is similarly constructive, having lifted its target earlier to $605 with a Buy rating based on sustained data center demand for mass-capacity storage. Its bullish scenario suggests Seagate’s earnings could nearly double over the next few years if AI infrastructure spending remains elevated.

Not every trading session has been one-way up. Ahead of the earnings release, Seagate shares slipped 3–4% as part of a broader semiconductor selloff driven by anxiety around future AI budgets and geopolitical risks. But the strength of the latest Seagate Earnings and guidance appears to have overridden those macro jitters for now, with investors rewarding companies that can turn AI hype into tangible cash flow.

How does Seagate stack up against US peers?

For US investors comparing choices across the AI hardware spectrum, Seagate now looks better positioned than many traditional chip names whose valuations already bake in very aggressive growth. Storage peer Western Digital has also rallied hard on the AI narrative, but Seagate’s cleaner focus on mass-capacity HDDs and early ramp of HAMR technology give it a differentiated edge.

The move echoes past inflection points in other hardware leaders. Just as Tesla monetized a structural shift to EVs and Apple captured the smartphone supercycle, Seagate is trying to harness the storage supercycle created by AI. If hyperscalers continue to invest heavily in data centers while supply remains disciplined, hard drives could become a critical bottleneck — and a profit engine — for years.

That said, investors should watch for signs of demand normalization or aggressive capacity additions by rivals that could erode pricing power. Any sustained slowdown in AI investment or a sharp rotation out of high-multiple tech could also inject volatility into STX, which has already climbed several hundred percent in the last 12 months.

Related Coverage

For a deeper dive into how much optimism is already embedded in the stock, readers can review our prior analysis, “Seagate Earnings: -2.8% Rally Warning Before Next Print”. That piece examined whether a sevenfold AI-fueled rally had priced in perfection ahead of this latest report and outlined the key risks if Seagate failed to deliver.

In summary, the latest Seagate Earnings confirm that AI-driven storage demand is translating into faster growth, fatter margins and rising cash flow for Seagate Technology Holdings plc. For US investors seeking exposure to the infrastructure behind large language models, Seagate now sits alongside GPU and cloud leaders as a core AI beneficiary. The next few quarters will show whether management can sustain 20%+ growth, but for now the trend is firmly in Seagate’s favor.