Can the latest ServiceNow Forecast and AI ambitions really justify the stock’s premium valuation after a brutal 2026 selloff?

Is ServiceNow Forecast enough to offset the selloff?

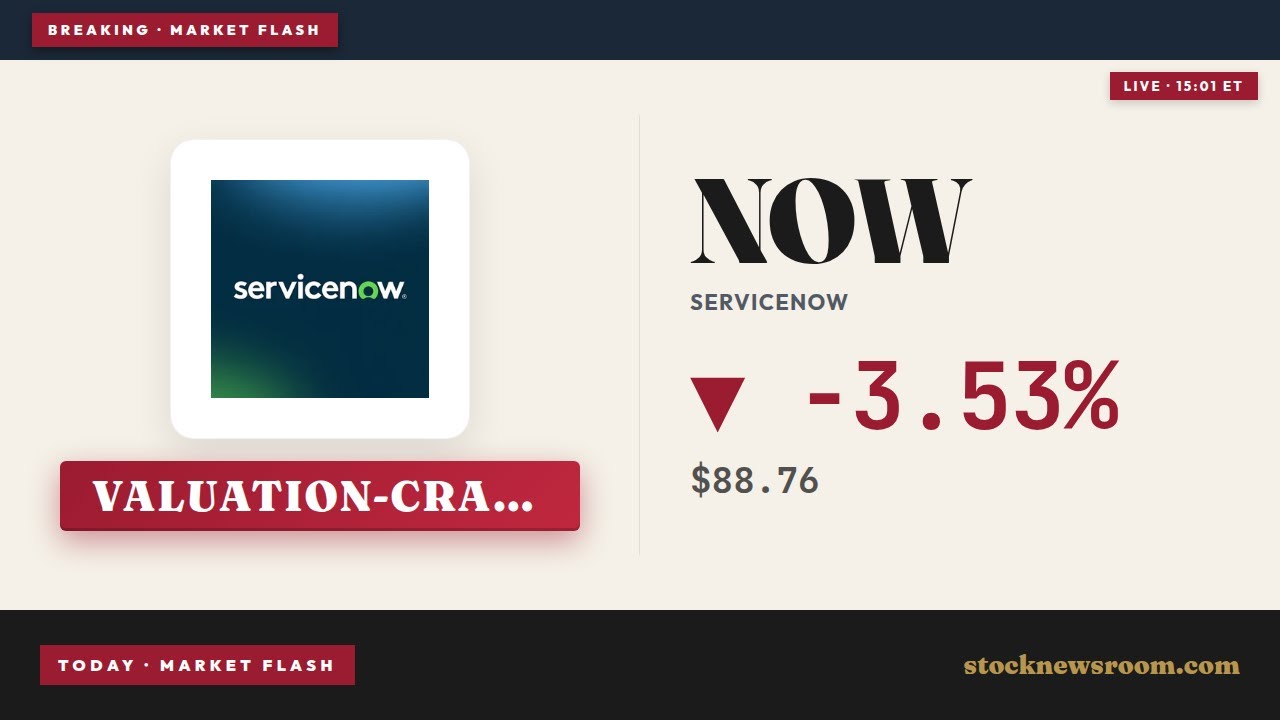

ServiceNow, Inc. shares changed hands at about $88.82 on Wednesday, down roughly 3.5% on the day and deep in negative territory year to date. The stock has dropped more than 40% in 2026 as concerns over software multiples and slowing growth weighed on high‑beta cloud names across the NASDAQ and S&P 500. Against that backdrop, the new ServiceNow Forecast from Bernstein stands out: analyst Peter Weed raised his price target to $236 from $226 while maintaining a neutral stance on the stock.

Weed’s call underscores the core tension around ServiceNow today. On one hand, the company is pushing an ambitious long‑term framework that leans heavily on expanding margins and accelerating free cash flow, bolstered by its AI platform and a fresh partnership with Anthropic. On the other, the same framework anchors expectations for subscription revenue in 2030 that imply growth slowing into the mid‑teens, a pace some investors see as incompatible with a premium software valuation.

How does ServiceNow make its AI case?

Under CEO Bill McDermott, ServiceNow, Inc. positions its platform as an “AI control tower” for enterprise workflows, competing in the same broad AI‑infrastructure narrative that powers names like NVIDIA and Apple. In Q1 2026, ServiceNow delivered subscription revenue of roughly $3.67 billion, up about 19% year over year in constant currency. Operating margin came in around the low 30s, with free cash flow margin in the mid‑40s, metrics that rank the company among the more profitable large‑cap software names.

AI is central to the ServiceNow Forecast. Management recently raised its 2026 revenue goal for its Now Assist AI products from $1 billion to $1.5 billion, citing strong traction in so‑called agentic AI use cases. Large customers are scaling fast: the number of clients spending over $1 million annually on the platform grew more than 130% year on year. The rapid integration of Moveworks into ServiceNow’s Employee Works module in under three weeks is held up as proof that the platform can move quickly in a fiercely competitive AI landscape that includes NVIDIA on the hardware side and workflow rivals embedded in the broader enterprise stack.

What exactly is Bernstein’s ServiceNow Forecast?

Bernstein’s detailed ServiceNow Forecast hinges less on explosive top‑line growth and more on a significant shift in profitability. The firm highlights a revised long‑term model in which ServiceNow targets a Rule of 60‑plus by 2030, meaning the sum of revenue growth and free cash flow margin could exceed 60%. Compared with expectations for 2025, free cash flow margins are projected to rise by roughly 900 basis points. The company also plans to reduce stock‑based compensation to under 10% of revenue by 2029, a key concern for institutional investors focused on dilution.

However, the same document that underpins Bernstein’s optimistic ServiceNow Forecast also “feeds the bears.” Management’s new 2030 subscription revenue target of $30 billion implies growth decelerating toward the mid‑teens as the decade progresses. After years of 20%‑plus expansion, that glide path has sparked debate over whether ServiceNow can sustain anything close to its historic valuation multiples. With the stock now trading around 22x forward earnings and roughly 55x trailing earnings, the question is whether investors will reward margin gains enough to compensate for slower growth.

How does ServiceNow stack up against U.S. tech peers?

For U.S. investors comparing opportunities across large‑cap tech, ServiceNow now screens more like a mature, cash‑generative software name than a hyper‑growth cloud story. While high‑flying AI beneficiaries such as Tesla and NVIDIA have seen wild swings on AI optimism, ServiceNow’s slide reflects a more classic software rerating, with the stock compressed despite robust cash generation. The consensus Wall Street price target sits around $144.88, well below Bernstein’s $236 level, signaling that many analysts are still hesitant to fully endorse the long‑term ServiceNow Forecast.

That divergence gives portfolio managers a clear decision point. Investors seeking pure AI beta may favor more cyclical chip or auto‑AI plays, while those emphasizing durability of free cash flow could see ServiceNow as a candidate for core holdings in technology allocations. Position sizing is crucial: the path to Bernstein’s target likely runs through years of disciplined execution on margins rather than near‑term upside from a single earnings print.

Related Coverage

For a deeper dive into how AI optimism could re‑rate the stock, investors may want to read ServiceNow Forecast +60% Upside: AI Rally Warning for Bears, which explores whether the current valuation already discounts much of the potential AI tailwind. That analysis also contrasts ServiceNow’s risk‑reward with other enterprise software leaders and highlights what a renewed AI rally could mean for long‑term shareholders.