Will the upcoming UnitedHealth Earnings report be strong enough to rescue the stock from a mounting FTC regulatory crackdown?

Why Are Investors Focused on UnitedHealth Earnings?

The upcoming UnitedHealth Earnings release is expected to provide key insights into the financial health of the largest US health insurer. Wall Street analysts expect the company to report quarterly earnings of $4.85 per share, representing a notable increase from the $4.08 per share reported in the same period last year. On the revenue front, the consensus estimate stands at approximately $110.77 billion to $110.82 billion, compared to the $111.62 billion recorded in the prior-year quarter.

Historically, UnitedHealth Group Incorporated has demonstrated strong financial resilience, beating consensus earnings-per-share estimates in three consecutive quarters. In its most recent quarterly report, the company posted an EPS of $7.23, outperforming expectations of $6.56 by 0.10%, while revenue reached $111.72 billion. Investors will closely monitor Medicare Advantage membership trends and pricing commentary, which serve as crucial indicators for future growth.

How Do Analysts Rate UnitedHealth Group?

Ahead of the crucial UnitedHealth Earnings announcement, several major Wall Street investment firms have updated their outlook on the stock. Optimism remains high among institutional analysts, who are raising their price targets in anticipation of the financial disclosure. Keybanc analyst Matthew Gillmor maintained an Overweight rating on the stock and raised the price target significantly from $400 to $475. Similarly, David Macdonald of Truist Securities maintained a Buy rating, boosting his price target from $440 to $480. Meanwhile, TD Cowen adjusted its stance, maintaining a Hold rating while raising its price target to $430.

Currently, the stock carries a consensus Buy rating with an average price target of $432.63. In addition to potential capital appreciation, income-focused investors are targeting the company’s dividend yield, which currently stands at 2.18%, translating to a quarterly payout of $2.32 per share.

Will the FTC Settlement Impact Optum?

The regulatory landscape for healthcare conglomerates is undergoing a significant transformation. The Federal Trade Commission (FTC) recently reached a major settlement with Caremark, a subsidiary of CVS Health, which requires the pharmacy benefit manager (PBM) to reform its business practices. The FTC alleges that major PBMs, including CVS Caremark, Cigna’s Express Scripts, and UnitedHealth Group’s Optum, engaged in rebate-driven practices that artificially inflated the list prices of essential medications like insulin.

While Caremark agreed to a settlement that could save consumers up to $13 billion over the next decade, the FTC has temporarily withdrawn its administrative case against UnitedHealth’s Optum division to consider a proposed consent agreement. Investors are highly focused on how these regulatory adjustments will affect Optum’s high-margin pharmacy services, which are critical to offsetting any potential flatlining in the company’s core insurance business.

What Is Driving the Latest Stock Price Action?

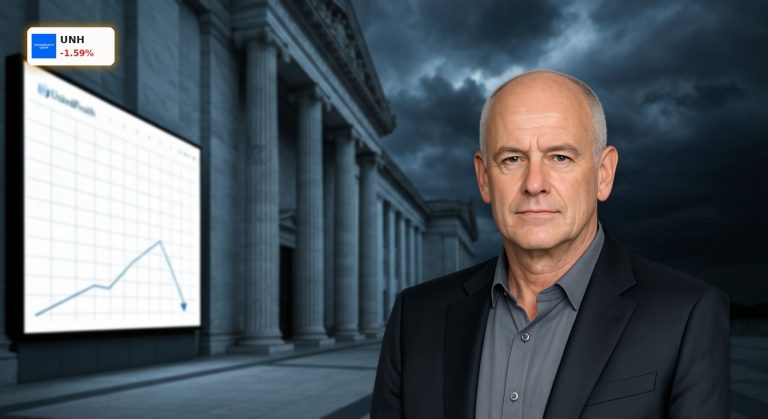

In the options market, trading activity has surged ahead of the earnings release. Investors purchased $8 million in call options compared to just $1.9 million in put options, signaling bullish expectations, though implied volatility is rising. Despite this options momentum, the stock experienced downward pressure during Wednesday’s intraday trading session, falling 1.59% to trade at $418.42, down from its previous close of $425.19. This short-term decline reflects broader market caution as traders position themselves for the upcoming financial results and analyze the potential long-term impact of the FTC’s regulatory crackdown on the PBM industry.

Related Coverage

For a deeper dive into how regulatory challenges could impact the company’s financial momentum, read our analysis on UnitedHealth Regulation: $111B Revenue Meets New Scrutiny. Additionally, to see how other healthcare giants are performing in this high-stakes environment, check out our report on Johnson & Johnson Earnings: $21 Billion Swing Ahead of Key Print.