Can UnitedHealth’s strong earnings momentum survive the growing weight of DOJ, FTC, and Medicare scrutiny?

What’s Driving UNH’s 23% YTD Rally?

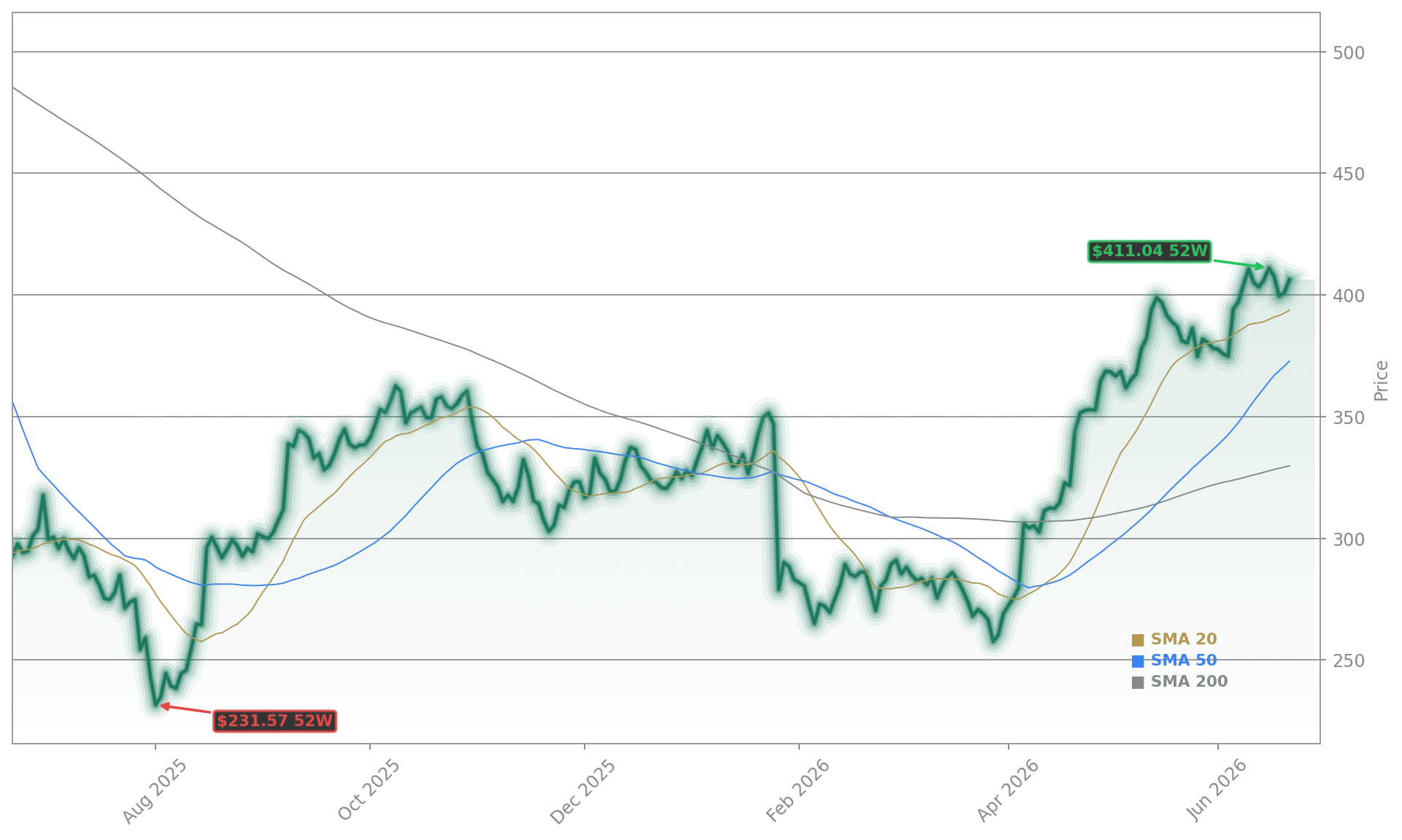

UnitedHealth Group Incorporated rose 1.34% to $406.35 on Monday, June 22, outperforming the S&P 500 and helping lift the Dow Jones Industrial Average while the NASDAQ lagged. The rally reflects strong Q1 2026 fundamentals: $111.72 billion in revenue (+2% YoY), adjusted EPS of $7.23 (beating consensus by $0.62), and a medical care ratio (MCR) improvement to 83.9% — a 90-basis-point gain. Management raised full-year adjusted EPS guidance to greater than $18.25. JPMorgan responded by raising its price target to $466 from $420 and maintaining an Overweight rating — citing upgraded healthcare services models and confidence in UNH’s long-term earnings power. Yet the rally comes amid a stark institutional retreat: Berkshire Hathaway fully exited its UNH stake in Q1 2026, Appaloosa Management meaningfully reduced its position, and SGA Global Growth Fund sold its entire holding on June 17.

How Serious Is the UnitedHealth Regulation Overhang?

UnitedHealth Regulation isn’t theoretical — it’s active, multi-front, and unresolved. The Department of Justice’s criminal and civil probe into Medicare Advantage billing practices remains open with no published timeline for resolution. Simultaneously, the Federal Trade Commission reached a procedural settlement on June 12 with OptumRx and Emisar Pharma Services over alleged anticompetitive rebating in insulin pricing — a matter now under consent-agreement review. Compounding pressure, a June 12 Office of Inspector General (OIG) report documented UnitedHealth Medicare Advantage post-hospital care denial rates between 51% and 80%, far exceeding peer averages. Fairview Health Services announced it will stop accepting UnitedHealthcare Medicare Advantage plans in 2027 — affecting over 11,000 patients. These developments directly threaten the MCR, UNH’s most sensitive profitability metric and the very lever that drove its Q1 margin recovery.

Are Institutional Sellers Right to Exit?

Berkshire Hathaway’s full exit, alongside Appaloosa and Chase Coleman’s reductions, signals more than portfolio trimming — it reflects a divergence in risk assessment. While UNH’s 0.65 beta and 2.15% dividend yield still anchor it as a defensive holding, the exits coincide with deteriorating Medicare Advantage fundamentals. Preliminary 2027 Medicare rates came in below expectations, and Optum Health’s Q1 operating earnings ($3.3 billion) remain 15% below the prior-year $3.89 billion — despite recovery efforts. Analysts maintain a bullish consensus: 22 buy or strong buy ratings versus one sell, with an average target of $407.38. But as one strategist noted, ‘The bull case rests on assumptions Berkshire and Tepper rejected.’ With forward P/E at 22x and quarterly revenue growth at just 2%, valuation discipline is tightening.

How Does UNH Compare to Peers in This Environment?

UnitedHealth Group Incorporated stands apart from peers like Humana and CVS Health, both of which rebounded sharply in 2026 — yet face similar regulatory scrutiny. Humana’s MCR improved to 84.2% in Q1, but its Medicare Advantage membership growth stalled. CVS’s Aetna unit faces its own DOJ probe into pharmacy benefit manager (PBM) practices. Meanwhile, NVIDIA and Apple — both in the S&P 500’s top decile for YTD returns — benefit from structural tailwinds absent in healthcare: AI infrastructure demand and ecosystem pricing power. UNH’s 22x P/E looks expensive next to the S&P 500’s 20.4x, especially with earnings growth decelerating. In contrast, Merck and Johnson & Johnson trade at lower multiples despite comparable regulatory exposure — underscoring investor preference for pharma over payer risk.

What’s Next for UnitedHealth Group Incorporated?

With jury selection in the Brian Thompson murder trial set for September and opening arguments expected in November, the human dimension of UNH’s crisis remains visible — yet market focus stays on regulatory and financial levers. The next catalyst is the final 2027 Medicare Advantage rate announcement, expected in August. If rates land below preliminary guidance, pressure on MCR and 2027 EPS estimates will intensify. Meanwhile, Optum Health’s recovery trajectory — critical to UNH’s earnings diversification — remains uncertain. JPMorgan’s $466 target assumes continued margin expansion; a sustained MCR above 84% would support it. But as long as UnitedHealth Regulation remains unbounded, the stock’s upside will be capped — and its downside asymmetric.

Related coverage: A fresh Bank of America buy call triggered a 5.9% surge in UNH shares just weeks ago — can Wall Street’s optimism overcome regulatory fatigue? Meanwhile, Pfizer’s CFO transition sparked a 2.9% selloff — highlighting how leadership changes amplify investor anxiety in highly regulated sectors. The contrast underscores UNH’s unique challenge: it must navigate not just earnings delivery, but a rapidly shifting regulatory landscape where every denial, rebate, and rate decision carries market-moving weight.

UnitedHealth Group Incorporated’s turnaround is real — but it’s fragile. For U.S. investors, the key question is whether UnitedHealth Regulation will remain a drag or become a catalyst for structural reform and renewed trust. The next quarterly earnings report will test whether margin gains are sustainable — or merely a pause before the next wave of UnitedHealth Regulation scrutiny. For long-term portfolios, UNH remains a high-conviction healthcare holding — but one demanding active monitoring, not passive ownership.