Has Wall Street overreacted to Zscaler’s long-term guidance reset, or is this rebound the start of a fresh rerating?

Why did Zscaler rebound so sharply?

Zscaler, Inc. staged a powerful recovery Monday after Guggenheim upgraded the stock to Buy from Neutral and set a $214 price target. The firm argued that valuation now offers an attractive entry point for a category leader in zero-trust security and AI-linked cybersecurity, helping reverse some of the damage from last week’s post-earnings selloff. Barron’s highlighted that Wall Street is increasingly willing to buy into the company’s “trust me” AI narrative, while Seeking Alpha noted the stock rose as much as 10% on the upgrade.

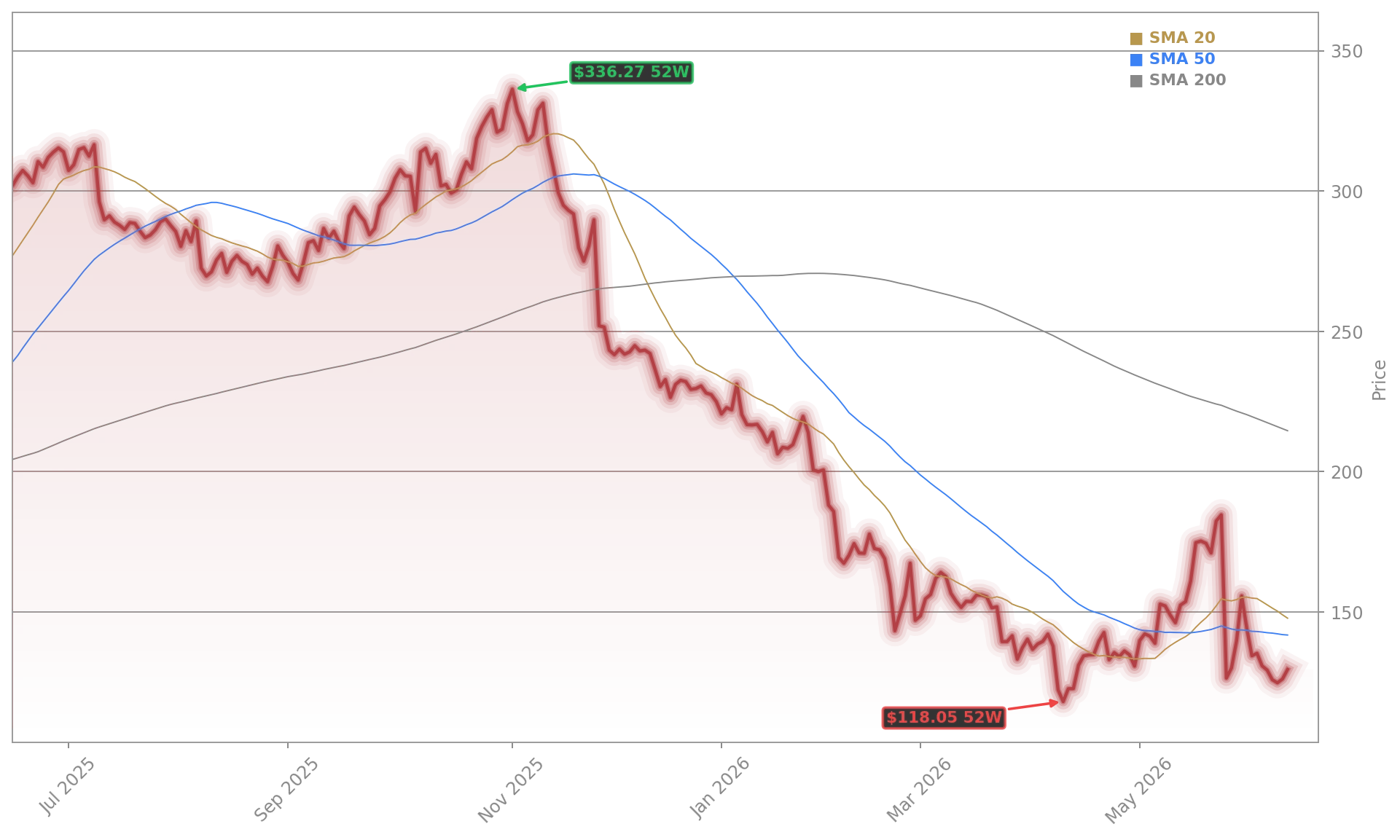

The rebound matters because it came just days after one of the stock’s sharpest drops in years. Investors had punished shares after management outlined a fiscal 2027 annual recurring revenue growth range of 16% to 17%, below what many on Wall Street had expected. A lower free cash flow margin outlook for fiscal 2026, tied to higher capital expenditures, added to concerns that near-term profitability will be weaker than previously modeled.

What changed in the Zscaler Forecast?

The core issue in the Zscaler Forecast is not whether the latest quarter was weak. Fiscal third-quarter results were solid, with revenue growth around 25% and management also lifting parts of its fiscal 2026 guidance. The problem was forward visibility. Investors focused on the preliminary fiscal 2027 ARR outlook and on a revised free cash flow margin target of 22.8% to 23.3%, down from the prior 26.5% to 27% range.

That shift triggered a wave of analyst resets. Evercore ISI analyst Peter Levine downgraded Zscaler to In Line from Outperform after the earnings report, reflecting a more cautious stance on the company’s growth trajectory. Other firms also lowered price targets, though the broader analyst base has not fully turned negative. TradingView data showed the average 12-month target fell to $197.22, while the consensus rating remained Buy. That leaves the Zscaler Forecast caught between short-term skepticism and longer-term confidence.

How does Zscaler compare with rivals?

For US investors, valuation is becoming the key counterargument to the bearish narrative. Zscaler now trades at a lower price-to-sales multiple than major cybersecurity peers such as CrowdStrike and Palo Alto Networks, even though it is still producing double-digit growth and remains a leader in cloud-native security. That relative discount has fueled the idea that the selloff may have gone too far.

There is also a useful precedent. Morgan Stanley downgraded CrowdStrike in 2025 on valuation concerns, and HSBC downgraded Palo Alto Networks later that year after an earnings report that failed to impress. Both stocks ultimately recovered strongly. Zscaler is not guaranteed to follow the same path, but Monday’s rally suggests investors are willing to revisit the story when sentiment becomes too pessimistic. In a market still rewarding AI and software leaders, comparisons with names like NVIDIA and Apple also keep attention on cybersecurity platforms that could benefit from enterprise AI adoption.

Can Wall Street move past the legal noise?

Another overhang is the burst of shareholder law firm announcements following the post-earnings plunge. Those headlines can pressure sentiment in the near term, but they do not change the central investment debate, which remains focused on growth durability, sales execution, and cash generation. The more important question for institutions is whether increased spending today can support stronger platform expansion later.

Related Coverage: Investors tracking the latest reset in sentiment should also read Zscaler Earnings: $850M Beat but Outlook Warning Hits. That report breaks down how a headline earnings beat was overshadowed by weaker forward signals, helping explain why the stock sold off so violently before Monday’s rebound. It also offers useful context for how the current Zscaler Forecast debate developed so quickly.

The latest move shows the Zscaler Forecast is now a battle between downgraded growth expectations and a cheaper valuation that some analysts see as compelling. For investors, the next few quarters will need to prove that higher spending can support durable ARR growth and rebuild confidence in free cash flow. If management executes, Monday’s rebound could mark the start of a broader recovery rather than just a relief rally.