Can CrowdStrike justify its latest surge as analysts raise targets and a new Germany partnership sharpens the growth story?

Why is CrowdStrike Forecast improving now?

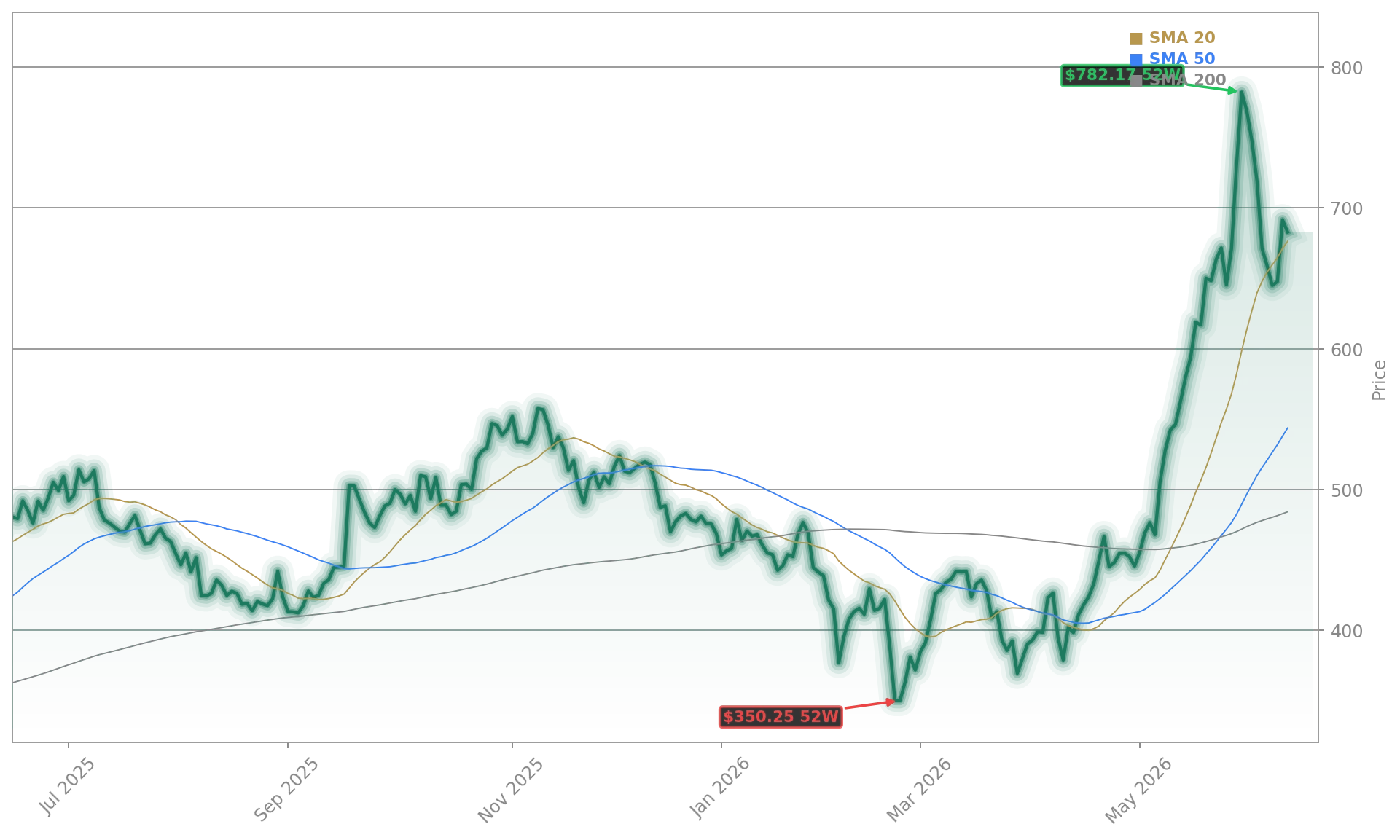

CrowdStrike Holdings, Inc. is back at the center of Wall Street’s software leadership trade after a powerful session that pushed CRWD to $650.11, up from a previous close of $615.00. The after-hours move to $649.44, down 0.10%, suggests investors are holding gains rather than rushing to take profits. This matters because the stock has rallied far above key moving averages and is now trading near the upper end of recent analyst targets.

The near-term driver is simple: analysts are becoming more bullish just ahead of fiscal first-quarter results due June 3. Stifel lifted its target to $660 from $480 and kept a Buy rating after reseller checks showed a 3-to-1 bullish skew on fiscal 2027 growth. KeyBanc previously moved to $700, while Barclays has an Overweight rating with a $650 target. TD Cowen reiterated Buy and raised its target to $625, and BTIG has also been positive at $621. The outlier remains DZ Bank, which cut the stock to Sell with a $500 target, underscoring how split the Street still is on valuation.

How important is CrowdStrike’s Germany deal?

The company’s new partnership with SVA System Vertrieb Alexander GmbH adds a meaningful international angle to the CrowdStrike Forecast. SVA will standardize the AI-native Falcon platform for Germany’s public sector, enterprises, and midmarket customers. That broadens CrowdStrike’s route to market in Europe and strengthens the case that Falcon is becoming a deeper platform sale rather than a point product.

The strategic value is in consolidation. Falcon combines endpoint, identity, cloud, next-gen SIEM, and data protection with AI-driven automation, which plays directly into customer demand for fewer vendors and faster security response. CrowdStrike also plans joint growth efforts through AWS Marketplace, Stackit, and Google Cloud Marketplace, extending distribution and potentially accelerating adoption. For U.S. investors, that matters because international expansion can support durable ARR growth even if domestic comparisons become tougher later this year.

The broader software tape has also improved, with cybersecurity names benefiting from renewed confidence that AI is increasing demand for defense-oriented software rather than replacing it. That narrative has helped names like NVIDIA by association in the AI trade, while also supporting peers such as Palo Alto Networks and Fortinet.

Can CrowdStrike keep outrunning rivals?

Competitive positioning remains central to the bull case. CrowdStrike exited fiscal 2026 with $5.25 billion in ending ARR and $4.81 billion in full-year revenue, up 22% year over year. Falcon Flex ARR reached $1.69 billion, up 120%, highlighting growing customer commitment to the platform model. That momentum is why some investors currently prefer CrowdStrike over Palo Alto Networks in the cybersecurity space.

Still, valuation is the main risk to any CrowdStrike Forecast. Bears point to a forward earnings multiple above 100x, competition from Microsoft Defender, and lingering sensitivity around the July 2024 outage. Even with that backdrop, the Street remains overwhelmingly favorable, with far more Buy ratings than Holds and effectively no broad bearish consensus outside a few valuation-focused calls. Comparisons with large-cap software and AI winners like Microsoft, Amazon, and Alphabet also show why investors are willing to pay for category leadership when growth remains visible.

Related Coverage: Earlier this month, stocknewsroom.com examined how a fresh Gartner leadership nod could reinforce CrowdStrike’s AI security narrative in CrowdStrike Gartner win: CRWD +3% AI Surge on new lead. That piece adds useful context for investors tracking whether product leadership and market recognition can keep fueling premium multiples into the next leg of the rally.

The current CrowdStrike Forecast is supported by stronger channel checks, a new Germany distribution partnership, and a rising stack of bullish price targets. For investors, the next test is clear: June 3 earnings must confirm that Falcon demand and ARR momentum are strong enough to justify a stock already trading near the top of Wall Street targets.