Did Zscaler Earnings just expose a temporary sales hiccup, or the start of a deeper slowdown in cybersecurity growth?

Why are Zscaler Earnings hitting shares?

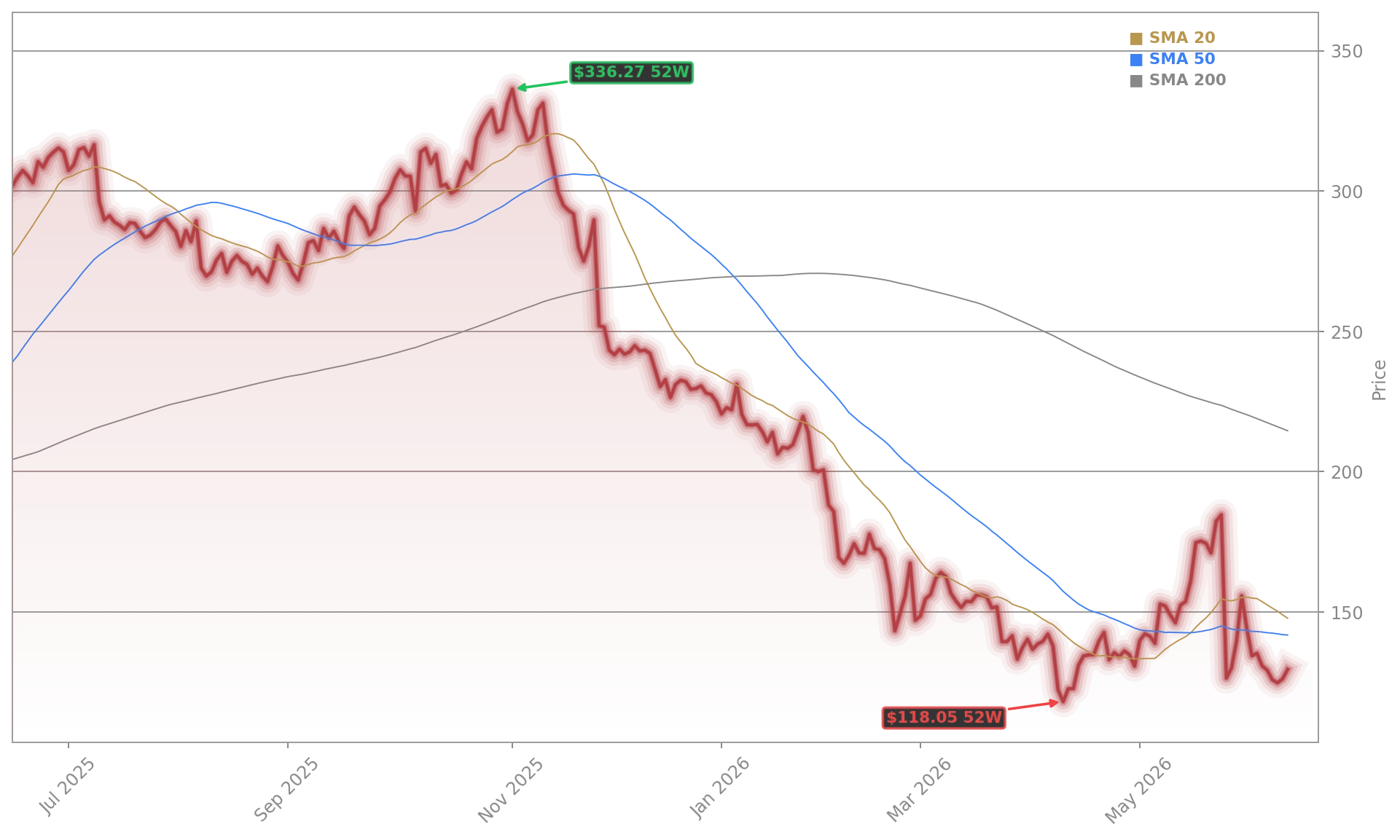

Zscaler, Inc. is under pressure Wednesday morning after posting better-than-expected fiscal third-quarter results while offering a softer-than-expected outlook for the next quarter. The stock was indicated at $139.33 in pre-market trading, down 24.52% from the prior close of $146.24, even though shares also showed a separate quote of $184.60 in current market data. The key issue for investors was not the quarter that ended, but the quarter ahead.

Zscaler reported revenue of $850.48 million, up 25% year over year and ahead of Wall Street expectations near $835 million. Adjusted earnings came in at $1.08 per share, topping the consensus estimate of $1.01. Still, the company guided fiscal fourth-quarter revenue to $875 million to $878 million, roughly in line at the low end but shy of the Street’s $878.53 million target.

That narrow miss mattered because Zscaler had rallied sharply into the print. After a roughly 35% to 45% run over the past month, expectations had become elevated, leaving little room for caution in the outlook.

What changed at Zscaler?

The deeper concern in Zscaler Earnings was management’s explanation for the conservative forecast. Chief Financial Officer Kevin Rubin said two sales leaders left the company at the end of the third quarter, creating go-to-market disruption. Management said it was taking a prudent approach to guidance during that transition.

That comment reinforced fears that demand is not collapsing, but execution may be getting harder. It also helps explain why commentary from market watchers quickly shifted from the quarter’s headline beat to concerns about sales deceleration. For growth software names, especially in cybersecurity, investors often reward acceleration and punish even modest signs of slowing momentum.

The company also previewed fiscal 2027 with revenue and annual recurring revenue growth expected to slow to about 16% to 17%. That is still healthy by broader software standards, but it marks a visible step down from the pace investors have been accustomed to from premium cybersecurity names.

Can AI keep Zscaler competitive?

Zscaler is trying to offset those concerns with a stronger AI security story. Chief Executive Officer Jay Chaudhry said the company is positioned to be a cybersecurity platform for the AI era, and management highlighted more than $100 million in bookings for its AI Protect offering. Recent moves, including the Symmetry Systems acquisition and Project AI-Guardian launch, are meant to deepen data security and AI governance capabilities.

That strategy matters because Zscaler is competing for investor attention against larger technology leaders like Microsoft, Palo Alto Networks, and CrowdStrike, while AI spending continues to pull capital toward names such as NVIDIA and Amazon. The problem for Zscaler is that Wall Street wants proof these AI products can lift growth fast enough to justify a still-premium software valuation.

Before the report, analysts remained broadly constructive. Benzinga noted firms including Cantor Fitzgerald and Guggenheim had positive views heading into earnings, while Barchart highlighted a Street average target above current levels. Even so, Zscaler Earnings show how quickly sentiment can reset when guidance misses by even a small amount.

What should investors watch next?

Investors now need to see whether the sales transition is brief or the start of a broader slowdown. The next few months will likely center on billings, annual recurring revenue, and whether AI-related offerings meaningfully expand deal sizes. If execution stabilizes, this sell-off may look overdone; if growth keeps decelerating, valuation pressure could continue.

Related Coverage: Investors looking for a broader valuation perspective can read Zscaler Earnings +26% Surge: Is Wall Street Overreacting?. That earlier analysis examined whether strong growth and a still-expanding security platform were enough to balance a lower multiple. In light of the latest report, that debate looks even more relevant as Wall Street weighs strong fundamentals against softer forward guidance.

At the end of the third quarter, 2 sales leaders departed the company. We are taking a prudent approach to our guidance during this transition.— Kevin Rubin

Zscaler Earnings delivered the classic growth-stock dilemma: a strong quarter, but not enough confidence about what comes next. For investors, the next catalyst is whether management can restore sales momentum and turn its AI security push into faster, more durable growth.