Can Workday prove its AI push will accelerate growth without turning a margin story into a spending problem?

Why are Workday Earnings so important now?

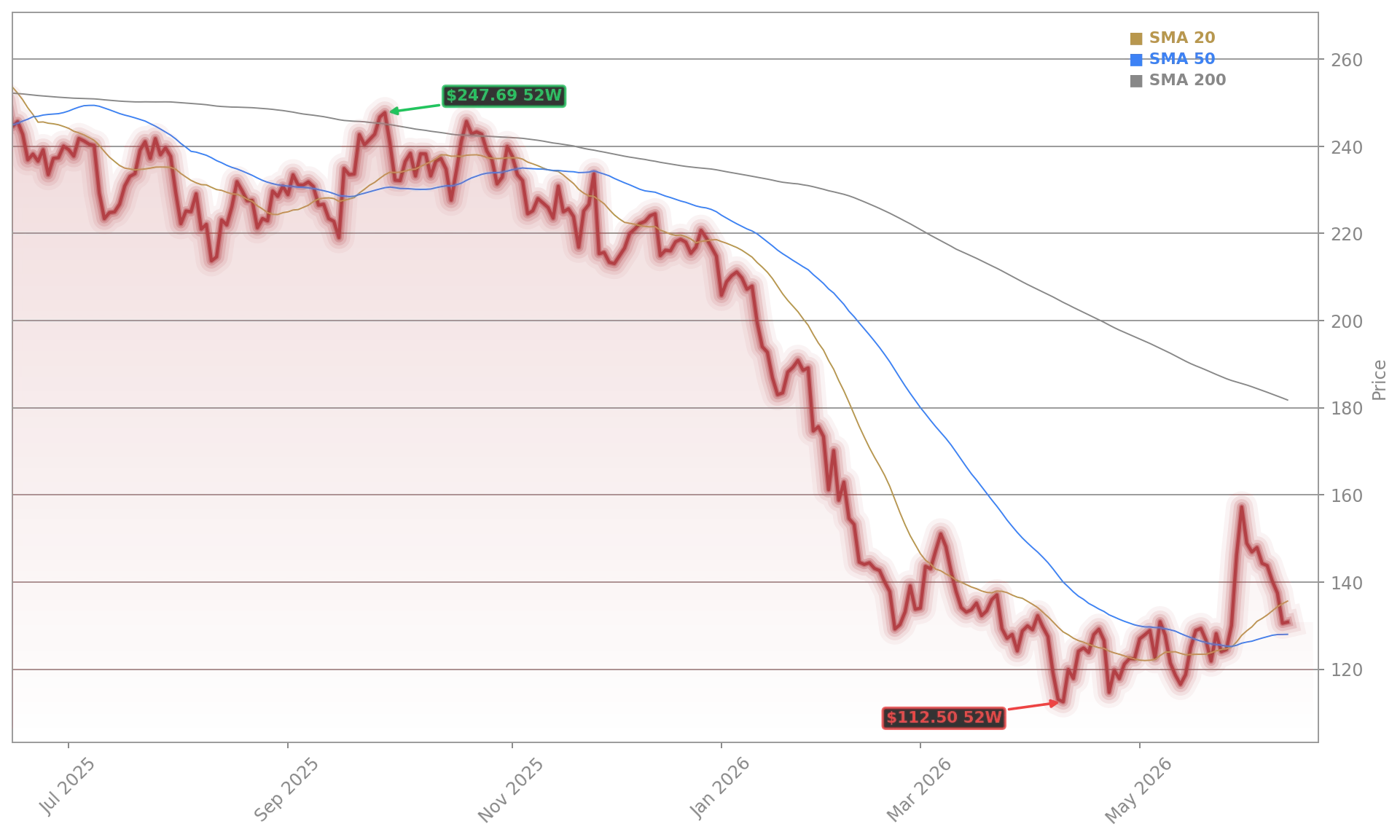

Workday, Inc. heads into its report with sentiment fragile across enterprise software. Shares were trading at $121.31 Thursday, versus a previous close of $124.10, as investors digested a broader selloff that also hit Salesforce, ServiceNow, Adobe, and Atlassian. The setup for Workday Earnings is less about whether the company can meet near-term estimates and more about what management says on growth durability.

Jefferies said expectations heading into the print appear reasonable, with subscription revenue growth around 13% and current remaining performance obligations, or cRPO, also seen in line. But the firm maintained a Hold view, highlighting execution risk, an still-evolving AI roadmap, and limited room for upside to near-term estimates. Investors are also watching whether Workday can still support its fiscal 2028 growth target of 13% to 14% while competing against SAP and Oracle in back-office software.

Can Workday defend margins while investing?

Margins may be the biggest swing factor in this quarter’s discussion. Jefferies has flagged concern that heavier AI spending could slow operating margin expansion, even after Workday previously pointed to fiscal 2027 non-GAAP operating margin around 30%. That issue matters more because the stock has already been under pressure since founder Aneel Bhusri returned as CEO, with some investors questioning whether the company is entering a lower-growth, higher-investment phase.

The most recent reported quarter showed a stronger profitability profile than the market currently seems willing to credit. Workday posted Q4 subscription revenue of $2.36 billion, up 16%, total revenue of $2.53 billion, up 15%, and a non-GAAP operating margin of 30.6%. For the full year, subscription revenue reached $8.83 billion, while free cash flow rose 27% to $2.78 billion. Those historical figures suggest the margin base is solid, but the key question now is whether AI-related costs start to cap future expansion.

Is Workday’s AI story convincing Wall Street?

The AI narrative remains central to Workday Earnings. Management has emphasized internally developed agents over large acquisitions, while using a Flex Credits model to monetize AI consumption across its platform. In the last reported quarter, AI-related annual recurring revenue topped $400 million, with more than $100 million in new AI ACV generated in Q4, more than doubling year over year. Workday also said it delivered 1.7 billion AI actions during the full year.

That sounds encouraging, but Wall Street still wants clearer proof that AI can become a meaningful revenue driver rather than just a product enhancement story. Jefferies said AI today represents only about 4% of revenue and described adoption as still early. At the same time, the broader software group is trying to show investors that AI can lift growth, a dynamic also shaping sentiment around Microsoft, NVIDIA, and Oracle.

What else should investors watch at Workday?

Beyond AI and margins, investors will likely focus on retention, international growth, and large-deal momentum. Workday’s gross revenue retention rate has held at 97%, and its installed base remains a core strength. Management previously said expansion deals tied to AI were nearly 50% larger on average, while partner-sourced deals represented 25% of net new ACV in Q4. Still, large enterprise deal cycles have lengthened, and international growth has lagged the U.S.

Another point supporting the long-term case is shareholder interest. Hotchkis and Wiley disclosed a 5.07% passive stake in mid-May, a sign that some institutional investors see value after the stock’s steep decline over the past year. Eagle Capital Management has also argued that Workday operates below normalized margins and could benefit if founder-led execution helps reignite product development.

Related Coverage: Earlier this year, Workday Earnings: Weak 2027 Outlook Sends Stock Plummeting examined how an earnings beat was overshadowed by soft fiscal 2027 guidance and renewed AI concerns. That earlier reaction still matters now, because Thursday’s report will be judged not just on quarterly numbers, but on whether management can rebuild confidence in the medium-term growth path.

Workday Earnings now come down to a simple test: can the company prove that AI investment will strengthen growth without breaking its margin story? If management delivers clearer answers on monetization, cRPO, and spending discipline, the stock could regain footing; if not, Wall Street may stay cautious into the next quarter.

Our focus really right now is on the organic development of agents.— Aneel Bhusri

Fazit folgt.