Can a double beat on Boeing Earnings and cash flow progress really offset years of crises and keep the stock flying higher?

How did Boeing Earnings beat expectations?

The Boeing Company posted first-quarter 2026 revenue of $22.22 billion, up 14% year over year and ahead of consensus expectations near $21.9 billion. Adjusted core loss came in at just $0.20 per share, a dramatic beat versus analysts’ forecast for a $0.84 loss. On a GAAP basis, Boeing reported a small net loss of $7 million, or $0.11 per share, improving from a $31 million loss a year earlier.

The beat was driven primarily by stronger-than-expected commercial aircraft deliveries and steady growth in defense and services. Boeing handed over 143 commercial jets in the quarter, a 10% increase and its highest quarterly tally since 2018, despite lingering production and certification challenges on the 737 MAX family. That volume, combined with improved operational performance and favorable order timing, pushed margins modestly higher across several segments.

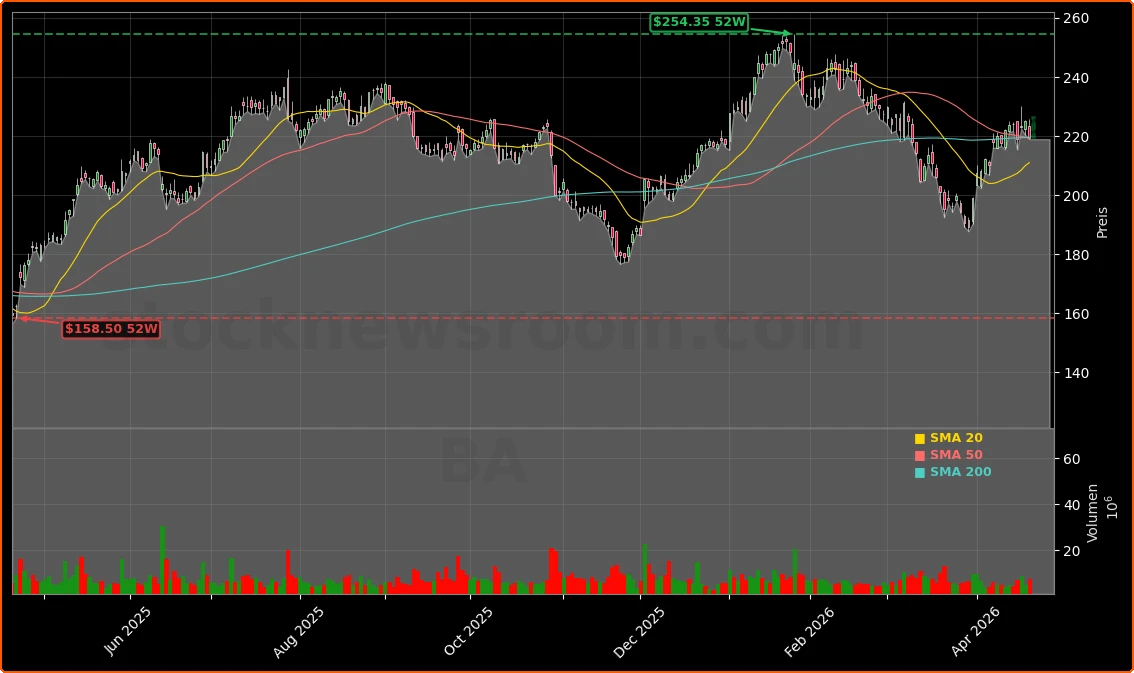

Investors responded positively in early trading. Boeing shares closed the prior session at $221.00 and recently traded around $219.16, down 2.63% on Tuesday’s close but indicated higher in pre-market action near $226.54, suggesting the stronger Boeing Earnings are being priced in before the opening bell on the NYSE.

Is Boeing finally taming its cash burn?

While the headline Boeing Earnings beat grabbed attention, Wall Street’s real focus remains cash flow. Boeing still burned through $1.45 billion of free cash flow in Q1, but that marks a substantial improvement from a $2.29 billion outflow a year earlier. Operating cash flow was nearly breakeven at negative $179 million compared with a $1.6 billion outflow in the prior-year quarter.

Management reiterated its goal of stopping the cash bleed before the end of 2026, driven by higher narrow-body and wide-body production rates, tighter discipline on fixed-price defense contracts and efficiency improvements in services. The company ended the quarter with $20.9 billion in cash and short-term investments and $47.2 billion of consolidated debt after paying down obligations, leaving it with a still-elevated but gradually improving balance sheet.

Total backlog reached a record $695 billion, including more than 6,100 commercial aircraft valued at $576 billion, plus record backlogs in defense and global services. That visibility gives investors confidence that as production stabilizes, each incremental plane delivered should translate into better cash generation. For U.S. portfolios, that transition from heavy cash burn to sustainable free cash flow is the core of any long-term Boeing thesis.

What’s driving the segment performance at Boeing?

Commercial Airplanes revenue rose 13% to $9.2 billion, though the segment still posted a loss from operations of $563 million, for a negative 6.1% margin. The 737 program is running at 42 aircraft per month, and Boeing is targeting certification of the 737-7 and 737-10 variants in 2026 with first deliveries in 2027. The 787 line is stabilizing at eight per month, and the 777X program continues progressing through FAA certification steps with first 777-9 delivery also planned for 2027.

Defense, Space & Security turned in a stronger quarter with revenue jumping 21% to $7.6 billion and operating profit climbing 50% to $233 million, reflecting higher volume and more stable execution. Boeing’s role in NASA’s Artemis II lunar mission, as well as new contracts such as the PAC-3 seeker framework and an MQ-28 Ghost Bat partnership with Rheinmetall, highlight the company’s strategic position in U.S. and allied defense, a key consideration for investors balancing cyclical commercial exposure with more resilient military demand, similar to diversified defense peers like RTX and GE Aerospace.

Global Services, often overshadowed by jets and missiles, quietly delivered another solid quarter. Revenue increased 6% to $5.37 billion while operating margins remained robust at 18.1%, supported by higher government volume and a growing installed base of Boeing aircraft worldwide. Large long-term deals, including a major landing gear exchange program with Singapore Airlines Group, reinforce services as a high-margin buffer in future downcycles.

How does Boeing stack up against U.S. industrial peers?

Boeing’s rebound comes in a broader Wall Street context where cyclical industrial and aerospace names have been rerated higher on strong order books and recovering travel demand. Jet-engine leader GE Aerospace recently guided 2026 profit toward the top of its range despite oil price risks, while defense-focused players like RTX emphasize backlog strength amid elevated geopolitical tensions. For equity investors, Boeing’s mix of commercial recovery and defense exposure positions it somewhere between pure-play airlines such as United Airlines and diversified defense groups.

Institutional appetite appears to be rebuilding. Asset managers like Eagle Global Advisors and Jones Kertz & Associates have disclosed meaningful increases to their Boeing positions in recent quarters, even as insider selling has taken place at the margin. Analysts broadly maintain a “Moderate Buy” stance with an average price target around the mid-$250s, implying upside from current levels if execution on production, safety and cash flow continues to improve.

Boeing Earnings also land on a busy day for mega-cap growth and industrial bellwethers, with Tesla set to report after the close and chip and AI leaders such as NVIDIA and Apple continuing to dominate S&P 500 earnings growth. For portfolio managers, Boeing’s more cyclical, real-economy profile offers diversification alongside tech-driven market leaders, especially as global air travel and defense spending trend higher over the long term.

Related Coverage

For a deeper dive into how geopolitical tensions could disrupt Boeing’s fragile recovery, especially around Middle East shipping lanes and energy prices, readers can explore our detailed analysis in Boeing Supply Chain Risk +3.8%: Middle East Conflict Warning. That piece examines whether supply chain strains and higher fuel costs might offset the positive momentum seen in the latest Boeing Earnings report and what that means for long-term investors.

Overall, the latest Boeing Earnings underscore that the turnaround is real but still incomplete: losses are shrinking, deliveries are climbing and backlog is at a record, yet free cash flow remains negative and leverage is high. For U.S. investors, the stock is increasingly a high-beta play on global air travel, defense spending and execution on safety and production quality. The next few quarters of Boeing Earnings will be critical in proving that the company can flip from burning cash to consistently generating it, potentially unlocking further upside as sentiment and credit metrics continue to heal.