Is Dell’s latest pullback a warning sign for the AI trade, or the kind of dip growth investors wait for?

What’s Driving Dell’s AI-Fueled Rally?

Dell Technologies Inc. is no longer just a PC vendor—it’s a critical AI infrastructure enabler. Server and storage revenue surged 42% year-over-year in Q2 2026, fueled by hyperscaler deployments and enterprise AI rollout plans. Unlike NVIDIA, whose chips power AI models, Dell integrates those chips into scalable, support-rich systems—making it indispensable for customers who need production-grade AI infrastructure yesterday. Wells Fargo analyst Aaron Rakers reiterated his Overweight rating and $505 price target, citing Dell’s ‘supply chain economies of scale’ and ‘de-leveraging execution’ as key catalysts for capital return acceleration. Evercore ISI’s Amit Daryanani lifted his target to $500 on July 8, emphasizing upside potential if AI demand continues outpacing supply constraints.

How Does the Trump Bump Fit In?

President Donald Trump’s July 6 White House launch of Trump Accounts—530A tax-deferred savings vehicles for children born 2025–2028—gave Dell Technologies Inc. a surprising visibility boost. Though unrelated to its core business, CEO Michael Dell publicly endorsed the initiative as a tool for long-term wealth building, linking it to education and entrepreneurship goals. The endorsement coincided with a 4.1% intraday pop—yet the real driver remains AI. As Investor’s Business Daily notes, Dell’s IBD Composite Rating sits at a perfect 99, and its EPS Rating is 97—both metrics reflecting accelerating earnings power, not political optics. The ‘Trump Bump’ may have accelerated entry timing, but the Dell AI Forecast rests on fundamentals.

Is Dell Outpacing the Broader Tech Sector?

Absolutely. While the NASDAQ gained 15% YTD, Dell Technologies Inc. has surged 250%—outpacing even Apple and Tesla in raw momentum. Its relative strength line remains near all-time highs, and institutional ownership stands at 44%, led by Fidelity Contrafund (FCNTX) and Federated Hermes MDT Large Cap Growth Fund (QILGX). Citigroup’s Asiya Merchant maintains a Buy rating with a $475 target, stressing Dell’s ‘leading share in commercial PCs and servers’ as a durable moat amid AI-driven IT refresh cycles. Crucially, Dell’s AI exposure is diversified: AI PCs (Windows Copilot+), AI-optimized servers (PowerEdge XE9680), and AI storage (PowerScale with GPU-accelerated data lakes). That breadth insulates it from single-point failures—unlike pure-play chip or software vendors.

What Does the Dell AI Forecast Say About Competition?

The Dell AI Forecast isn’t just bullish on Dell—it’s bearish on execution risk elsewhere. Hewlett Packard Enterprise (HPE) moved in sympathy with Dell’s news but trades at a 30% discount to Dell’s forward P/E, reflecting weaker AI server share and slower software monetization. Meanwhile, SanDisk’s recent deal with Meta—a 3.6% stock surge on July 10—underscores how AI storage demand is becoming a standalone growth vector. Dell’s integrated hardware-software stack, however, gives it pricing power HPE and pure-play storage vendors lack. As Daryanani noted, ‘If Dell could procure more supply, there’d likely be upside to expectations’—a direct nod to its advantage in scaling AI infrastructure amid global component shortages.

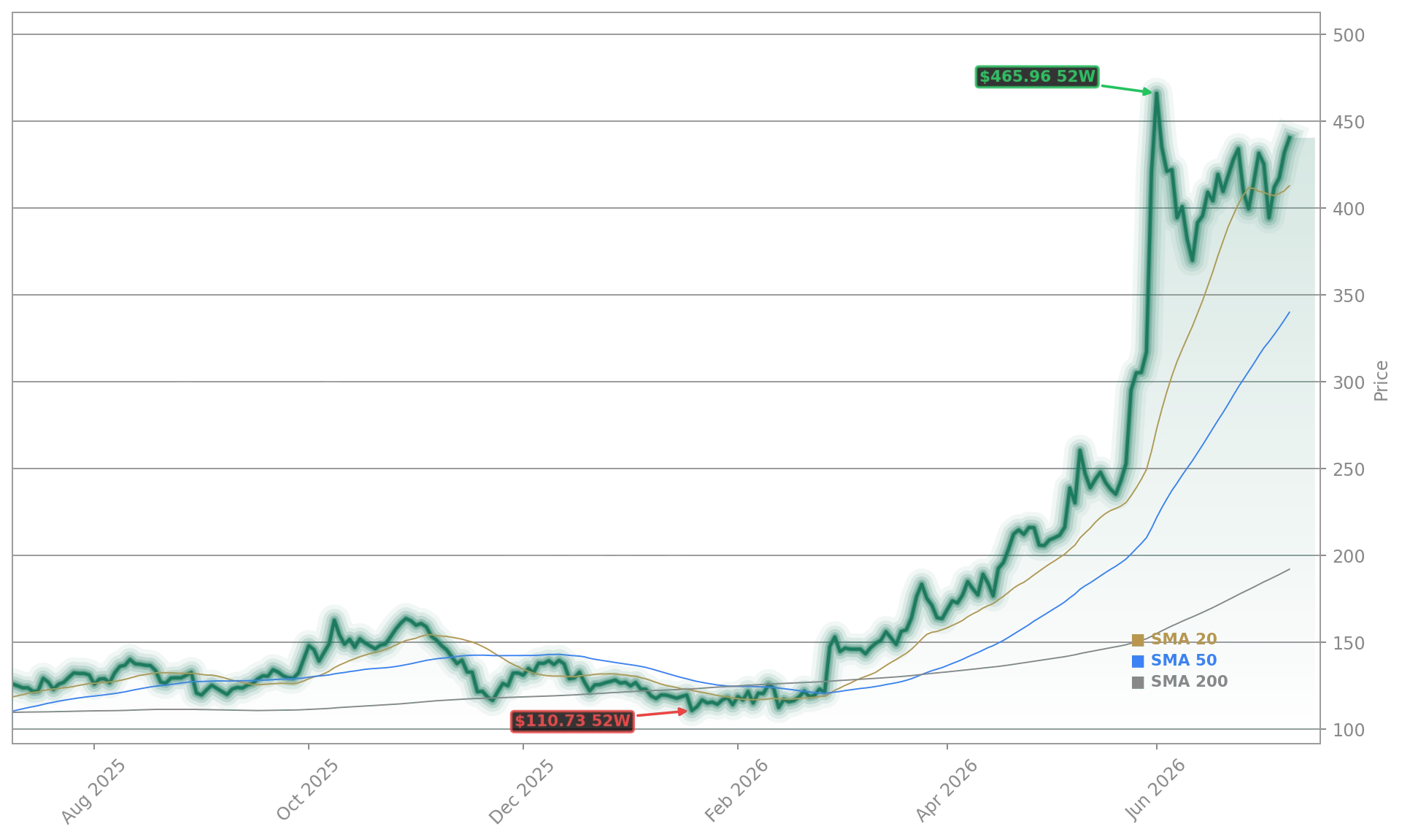

Where Is Dell’s Next Entry Point?

Technically, Dell Technologies Inc. is in the sixth week of a new base, with a potential buy point at $469.47. It cleared a shallow trendline this week and is rebounding off its 21-day exponential moving average—positive short-term signals. With 79% EPS growth projected for 2026 and 21% for 2027, the valuation remains justified. The stock’s Accumulation/Distribution Rating of ‘B’ confirms institutional buying, and its inclusion on the IBD Leaderboard Watchlist signals continued quality momentum. For U.S. portfolios, Dell offers scalable AI exposure without semiconductor cyclicality—and the Dell AI Forecast suggests this is just the beginning.

Our overweight rating on Dell reflects our positive view on the company’s de-leveraging execution and now pivot to a significant capital return story.— Aaron Rakers, Wells Fargo

Related Coverage: Dell’s AI-fueled momentum comes amid rising scrutiny—Dell Ethics Controversy: Stock Jumps 2.6% Amid Scrutiny shows how political and corporate narratives are colliding. Meanwhile, the SanDisk Meta Deal +3.6% as AI Storage Demand Surges highlights how Dell’s integrated storage solutions are competing directly in the same high-growth niche.