Can the bold GameStop Acquisition bid for eBay rewrite GME’s story, or did the board just dodge a massive risk?

Why did eBay reject GameStop’s bid?

In a letter to GameStop Corp. CEO Ryan Cohen, eBay chairman Paul Pressler confirmed that the board, working with independent financial and legal advisers, completed a full review of the unsolicited proposal before deciding to reject it. The offer valued eBay at roughly $55.5–$56 billion, to be paid half in cash and half in GameStop stock, even though GameStop’s own market cap sits at just above $10 billion. Management concluded that the proposed GameStop Acquisition did not reflect eBay’s intrinsic value and carried “significant risks and uncertainties” for shareholders.

The board highlighted several core concerns: lack of clarity around the financing structure, the substantial debt burden required to close the deal, and the operational risks of integrating a brick‑and‑mortar‑leaning gaming retailer with a large global e‑commerce marketplace. Pressler also raised issues with GameStop’s governance and executive incentive structure, signaling discomfort with handing control to a management team that has yet to prove sustainable growth beyond its meme‑stock fame.

eBay CEO Jamie Iannone stressed that the company has already executed a strategic turnaround, sharpening its marketplace focus and competing more effectively against giants like Amazon and Apple. The board reiterated its confidence in eBay’s standalone plan, noting steady improvements in active buyers and consistent capital returns to shareholders through buybacks and dividends.

How was the GameStop offer structured?

Ryan Cohen’s plan envisioned a complex GameStop Acquisition structure. GameStop proposed paying about $9–9.4 billion in cash and using up to $20 billion in financing commitments from TD Securities to purchase roughly 40% of eBay’s shares. The remaining 60% would be rolled into a new combined company, with eBay holders receiving a mix of stock that would leave GameStop effectively in control.

To fund its portion, GameStop would have relied heavily on external debt and the issuance of a large volume of new shares, a move that critics say would have pushed the combined entity into high‑yield or even junk‑rated territory. The share issuance would be strongly dilutive for current GameStop investors, while eBay holders would be swapping relatively stable e‑commerce exposure for a more leveraged, hybrid business heavily influenced by the volatile trading history of GME.

Cohen argued that the GameStop Acquisition could unlock massive cost savings at eBay, targeting about $2 billion in annual reductions: roughly $1.2 billion in sales and marketing, $300 million in product development, and $500 million in general and administrative costs. Based on these cuts, GameStop projected that eBay’s diluted EPS from continuing operations could jump from about $4.26 to $7.79 in the first full year post‑deal. However, the board questioned both the realism of those synergies and the long‑term impact on growth if marketing and product investment are aggressively slashed.

What does the market reaction tell investors?

On Tuesday, GME closed at $22.37, down around 3.45% on the day, before ticking slightly higher to $22.40 in after‑hours trading, while EBAY ended at $110.40, up about 2.10% and easing marginally to $110.22 after the close. Both moves are modest given the headline risk, suggesting that Wall Street had already discounted the likelihood that the GameStop Acquisition proposal would be accepted.

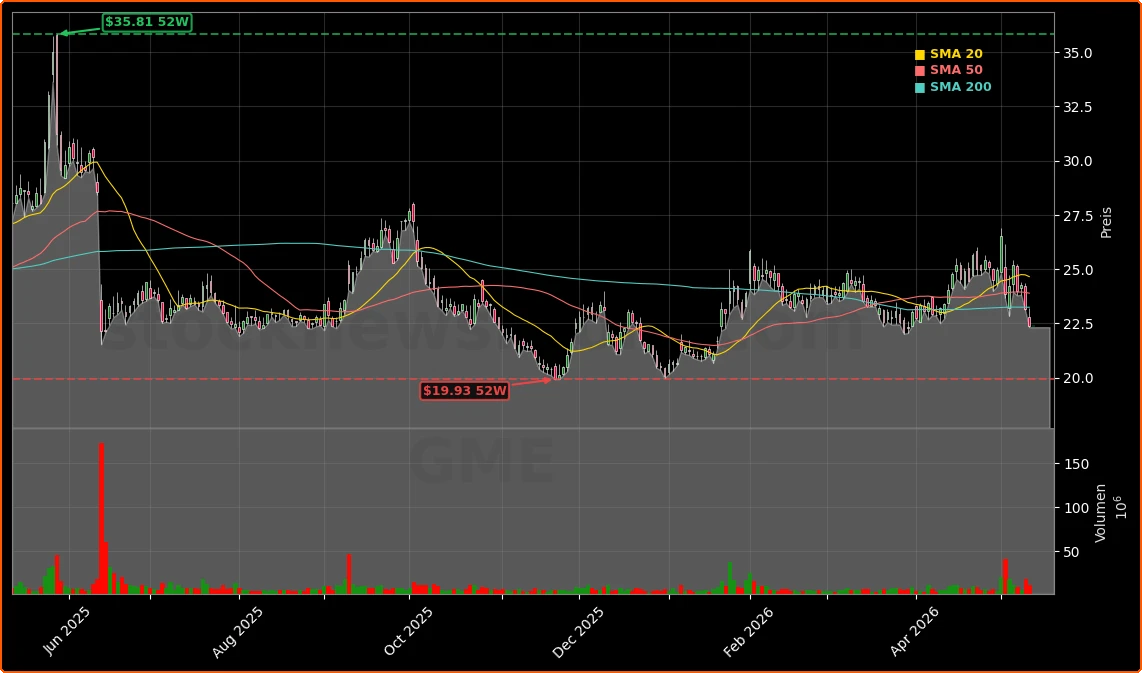

Over the past year, GameStop shares have fallen more than 16–18%, reflecting investor skepticism about the company’s transition away from thousands of physical stores toward a leaner digital and collectibles‑oriented model. The stock remains far above pre‑meme levels but has lost much of the speculative frenzy that once propelled it. By contrast, eBay has gained more than 50% over the last 12 months, outpacing parts of the NASDAQ and S&P 500 as it refocused on higher‑value verticals and improved profitability.

Notably, “Big Short” investor Michael Burry recently exited his entire GameStop stake after the offer was made public, citing concerns that the proposed debt levels contradicted his investment philosophy. The lack of a fully articulated funding plan also weighed on sentiment; in a televised interview, Cohen struggled to clearly explain how all elements of the financing would work, reinforcing the board’s criticism that the bid lacked credibility.

What’s next for GameStop and eBay?

With the GameStop Acquisition bid rejected, several scenarios are now in play. GameStop holds roughly 5% of eBay’s shares, giving Cohen some leverage if he opts for an activist path, including a potential proxy fight over board seats. However, the emphatic rejection and concerns over leverage may make it harder to rally major institutional investors behind a more aggressive campaign.

For GameStop, the failed bid raises fresh questions about strategy. The company has already attracted attention for using part of its balance sheet to buy Bitcoin, later writing covered calls against most of its position to generate yield. Critics argue that chasing a heavily leveraged mega‑deal in e‑commerce only adds to the perception that management is searching for the next narrative rather than executing a coherent long‑term plan.

Analyst coverage remains cautious. While no major Wall Street firm has upgraded GameStop on the back of the announcement, several research desks, including Goldman Sachs and Morgan Stanley, have highlighted the heightened execution and balance‑sheet risk the deal would have created, underscoring why many long‑only funds stayed on the sidelines. For eBay, brokers such as Citigroup and RBC Capital Markets have previously emphasized the company’s improving margin profile and disciplined capital returns, and the firm’s latest defense of its independence is likely to reinforce that thesis.

How does this compare with tech peers?

The clash between GameStop and eBay also underscores how starkly their outlook differs from larger tech and platform peers like NVIDIA and Tesla, which have powered much of the NASDAQ’s recent gains through organic growth and technology leadership rather than high‑risk M&A. While eBay’s growth is slower, its balance sheet and cash generation appear more conventional and predictable than a leveraged GameStop Acquisition structure would have been.

For U.S. investors building diversified portfolios, the episode highlights the importance of balance‑sheet strength, governance quality and strategic clarity, especially in mid‑cap names outside the S&P 500’s megacap leaders. The rejection removes near‑term deal risk for eBay but leaves GameStop under pressure to present a more credible roadmap for value creation.

Related Coverage

For a deeper dive into the initial rationale and financial engineering behind the proposal, readers can explore the detailed analysis in “GameStop Acquisition Shock: Inside the $56B eBay Bid Plan”, which breaks down how the bid was structured and why it immediately divided Wall Street opinion.

We have concluded that your proposal is neither credible nor attractive.— Paul Pressler, Chairman of eBay

In the end, the GameStop Acquisition attempt has been firmly rebuffed, leaving eBay to continue on its standalone path while investors reassess GameStop’s ambitions. For shareholders, the episode reinforces the premium markets place on transparent financing and disciplined strategy over headline‑grabbing deals. The next few quarters will be crucial in showing whether GameStop can pivot from failed mega‑acquisition talk to sustainable execution that earns renewed confidence from Wall Street.