Can Kimberly-Clark Acquisition turn a defensive staple giant into a higher-growth cash machine, or is the market already pricing in the risk?

Why Is Kimberly-Clark Acquisition Timing Critical Now?

With the Kimberly-Clark Acquisition of Kenvue expected to close before December 2026, investors are reassessing KMB’s positioning amid softening oil costs and easing input inflation. Unlike peers such as Procter & Gamble or Colgate-Palmolive, Kimberly-Clark Corporation has already locked in leadership integration — naming former Kenvue CEO Thibaut Mongon as President of Global Consumer Health. That operational readiness signals faster synergy capture. Citigroup recently raised its price target to $122, citing ‘accelerated margin expansion potential post-close’ and reaffirming its ‘Buy’ rating. The deal adds $13 billion in annual revenue, shifting KMB’s health care exposure from 12% to nearly 40% — a structural upgrade that enhances earnings visibility in a slowing consumption environment.

How Does KMB Compare to Tech-Led Indices?

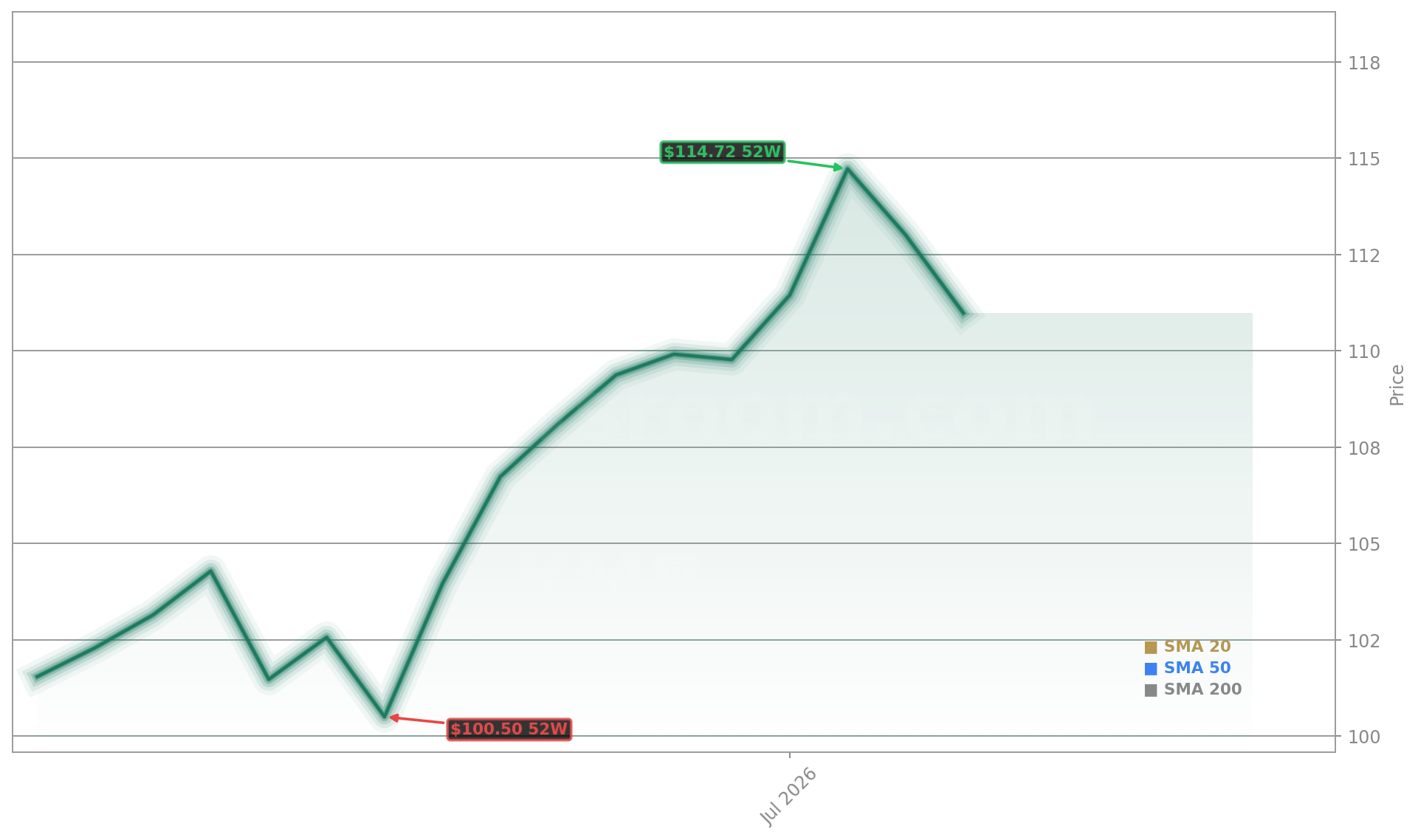

While the S&P 500 and NASDAQ Composite hover near all-time highs — up 9.6% and 11.1% YTD — Kimberly-Clark Corporation outperformed both on a risk-adjusted basis. Its 13.7% YTD gain excludes two $1.28 quarterly dividends, lifting total return to ~18.5%. That contrasts sharply with volatile mega-caps like NVIDIA and Apple, whose valuations remain stretched despite strong earnings. KMB trades at just 15.2x 2026 EPS ($7.54), 30% below its 10-year median P/E of 21.9 — a discount unmatched among Dividend Kings. RBC Capital Markets notes KMB’s ‘valuation gap versus peers is now its widest in a decade,’ making it a tactical hedge against potential tech correction.

What’s the Dividend Safety Outlook Post-Kenvue?

Kimberly-Clark Corporation raised its dividend for the 54th straight year in early 2026 — a hallmark of its Dividend King status. With a current payout ratio of 62% and free cash flow of $2.7 billion (2025), the dividend remains fully covered. The Kimberly-Clark Acquisition adds $1.8 billion in Kenvue’s annual free cash flow, further de-risking the payout. Still, integration execution is key: Morgan Stanley warns that ‘synergy realization must exceed $1.9 billion in Year 2 to maintain current payout coverage under base-case interest rate assumptions.’ That said, CFO Nelson Urdaneta emphasized on the Q1 call: ‘We’ve expanded margins every year since 2023 — and Kenvue’s portfolio gives us pricing power we didn’t have in OTC health.’

Kimberly-Clark Acquisition: Synergies or Stretch?

The $2.1 billion in annual run-rate synergies hinges on supply chain consolidation, shared R&D, and cross-selling — particularly in international markets where Kenvue’s brands are underpenetrated. KMB expects $800 million in cost savings by Q1 2027, with the remainder flowing in 2028. Bloomberg Intelligence estimates $1.4 billion is achievable if procurement and logistics integration proceeds on schedule — a view shared by Goldman Sachs, which upgraded KMB to ‘Conviction Buy’ citing ‘the most credible synergy path among recent CPG-health deals.’ Yet investors should monitor debt: KMB’s net leverage will rise to 3.4x EBITDA post-close — still within investment-grade parameters but higher than its pre-2025 average of 2.6x.

Is KMB a Hedge Against Recession or Inflation?

Yes — and that duality is rare. Kimberly-Clark Corporation’s core brands — Huggies, Kleenex, Cottonelle — show inelastic demand across cycles, while Kenvue’s Tylenol, Neutrogena, and Listerine add counter-cyclical health spending resilience. With consumer confidence softening and oil prices stabilizing near $78/barrel, margin pressure is easing. Unlike hyperscalers such as Tesla or cloud infrastructure players, KMB spends just 3.1% of revenue on capex — freeing capital for dividends and debt reduction. Its 3.6% yield is now the highest among S&P 500 Consumer Staples peers, surpassing Procter & Gamble’s 2.3% and Clorox’s 2.9%.

We’ve expanded margins every year since 2023 — and Kenvue’s portfolio gives us pricing power we didn’t have in OTC health.— Nelson Urdaneta, CFO of Kimberly-Clark Corporation

Kimberly-Clark Corporation remains a cornerstone holding for income and stability-focused portfolios. The Kimberly-Clark Acquisition transforms its growth profile without sacrificing dividend reliability. With regulatory clearance nearly complete and integration leadership in place, the next catalyst is Q3 2026 earnings — where synergy progress and margin guidance will set the tone for 2027. For long-term investors, the combination of yield, valuation, and strategic optionality makes KMB one of the most actionable value plays on Wall Street today.