Are Netflix Earnings signaling a one-off sentiment reset or the start of a tougher era for the streaming giant’s growth story?

How hard did Netflix hit investor sentiment?

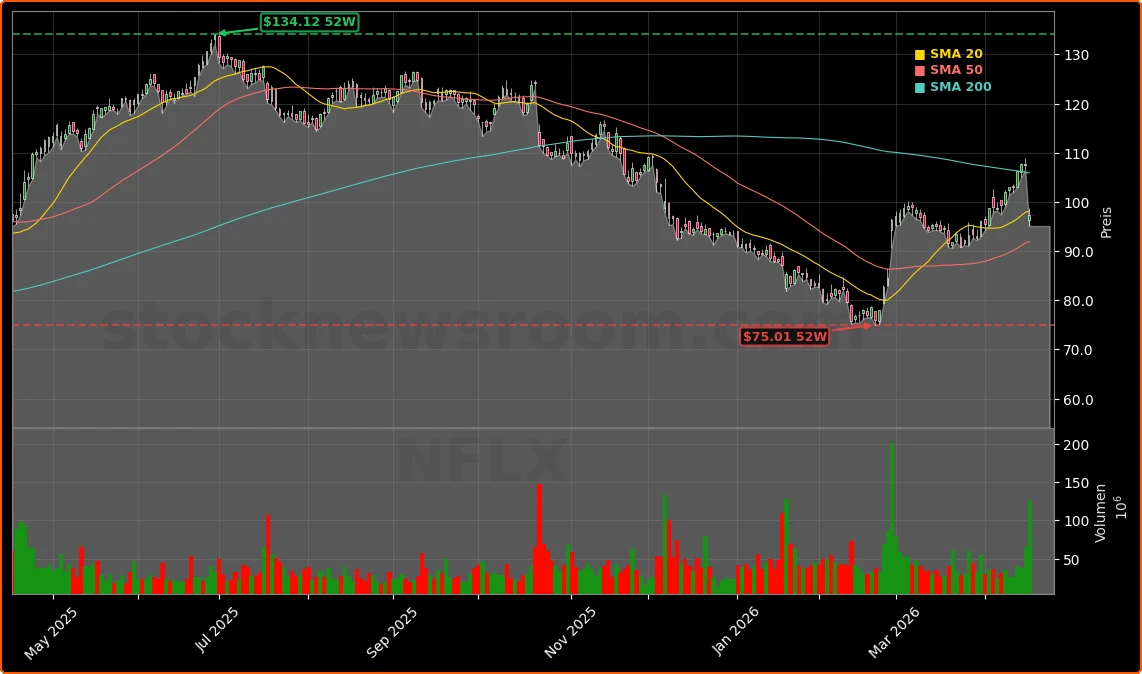

Netflix, Inc. (NFLX) closed Friday at $97.31, down 9.72% on the day and trading roughly flat in after-hours at $97.29. The drop wiped out a double-digit percentage gain the stock had built in the two weeks leading into the report, making Netflix one of the notable losers on a day when the Dow Jones Industrial Average jumped more than 600 points and broader indices rallied. For a stock often treated as a de facto member of the market’s premium growth club alongside Apple and NVIDIA, that divergence is a red flag for momentum-focused investors.

The selloff followed quarterly Netflix Earnings that beat on revenue and profit but came with weaker-than-hoped guidance for the next quarter. Management also disappointed parts of Wall Street by holding back on larger price hikes, eschewing transformative M&A and refraining from a more aggressive share-repurchase plan. With the shares now well below recent highs and far from any 52-week peak, the market is clearly recalibrating expectations around the growth runway.

What exactly went wrong in Netflix Earnings?

The core issue in the latest Netflix Earnings is growth quality, not the backward-looking numbers. Revenue grew at a healthy double-digit clip and operating margins in the low 30s underscored that Netflix has become a cash-generating machine. Yet investors were primed for more. Guidance left limited upside for the rest of the year, suggesting that the era of easy subscriber and pricing gains is fading as the service approaches saturation in key markets.

Recent price increases into the $26–$27 per month range for higher-end plans have triggered noticeable customer churn and migration down to cheaper tiers. At the same time, the ad-supported offering is adding more price-sensitive users, but with significantly lower revenue per user than the traditional premium package. That mix shift is pressuring average revenue per user and diluting the impact of price hikes, undermining one of the main levers bulls had counted on to drive earnings higher.

Analysts at TD Cowen maintained their Buy rating and a $112 price target, arguing the nearly 10% post-report decline is overdone and that strong margins and future optionality in areas like sports and live events still support a constructive long-term view. However, the broader selloff shows many portfolio managers are less patient, particularly with the S&P 500 offering plenty of high-growth alternatives in AI infrastructure and semiconductors.

Is the advertising pivot enough to reignite growth?

Advertising has become the most important new pillar of the Netflix Earnings narrative. The ad-supported tier is doing what it was designed to do: attracting new users who might otherwise sit on the sidelines or share passwords. But from an economic standpoint, those subs are less attractive, at least for now. Their lifetime value lags premium users, and the ad business still needs scale and better targeting capabilities to close the gap.

There is also a strategic trade-off. More ad-supported usage moves Netflix toward the more cyclical, ad-driven media model long dominated by traditional TV, YouTube and social platforms like Meta Platforms. That potentially exposes Netflix, Inc. to the same macro advertising headwinds and competitive dynamics that already challenge online ad players. Investors who once prized Netflix as a relatively pure, subscription-driven play with predictable cash flows are reassessing the risk profile.

Competition for attention is intensifying. YouTube’s dominance in user-generated and short-form video, as well as the rise of free ad-supported TV (FAST) channels, has hurt Netflix’s engagement metrics on the margin. While Netflix still commands huge viewing time, relative engagement trends matter for advertisers and for the company’s ability to push through future price increases without sparking additional churn.

Could user-generated content change Netflix’s story?

One of the most intriguing debates following the latest Netflix Earnings is whether the company should push into user-generated content (UGC) in a more serious way. Internally and among investors, ideas have circulated around a dual-platform approach: a curated, premium Netflix experience on one side and a separate UGC environment—dubbed by some as “You Flicks” or “Uflix”—on the other. The rationale is straightforward: Netflix owns massive global distribution and brand recognition but cedes much of the creator-driven, always-on engagement pie to YouTube and TikTok.

A UGC platform could, in theory, boost engagement, expand the ad inventory and attract a new wave of creators, including emerging makers of AI-generated long-form content. Because creators increasingly distribute across multiple platforms rather than signing exclusive deals, Netflix might not need to spend heavily on rights to seed such a marketplace. However, the Street remains skeptical. There are questions around moderation, brand safety and whether UGC would dilute Netflix’s premium positioning in the eyes of subscribers and advertisers.

Leadership changes add another layer of uncertainty. Co-founder Reed Hastings’ decision to step down from the board has unsettled some investors even though management insists it marks a natural transition rather than a strategic rupture. Former President Donald Trump publicly speculated that Hastings was “forced” out, adding political noise to an already volatile stock reaction. For investors, the critical question is not the rumor mill but whether the next phase of Netflix’s strategy—ads, potential UGC and selective sports rights—can sustain growth without the visionary founder at the table.

How does Netflix stack up against other mega-cap names?

From a portfolio-construction standpoint, the post-earnings slide forces a fresh comparison between Netflix and other high-profile growth stories. While Tesla and NVIDIA remain closely tied to secular themes like EV adoption and AI acceleration, Netflix is increasingly treated as a mature media and entertainment platform. Its valuation, even after the drop, still implies robust long-term expansion, which leaves less margin for error when guidance underwhelms.

Some long-term investors view the current weakness as a buying opportunity, pointing to strong cash flow, deep content libraries and optionality in live events, mobile experiences and merchandising. Others prefer to rotate into software and chip leaders that stand to benefit more directly from generative AI. In this environment, Netflix needs a clear narrative—whether through a more profitable ad stack, disciplined price increases or a well-executed UGC strategy—to reclaim its standing as a core growth holding on the NASDAQ.

Related Coverage: For a deeper dive into how guidance and sentiment are reshaping the bull case, check out Netflix Earnings -9.9% Plunge After Q1 Beat and Weak Guidance, which breaks down why headline beats may mask tougher fundamentals ahead. The same article, also featured as a sector piece at Netflix Earnings -9.9% Plunge After Q1 Beat and Weak Guidance, puts Netflix’s outlook in context with the broader streaming and media landscape.

In the end, the latest Netflix Earnings underscore a company at an inflection point: margins are strong, but premium growth is slowing, ads are rising yet less lucrative, and strategy debates around UGC and sports are just beginning. For investors, Netflix remains a heavyweight in global streaming, but portfolio sizing now depends on how much faith one has in management’s ability to unlock the next growth chapter. The next few quarters of Netflix Earnings will show whether this post-report selloff was a buying chance or an early warning signal for a maturing giant.