Can Oracle’s AI buildout justify a $40 billion financing gamble, or is Wall Street underestimating the balance-sheet risk?

Why Is Oracle Underperforming Amid a Software Rally?

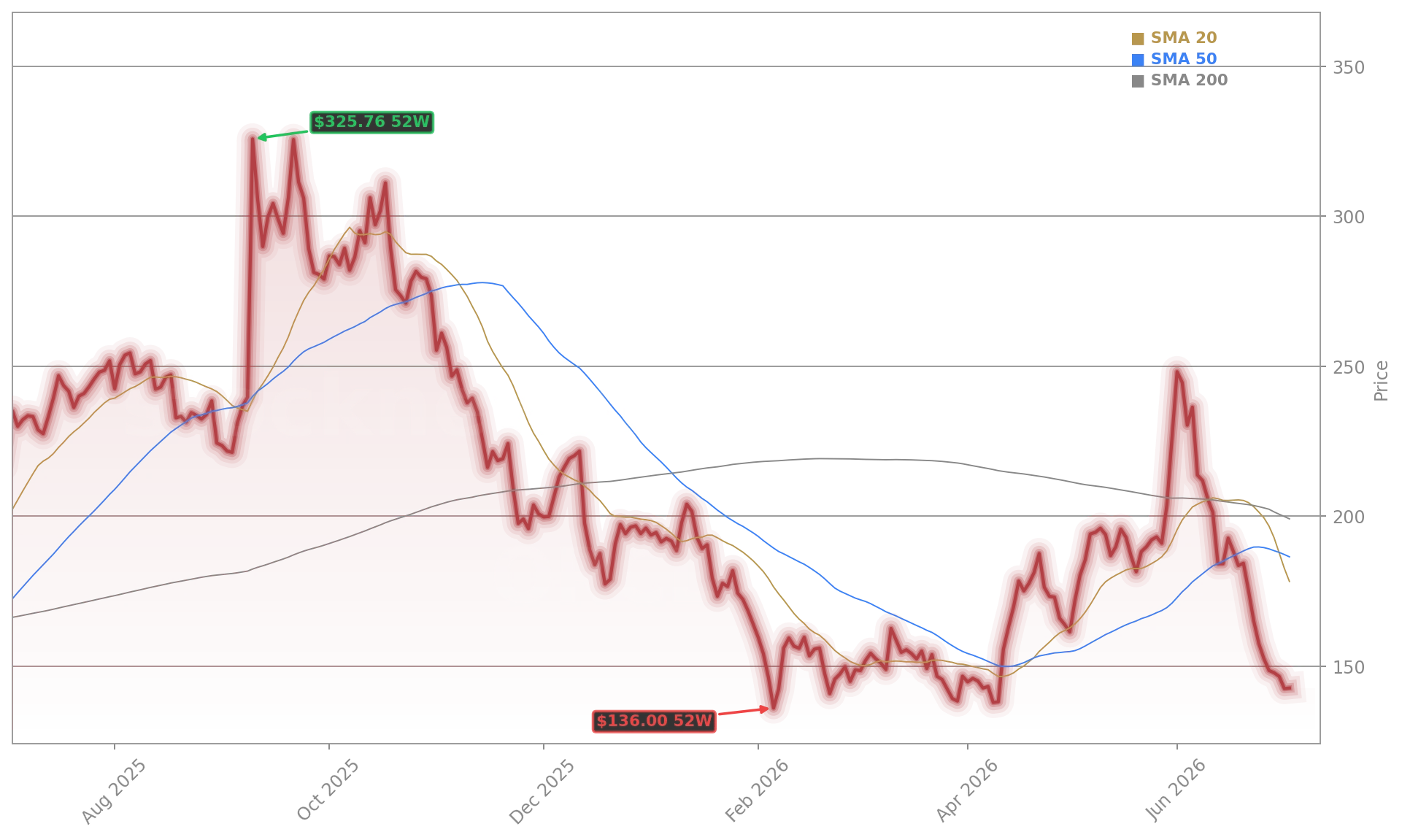

While the iShares Expanded Tech-Software ETF gained over 10% in five days, Oracle Corporation fell on 18 of 22 trading days since early June — a rare divergence that highlights mounting investor anxiety over capital discipline. The stock is now down 28% year to date and 57% from its September 2025 record close of $248.15. This underperformance isn’t due to weak fundamentals: cloud revenue grew 39% in fiscal 2026, and total revenue rose 17%. Instead, it’s driven by Oracle AI Financing concerns — specifically, $56 billion in fiscal 2026 capex, negative $23.7 billion free cash flow, and a $130 billion debt load that’s set to expand further. Competitors like Microsoft and Meta are also spending aggressively, but Oracle’s leverage ratio and lack of a diversified hardware ecosystem make its Oracle AI Financing strategy uniquely exposed to rate-sensitive capital markets.

What Do Analysts Say About Oracle AI Financing?

Despite the turmoil, 84% of Wall Street analysts rate Oracle Corporation a Buy — the highest consensus since May 2011, according to FactSet. Mizuho’s Siti Panigrahi reiterated her $320 price target and called Oracle ‘one of our top picks,’ citing its end-to-end AI stack across database, infrastructure, and applications. But she explicitly flagged ‘financing challenges’ as a key risk — the first major analyst to name Oracle AI Financing as a material headwind. KeyBanc Capital Markets maintained its Overweight rating and $300 target, noting ‘increasing comfort’ that operating expenses will remain muted — a critical offset to capex pressure. Meanwhile, Citigroup recently raised its price target to $265, emphasizing ‘backlog durability’ and ‘cloud margin expansion’ as de-risking levers for Oracle AI Financing.

How Does Oracle Compare to Hyperscaler Peers?

Oracle is now grouped with the ‘Big Five’ hyperscalers — alongside Meta, Microsoft, Alphabet, and Amazon — whose combined AI infrastructure spend is approaching 2.5% of U.S. GDP. Benzinga reports Q1 2026 data center lease commitments topped $850 billion, up 204% year-over-year, with Oracle, Meta, and Microsoft leading the surge. Yet unlike its peers, Oracle lacks a consumer revenue stream or advertising moat. Its AI buildout is purely enterprise- and government-facing — evidenced by its newly announced third Oracle Defense Ecosystem cohort, featuring cybersecurity and mission-critical AI partners. That focus demands massive upfront investment with longer payback horizons, intensifying the Oracle AI Financing debate. Wisconsin’s projected 40% energy demand surge by 2032 — driven largely by Oracle, Microsoft, and Meta data centers — further underscores the scale of physical infrastructure required.

Is the Sell-Off Overdone?

Historically, Oracle’s sharp pullbacks have been followed by strong recoveries. After each of the prior seven instances where Oracle fell 30%+ in a month — dating back to 1986 — the stock posted a median gain of 16% within three months and 93% a year later. That pattern is resonating today: premarket trading on Monday, July 6, showed Oracle up 2.37% to $143.59 — snapping its nine-day losing streak, its longest since December 2021. The rebound coincided with improved Nasdaq futures (+1.20%) and S&P 500 futures (+0.47%). Simply Wall Street estimates Oracle is undervalued by 34%, citing rising dividends and cloud guidance, while TIKR’s model implies 244% upside to $483 — contingent on successful Oracle AI Financing execution and earnings growth. Still, Jay Woods of RBC Capital Markets remains cautious, preferring Microsoft and Snowflake over Oracle amid financing uncertainty.

Related Coverage: For deeper analysis on the $40 billion financing question, see Oracle AI Financing: Why $40B Is Testing ORCL Bulls. Investors also should review Oracle (ORCL) Stock May Be Undervalued Despite AI Restructuring Cuts and Oracle (ORCL) Announces Third Cohort of Oracle Defense Ecosystem.

Oracle’s end to end AI stack across database, infrastructure, and applications positions it as a key long-term beneficiary of AI adoption.— Siti Panigrahi, Mizuho

Oracle Corporation remains a pivotal AI infrastructure play — not because it’s the largest, but because its financing path could define Wall Street’s tolerance for capital intensity in the AI era. With $638 billion in AI-driven backlog and 84% analyst support, the market isn’t doubting Oracle’s opportunity — it’s testing its Oracle AI Financing discipline. For long-term investors, the current price action may represent a rare entry point ahead of next fiscal year’s capex inflection — assuming debt markets remain cooperative and execution stays on track.