Can Oracle’s massive AI funding push unlock the next growth phase, or is Wall Street staring at a debt-fueled warning sign?

Why Is Oracle Underperforming Amid a Software Rally?

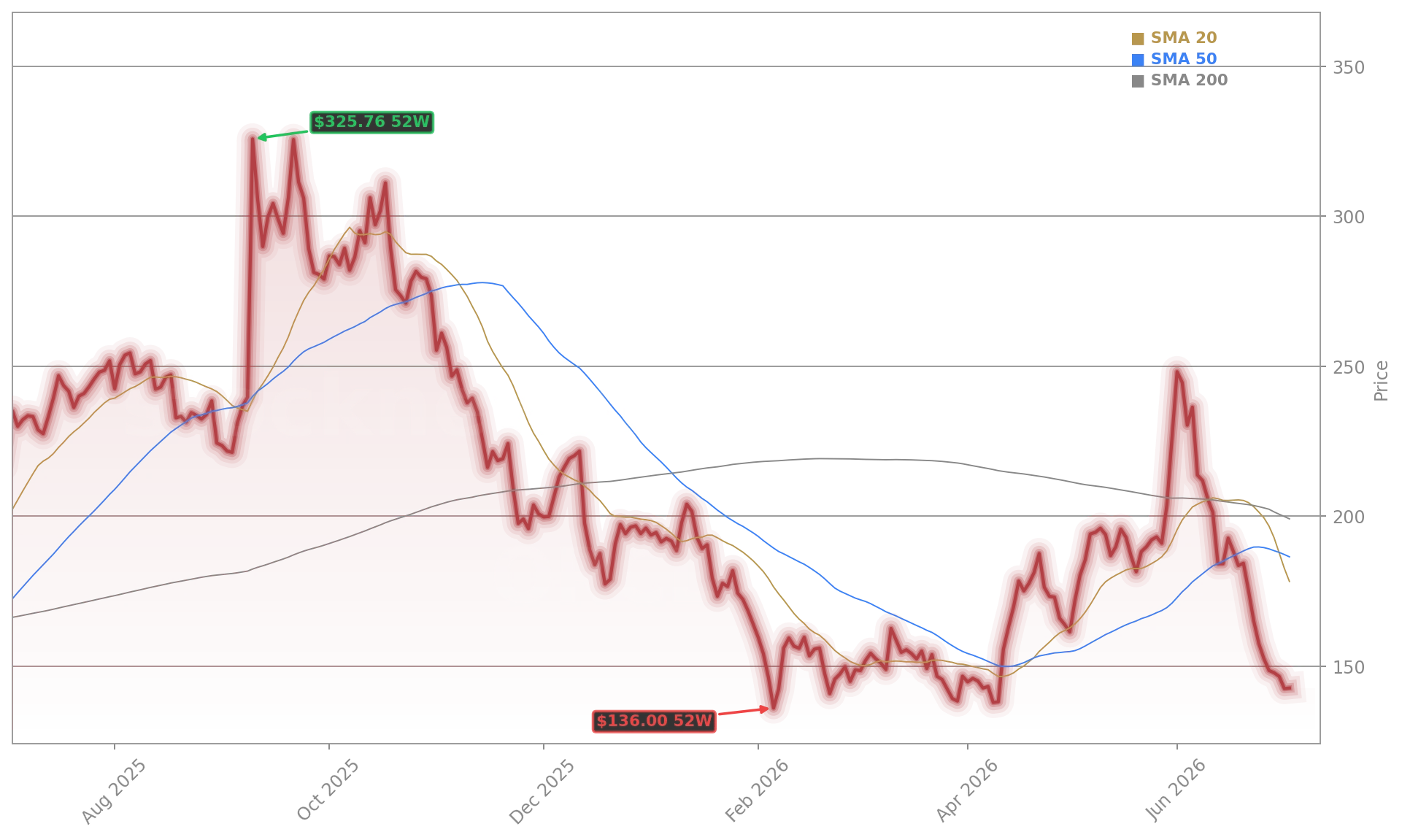

While the iShares Expanded Tech-Software ETF surged over 10% in five days, Oracle Corporation plunged — falling on 18 of 22 trading days since its June 1 high of $248.15. The stock now trades at $142.81, down 57% from its September 2025 all-time close. That divergence is stark: the broader NASDAQ rose 5.2% in June, while Oracle dropped 35%, its worst monthly performance since 1990. Investors aren’t rejecting AI — they’re questioning execution. Unlike NVIDIA, whose AI revenue growth is already monetized, Oracle’s AI infrastructure spend remains pre-revenue. Its $16.49 billion quarterly capex — the largest in its history — pushed full-year free cash flow to negative $23.7 billion, raising red flags for U.S. portfolio managers focused on cash discipline.

What Does Oracle AI Financing Actually Cover?

Oracle AI Financing isn’t just about debt rollovers — it’s a structural pivot. The company plans to raise up to $40 billion in new financing to support a projected $92 billion in fiscal 2027 capital expenditures. That sum dwarfs even Meta’s AI spend and places Oracle among the top five hyperscalers alongside Microsoft, Alphabet, and Amazon. According to Mizuho analyst Siti Panigrahi, Oracle’s ‘end-to-end AI stack’ — spanning database, cloud infrastructure, and enterprise applications — is a legitimate long-term moat. But she explicitly cited ‘financing challenges’ as a key risk, underscoring that Oracle AI Financing must balance speed with sustainability. KeyBanc Capital Markets, maintaining an Overweight rating and $300 price target, emphasized muted operating expense growth as the ‘upside catalyst’ — suggesting investors are betting Oracle can scale AI without exploding its cost base.

How Do Analysts Reconcile Debt With 84% Buy Ratings?

With 84% of analysts assigning Buy ratings — the highest level in 20 years — Oracle’s valuation disconnect is extreme. The average price target of $254.84 implies 82% upside from Thursday’s close, led by Mizuho’s $320 target and Citigroup’s $275 forecast. RBC Capital Markets reiterated its ‘Outperform’ rating, citing ‘unmatched database-AI integration’ and strong RPO visibility — $638 billion in remaining performance obligations provides multi-year revenue clarity. Yet Jay Woods, a noted software strategist, remains bearish, warning Oracle ‘cannot lift its head and maintain momentum’ and preferring Microsoft and Snowflake. That split reflects Wall Street’s broader tension: is Oracle’s debt-funded AI bet visionary or vulnerable? Unlike Tesla, which monetizes hardware and software synergies, Oracle’s path relies on enterprise adoption timelines that may lag infrastructure buildout.

Is This the Right Moment for U.S. Investors to Buy the Dip?

Historical precedent offers cautious optimism. Oracle has suffered eight monthly declines of 30%+ since 1986. After the prior seven, the stock delivered a median 16% gain within three months and 93% over 12 months — outperforming the S&P 500 two-thirds of the time. With NASDAQ futures up 1.2% and S&P 500 futures rising 0.47% Monday, broader sentiment is turning. Oracle’s premarket jump of 2.37% signals renewed interest — but only if Oracle AI Financing is perceived as credible, not desperate. For U.S. investors holding large-cap tech positions, Oracle represents a high-conviction, high-risk AI lever — one that demands scrutiny of debt service costs, capex ROI timelines, and competitive positioning against cloud-native rivals.

Oracle’s end to end AI stack across database, infrastructure, and applications positions it as a key long-term beneficiary of AI adoption.— Siti Panigrahi, Mizuho

Related Coverage: Is Oracle AI Infrastructure becoming Wall Street’s next cloud winner, or is the market right to fear the cost of its massive buildout? Oracle AI Infrastructure -2.3% as $95B CapEx Sparks Debate. Has Wall Street misread Adobe’s AI risk so badly that this Adobe Upgrade could mark the start of a major rerating? Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears.