Is Oracle AI Infrastructure becoming Wall Street’s next cloud winner, or is the market right to fear the cost of its massive buildout?

Why Are Analysts Raising Targets on Oracle?

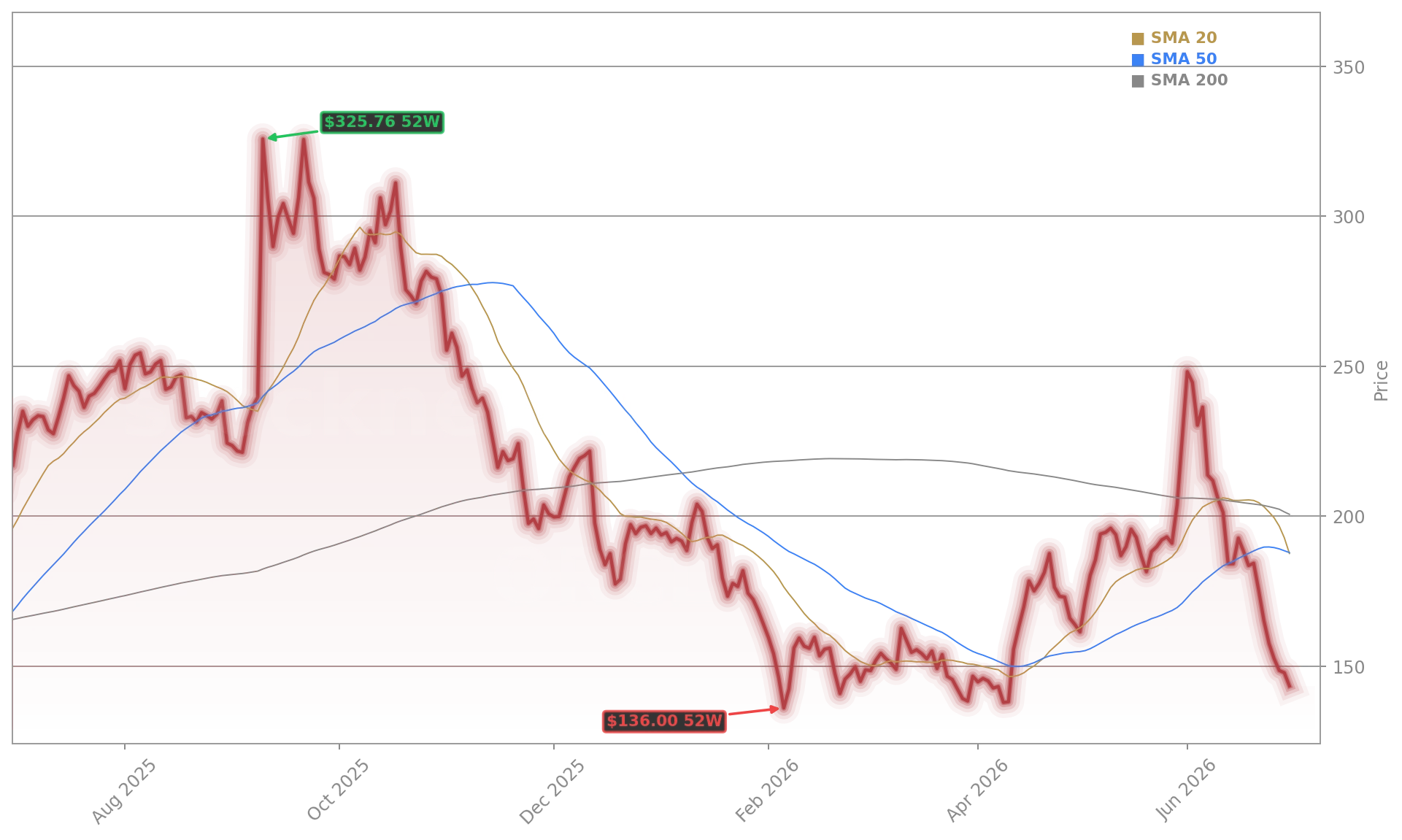

KeyBanc Capital Markets reaffirmed its Overweight rating and lifted its price target to $300, citing improved transparency around Oracle’s AI infrastructure spend and upward revisions to fiscal 2028–2030 EPS estimates—now exceeding consensus for 2029 and 2030. Mizuho Securities followed with an Outperform rating and a $320 price target, highlighting the on-time launch of the Abilene supercluster and additional OCI capacity. Both firms underscore that Oracle AI Infrastructure is delivering tangible, scalable revenue—not just promises. The 93% YoY Infrastructure as a Service growth, per Oracle’s latest results, is now the fastest among major U.S. cloud providers outside of NVIDIA-driven hardware suppliers—and significantly outpaces Microsoft’s Azure infrastructure growth rate in Q2 2026, according to Seeking Alpha.

How Does Oracle AI Infrastructure Compare to Rivals?

Unlike Amazon Web Services or Microsoft Azure, Oracle’s infrastructure strategy is tightly integrated with its enterprise software stack—giving it unique leverage in regulated verticals like finance and government. While Apple and Tesla remain hardware- and mobility-focused, Oracle is building the compute, power, and data layer that underpins their AI ambitions. Bloomberg notes Oracle’s fuel cell partnership with Bloom Energy—now scaled to 2.8 GW—has cut AI data center deployment timelines by more than 40%, directly addressing the single largest bottleneck cited by hyperscalers. That edge places Oracle AI Infrastructure in a distinct tier alongside Meta’s and Microsoft’s in-house builds—but with higher gross margin potential due to proprietary software lock-in and vertical-specific compliance.

What’s the Real Cost of Oracle AI Infrastructure?

Oracle’s $95 billion gross CapEx implies roughly $70 billion in cash outlays for fiscal 2027—up sharply from $50 billion in Q3—but still below the $100 billion Street expectations Oracle dismissed in Q2. The company confirmed $20 billion in incremental financing needs, manageable given its $53 billion in cash and equivalents. Still, the near-term pressure is real: free cash flow turned negative in Q4 2026, and the stock has fallen 23.33% year-to-date. Yet William Blair added Oracle to its Conviction List—citing ‘strong position in AI infrastructure and cloud demand’—while removing Meta Platforms, signaling a strategic rotation toward infrastructure enablers over end-user AI platforms.

Is the Market Mispricing Oracle’s AI Infrastructure Bet?

Despite the sell-off, Oracle’s AI infrastructure execution is gaining traction beyond Wall Street. A new ISG report names Oracle the top overall leader in enterprise talent recruitment and performance management suites—driven by demand for AI-integrated, governed HR platforms. Its newly launched Oracle Manager Edge, an AI coaching assistant embedded in Slack and Microsoft Teams, reinforces that enterprise AI adoption is moving from infrastructure to workflow—where Oracle’s cloud applications dominate. Meanwhile, a lawsuit against Wisconsin’s PSC over $100 million in data center financial security requirements underscores the scale of Oracle’s physical buildout. That litigation isn’t a risk—it’s evidence: Oracle AI Infrastructure is now large enough to challenge state-level regulatory frameworks.

Related Coverage: Oracle’s aggressive AI infrastructure expansion has coincided with a 5.3% workforce reduction, sparking debate over whether the pivot is a disciplined reallocation or a sign of overextension. Meanwhile, the broader quantum-AI infrastructure race continues to accelerate, as seen in IonQ’s new global partnership with Archer, which expands sovereign quantum access just as Oracle scales its classical AI infrastructure footprint.

Larry’s been seeing around corners for 49 years. He’s positioned his business ahead of every single way.— Analyst, William Blair

Oracle Corporation remains a pivotal infrastructure play in the AI era—not as a chipmaker like NVIDIA, nor as a consumer-facing platform like Meta, but as the enterprise-grade engine powering regulated, high-performance AI workloads. The next quarterly earnings will test whether OCI revenue growth sustains above 85%—a threshold that would validate Wall Street’s $300–$320 price targets. For investors seeking exposure to the trillion-dollar AI infrastructure buildout, Oracle AI Infrastructure is no longer speculative—it’s essential.