Can Meta turn massive AI spending into real returns before investor patience runs out?

Is Meta’s AI Spend Justifying Its Stock Price?

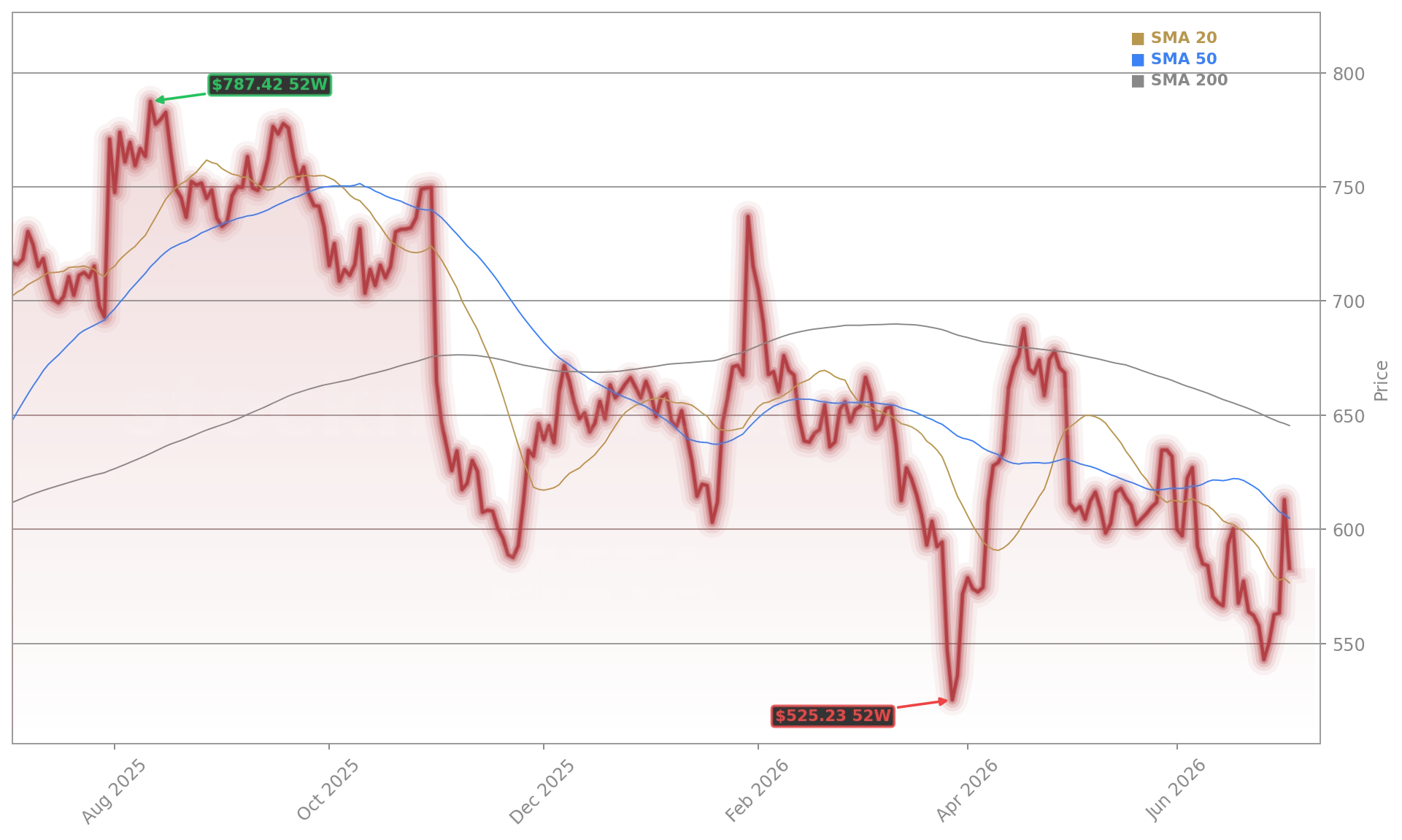

Meta Platforms, Inc. is down nearly 10% year-to-date despite $56.3 billion in revenue — up 33% year over year — and record AI investment. The company now expects to spend $125–$145 billion on chips, data centers, and infrastructure in 2026, up from prior guidance. Yet CEO Mark Zuckerberg conceded in an internal town hall that AI agent development hasn’t ‘accelerated in the way we expected’ and that the 2026 reorganization ‘wasn’t as clean as it could have been.’ That candid admission — paired with a 4.65% intraday slide — signals growing Wall Street unease. While Wells Fargo raised its price target to $767, the market is pricing in execution risk: implied volatility is falling, momentum is weakening, and META’s weight in the S&P 500 is amplifying broad index volatility. For investors holding the Meta AI Strategy as a core tech exposure, the question isn’t whether AI matters — it’s whether Meta can translate capital into cash flow before rivals like NVIDIA and Apple widen their moats.

What Does ‘Opt-In Only’ Mouse Tracking Say About Trust?

Meta’s CTO Andrew Bosworth confirmed in an internal town hall that the controversial mouse-and-keystroke AI training program — paused after an internal leak exposed employee data — will return only as an opt-in feature. That reversal follows another retreat: engineers reassigned to Meta’s Applied AI task force were recently granted the option to leave — a move dubbed ‘the undraft’ by staff. With morale reportedly ‘one of the worst it’s ever been’ and 8,000 layoffs in May, the trust deficit is material. This matters for investors because AI development at scale requires cultural alignment — not just compute. When top AI researchers at Meta Superintelligence Labs cite ‘elbow grease’ as the path to ‘superintelligence,’ it underscores the human friction beneath the technical ambition. For U.S. portfolios, this isn’t just HR noise: it’s a leading indicator of whether Meta’s Meta AI Strategy can sustain velocity amid rising regulatory scrutiny — from the UK’s Online Harms Bill to U.S. FTC investigations into pixel tracking.

Can Meta Compute Compete With AWS and Azure?

Meta is developing ‘Meta Compute,’ a cloud infrastructure business to sell excess AI compute and models — directly challenging CoreWeave and Nebius, and indirectly pressuring Tesla-adjacent AI infrastructure plays. But analysts are skeptical. Saxo Bank warns the move may signal early overcapacity in AI infrastructure, while UBS’s Nadia Lovell notes hyperscalers’ CapEx is up 70% year-over-year — yet monetization lags. Crucially, Meta lacks enterprise relationships, security certifications, and a full-stack cloud offering. As Bloomberg notes, AWS has spent 18 years building what Meta wants to copy — and even in an optimistic scenario, Meta Compute will compete primarily with specialists, not incumbents. That reality hit shares hard: META fell alongside semiconductor peers like Broadcom and AMD, dragging down the Nasdaq — which dropped 0.8% — while the Dow hit a new all-time high. The sell-off confirms Wall Street’s concern: without a cloud revenue stream, Meta remains a single-digit-multiple ad business betting on AI’s future — not its present.

Is ‘Watermelon’ Enough To Close the Gap With OpenAI?

Meta’s AI chief Alexandr Wang claimed internally that its next model, codenamed ‘Watermelon,’ has matched OpenAI’s GPT-5.5 on key benchmarks — a notable leap from Muse Spark (Avocado), its April release. If verified, it would validate Meta’s $100B+ AI bet. But OpenAI launched GPT-5.6 last month, and Google’s Gemini 3.5 remains entrenched in enterprise workflows. Meanwhile, Meta’s open-source philosophy — while lauded by developers — hasn’t yet translated into developer adoption at scale. Unlike NVIDIA’s CUDA ecosystem or Apple’s App Store, Meta lacks a distribution moat. The market’s reaction — punishing META while rewarding Amazon (+0.55%) on the same cloud news — reveals investor preference for proven monetization over speculative benchmarks. For S&P 500 investors, Meta’s Meta AI Strategy remains a high-risk, long-duration bet — one that could reshape the index’s tech weighting if it succeeds, or accelerate rotation into value if it stalls.

Related coverage: Meta Cloud +10.9%: Meta Soars as AI Push Expands examines how the company’s infrastructure pivot could unlock $20 billion in annual compute revenue — if demand materializes. Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears shows how Wall Street is reassessing AI disruption — upgrading Adobe on evidence that creative AI tools are boosting, not replacing, subscription revenue. Both pieces underscore a broader truth: AI winners will be those monetizing intelligence, not just building it.

AI spend puts strain on company and stock price ‘would be higher’ without it, but it is a long-term investment.— Mark Zuckerberg, CEO, Meta Platforms, Inc.

Meta Platforms, Inc. remains a pivotal force in the Nasdaq and S&P 500 — but its Meta AI Strategy is now under intense, earnings-driven scrutiny. For investors, the next 3–6 months — when Zuckerberg expects ‘more benefits’ — will determine whether the stock rebounds as a tech leader or drifts as a cautionary tale. The path forward demands disciplined capital allocation, transparent execution, and tangible monetization — not just model benchmarks.