Can a double beat on Philip Morris earnings offset a trimmed outlook and growing regulatory risks in smoke-free products?

How did Philip Morris Earnings surprise Wall Street?

Philip Morris International Inc. (PM) reported first-quarter 2026 results that were stronger than analysts had anticipated on both the top and bottom line. Net revenue climbed 9.1% year over year to $10.15 billion, clearly ahead of market expectations. Adjusted earnings per share came in at $1.96, beating the consensus estimate of around $1.83.

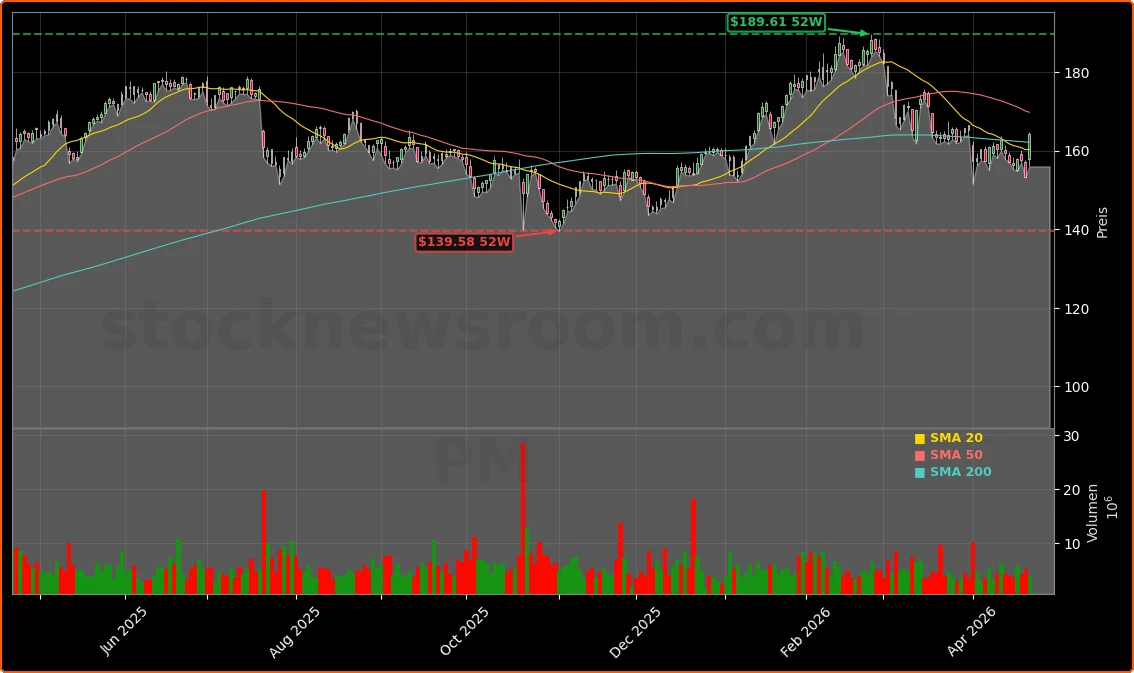

The market reaction was immediate. On the New York Stock Exchange, PM shares recently traded at $164.17, up about 7.1% versus the prior close of $154.77, outpacing the broader S&P 500 on the day. While the stock is below its 52‑week high in Europe of about EUR 161, the move underscores renewed confidence in the smoke-free pivot despite a more cautious guidance tone.

However, on a reported GAAP basis, earnings per share actually declined. EPS fell from $1.72 a year ago to $1.56, a drop of roughly 9.3%. Management attributed this to a non-cash revaluation of a minority stake in India, which weighed on reported profit but did not change the underlying operating trajectory. For investors focused on Philip Morris Earnings quality, the gap between adjusted and reported EPS is an important nuance.

Is the smoke-free pivot delivering?

The latest Philip Morris Earnings reaffirm that the transformation away from traditional cigarettes is gaining traction. The company’s international smoke-free business — encompassing IQOS heated tobacco, e-vapor under the Veve brand, and oral nicotine products — increased net revenue by nearly 25%, with organic growth of around 16%.

IQOS remains the primary engine. In Japan, IQOS has reached an estimated market share of almost 35% of the total nicotine market, delivering another record quarter. Taiwan is emerging as one of the company’s strongest IQOS launches to date, underlining the global runway for heated-tobacco adoption. Across key markets, Philip Morris holds roughly 75% market share in heated-tobacco devices, outpacing rivals like British American Tobacco, Imperial Brands and Japan Tobacco.

Smoke-free products now account for about 40% of group revenue and carry higher margins than legacy combustible cigarettes. For long-term investors in the consumer staples and dividend space, this mix shift is central to the investment case. Management has signaled that a spin-off of the smoke-free unit is under consideration toward the end of the year, an option that, if executed, could create a more growth-focused vehicle distinct from the mature cigarette franchise. That possibility is increasingly relevant for portfolio managers benchmarking against the S&P 500 and global defensive sectors.

Why was the full-year outlook cut?

Despite the strong Philip Morris Earnings in Q1, the company trimmed its full-year 2026 reported EPS guidance. Management now expects $7.56 to $7.71 per share, down from a prior range of $7.87 to $8.02. The downgrade is driven by two main factors: intensifying competition in the traditional tobacco segment and regulatory uncertainty around nicotine pouch brand ZYN in the United States.

In the U.S., ZYN faces what the company describes as an uneven competitive landscape. New variants — including ZYN Ultra — are still awaiting Food and Drug Administration clearance, while the FDA has been more cautious on approving stronger flavors that are central to the category’s growth. As a result, the U.S. segment saw a striking 31% revenue decline in the quarter, in stark contrast to the strength of international operations.

Looking ahead to the second quarter, management guides for adjusted EPS of $2.02 to $2.07. The company expects disruptions from the Middle East conflict to remain manageable, with the main impact felt in duty-free channels due to weaker travel. Higher freight and energy costs have already been factored into forecasts, limiting the risk of additional cost shocks if current conditions persist.

How do Philip Morris Earnings compare with peers?

On Wall Street, the latest Philip Morris Earnings will be assessed relative to global tobacco peers trading both in the U.S. and abroad. While competitors such as British American Tobacco and Japan Tobacco are also investing heavily in reduced-risk products, none has matched Philip Morris’s scale in heated tobacco. This leadership position and the potential spin-off narrative differentiate PM within the sector, particularly for U.S. investors seeking yield with structural growth.

At the same time, the U.S. regulatory overhang around ZYN narrows the gap versus rivals in oral nicotine. Any further tightening by the FDA could compress growth expectations and weigh on valuation multiples. Conversely, incremental approvals for ZYN Ultra or broader flavor portfolios would be a clear positive surprise.

Against the wider equity market, PM’s post-earnings jump stands out at a time when many defensive names lag high-growth tech giants like NVIDIA, Apple and Tesla. For diversified portfolios, PM offers a different risk-return profile: high cash flow, a sizable dividend, and exposure to a multi-year product transition rather than pure-play AI or EV momentum.

Analyst commentary around the sector remains mixed. Large banks such as Goldman Sachs, Citigroup and Morgan Stanley have previously highlighted regulatory risk but also pointed to attractive cash returns and improving growth in smoke-free categories. The evolution of their ratings and price targets after these Philip Morris Earnings will give investors another signal on how far the guidance cut has dented confidence.

In summary, the latest Philip Morris Earnings underscore a company that is executing well on its international smoke-free strategy while wrestling with U.S. regulatory friction and a softer outlook for legacy products. For investors, PM remains a high-yield defensive play with an embedded growth option in IQOS and nicotine pouches. The next quarters will show whether management can navigate FDA hurdles, unlock potential value from a smoke-free spin-off, and turn today’s transformation into durable shareholder returns.