Can Fox turn a $22 billion Roku Acquisition into a streaming breakthrough, or is Wall Street right to fear the price tag?

What Does the Roku Acquisition Mean for Wall Street?

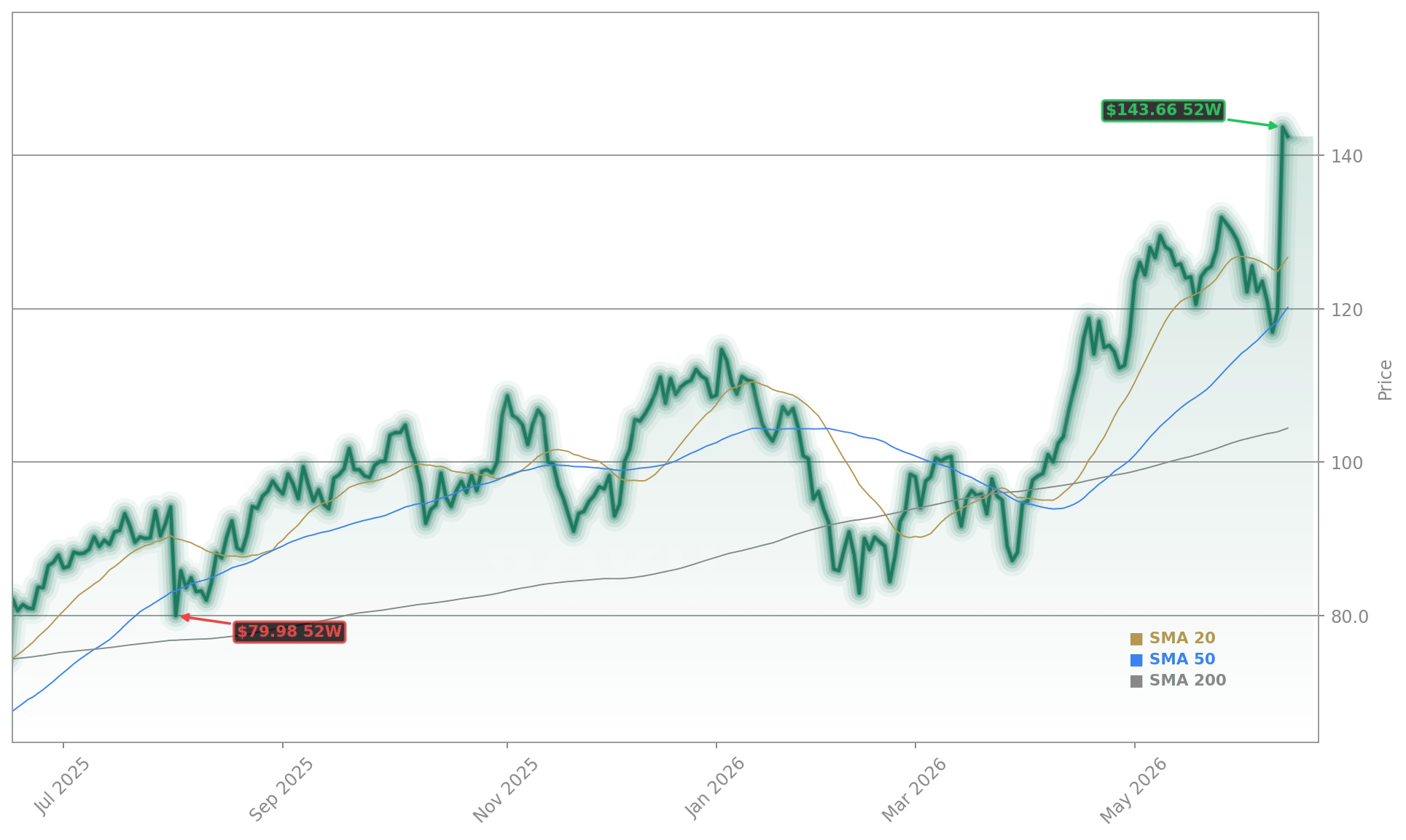

The Roku Acquisition delivers immediate strategic scale — and immediate portfolio volatility. Roku, Inc. shares rose to $144.16 in after-hours trade — a 1.19% gain — after closing at $142.46, while Fox Corporation (FOXA) plunged to $68.30 (+24.75% after-hours) from a $54.75 intraday low, reflecting investor skepticism about debt-financed transformation. The $22 billion price tag — $96 in cash plus 0.9693 shares of FOX Class A stock per ROKU share — represents an 11.4% premium to Roku’s prior close but leaves 27% of the combined entity in Roku shareholders’ hands. That structure explains the muted rally: investors are pricing in execution risk, regulatory scrutiny, and the $12 billion bridge loan arranged with Morgan Stanley Senior Funding, Inc. The combined company will hold ~2.8x net leverage post-close — manageable, but a sharp departure from Fox’s historically conservative balance sheet.

How Does Roku Stack Up Against Netflix and Disney?

Unlike Netflix — which missed its chance to build its own hardware platform when Roku founder Anthony Wood worked in its offices in the early 2000s — Roku owns the operating system layer across 100 million+ global households. That reach dwarfs Disney’s 130 million combined Disney+/Hulu subscribers and exceeds Netflix’s 270 million global accounts in terms of active TV screen engagement. Roku’s platform segment — advertising and subscriptions — generated $1.13 billion in Q1 2026, up 28% year-over-year, while device revenue declined 16%. That mirrors the trajectory of Apple and Tesla hardware-as-acquisition-channel models. Meanwhile, Netflix recently abandoned its $25 billion Warner Bros. Discovery bid, pivoting to a $15 billion buyback — a stark contrast to Fox’s aggressive, platform-first acquisition. Disney’s streaming growth has stalled, and its D23 conference this summer offers no Roku-scale distribution leverage.

Roku Acquisition: What’s Next for Fox’s Growth Profile?

The Roku Acquisition transforms Fox from a linear-first media holding into a vertically integrated streaming power. JPMorgan analysts underscored this shift, calling it a ‘pivot toward free ad-supported streaming’ that answers ‘long-term concerns about a legacy in PayTV.’ With Tubi nearing 100 million monthly active users and The Roku Channel adding another 60+ million, Fox gains direct access to first-party CTV data — a critical advantage over traditional ad buyers like Comcast or Charter. Revenue synergy targets include $400 million in annualized cost synergies and accelerated monetization of FOX News, NFL, and MLB inventory across Roku’s ad stack. Crucially, Fox CEO Lachlan Murdoch emphasized financial discipline: the deal maintains Fox’s investment-grade rating and uninterrupted shareholder return program — buybacks and dividends continue.

Will Regulators Approve the Roku Acquisition?

This is a defining moment for FOX, and a natural extension of the deliberate and focused strategy we have been executing for nearly a decade.— Lachlan K. Murdoch, Executive Chair and CEO of Fox Corporation

Regulatory risk is the biggest near-term overhang. While Fox and Roku pledged to keep the platform ‘open and partner-friendly’ — ensuring continued distribution of NVIDIA-powered streaming apps, Apple TV, and Netflix — antitrust scrutiny is inevitable. The U.S. Department of Justice and FTC will examine whether Fox’s ownership compromises neutrality in app placement, ad bidding, or data sharing. Roku’s 25% U.S. CTV OS market share (ahead of Samsung’s Tizen at 23%) gives it gatekeeper status — a role that could trigger behavioral remedies. Baird analysts downgraded Roku to Neutral with a $160 price target, citing ‘valuation and deal uncertainty,’ while Needham lifted its target to $170 and Citizens raised theirs to $175 — both affirming the strategic logic behind the Roku Acquisition. The transaction requires approvals from both companies’ shareholders and multiple international regulators, with closing expected in the first half of 2027.