Can Seagate Earnings keep justifying a massive AI-driven run, or is valuation finally becoming the market’s breaking point?

What Did Seagate Earnings Reveal?

Seagate Technology Holdings plc reported Q3 FY2026 results that underscored its transformation from legacy HDD vendor to AI-enabling infrastructure partner. Revenue surged 44.1% year-over-year to $3.11 billion, while non-GAAP EPS landed at $4.10 — well above analyst expectations. Gross margin expanded sharply to 47.0%, up from 36.2% in the prior-year quarter, marking the ninth consecutive quarter of margin expansion. CEO Dave Mosley emphasized that AI workloads are now the primary catalyst, citing qualification of HAMR-based Mozaic drives at major cloud providers including Meta and Microsoft. Unlike cyclical memory plays like Micron Technology (MU), Seagate’s build-to-order visibility extends through mid-2026 — a rare near-term revenue certainty in today’s volatile tech environment.

How Does Seagate Compare to AI Infrastructure Peers?

Stanley Druckenmiller’s Duquesne Family Office disclosed positions in three AI-infrastructure names in its March 31, 2026 13F filing: Broadcom (AVGO), Seagate Technology Holdings plc, and Micron Technology (MU). Broadcom remains the largest holding, but Seagate ranks second — signaling strong conviction in the storage layer’s structural upside. While NVIDIA dominates AI compute and Micron supplies critical HBM, Seagate owns the high-capacity, energy-efficient storage bottleneck. RBC Capital Markets recently reiterated its ‘Outperform’ rating on Seagate, citing ‘unmatched margin scalability in the AI storage stack’ and raising its price target to $925. Citigroup, meanwhile, noted that ‘Seagate Earnings reflect a durable inflection — not a one-off,’ though it trimmed its upside potential due to valuation concerns.

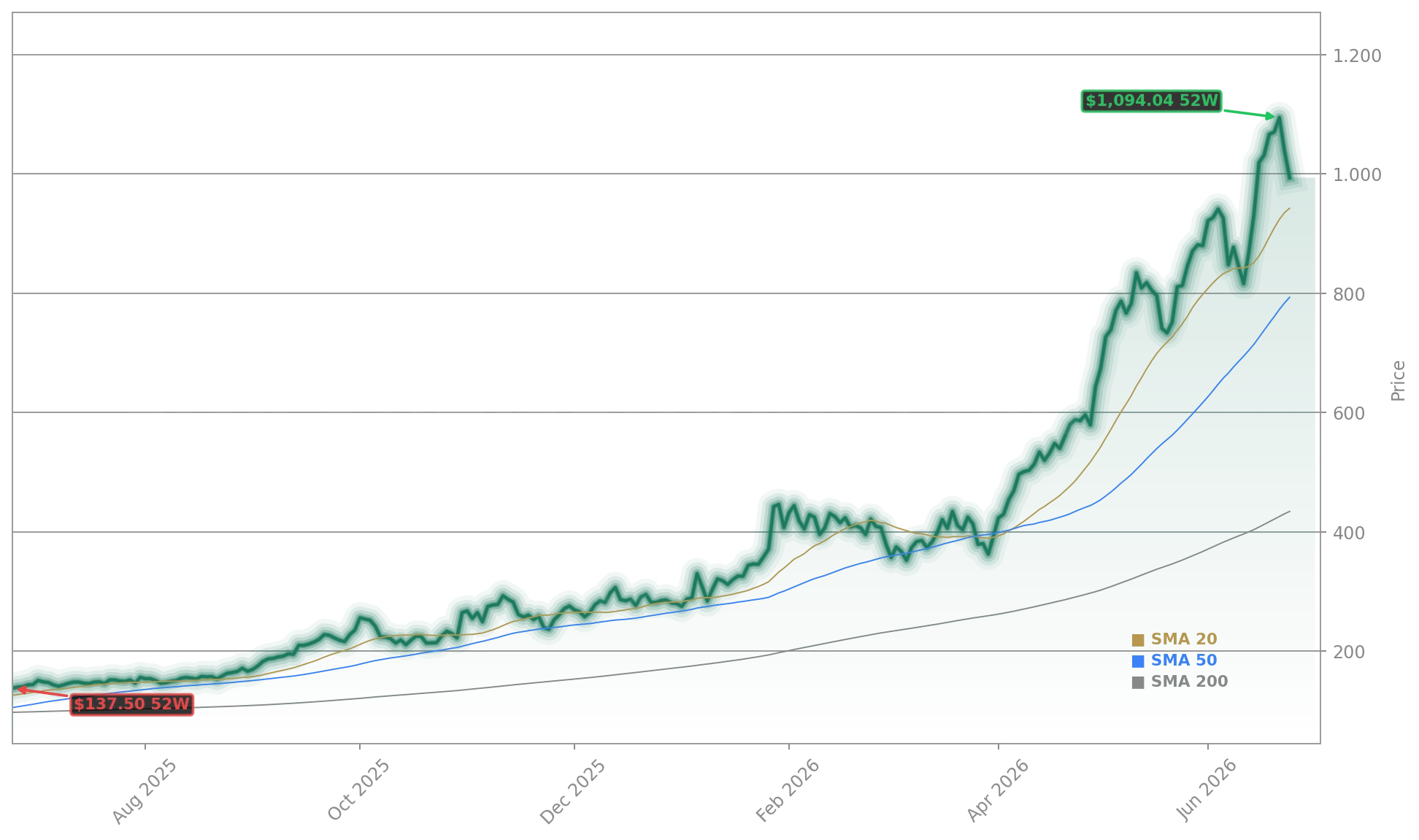

Is Seagate Earnings Sustainable Amid Rising Valuation Pressure?

At $1057.00 as of Wednesday, June 24, 2026, Seagate Technology Holdings plc trades 278% above its 2025 year-end price — and 17.6% above the $898.09 average analyst target. Its forward P/E of 44x sits well above the NASDAQ Composite’s 28x and even above the S&P 500’s 21x. The stock dipped 6.31% recently — from $1,094.04 to $1,025.01 — as memory and storage names sold off ahead of Micron’s earnings. That pullback highlights mounting investor sensitivity: Seagate Earnings are strong, but the market increasingly demands proof that margins and revenue scale beyond 2026. Unlike Apple or Tesla, which face hardware saturation risks, Seagate’s HAMR roadmap remains under-penetrated — with just 12% of cloud datacenter HDD shipments currently HAMR-enabled, per industry estimates.

What’s Next for Seagate Earnings and AI Storage?

Seagate’s next catalyst lies in HAMR adoption acceleration and the ramp of its 52TB Mozaic 3.0 drives — expected to ship in volume by Q4 FY2026. The company’s nine-quarter margin streak suggests pricing power and supply chain discipline are intact. Yet valuation remains the wildcard: with a $23 billion market cap, Seagate is now larger than many legacy enterprise software firms — and trades at a premium to peers like Western Digital (WDC). Goldman Sachs maintains its ‘Buy’ rating but warns that ‘any softness in cloud capex guidance could trigger a sharp de-rating.’ Meanwhile, the broader NASDAQ is up 14% year-to-date — meaning Seagate’s 278% surge has massively outpaced the index. That divergence makes Seagate Earnings not just a company story, but a barometer for AI infrastructure sentiment across Wall Street.

A new era of structural growth as AI applications amplify data creation.— Dave Mosley, CEO of Seagate Technology Holdings plc

Related Coverage: Has Seagate’s AI-driven rally finally outrun reality, or is this 6.7% drop just a reset before the next leg higher? Seagate Forecast: Stock Drops 6.7% on Valuation Warning. Can Rigetti Quantum Strategy survive a brutal reality check as investors demand proof that quantum ambition can finally become revenue? Rigetti Quantum Strategy Falls 10% as Risks Keep Building.