Can Seagate’s AI storage boom still justify a four-digit stock price after a sharp after-hours reversal?

Why Is Seagate Forecast So Bullish Now?

Morgan Stanley’s $1,035 price target reflects a fundamental re-rating of Seagate Technology Holdings plc — no longer viewed as a legacy storage vendor but as a critical AI infrastructure enabler. The firm maintained its Overweight rating and cited accelerating qualification of HAMR-based Mozaic drives with five of the world’s largest cloud providers. Q3 FY26 results — $3.11 billion in revenue (up 44.1% year over year), $4.10 non-GAAP EPS (vs. $3.50 expected), and record 47% gross margins — validated the shift. Free cash flow hit $953 million, and 88% of capacity shipped to data centers. This isn’t incremental growth — it’s structural. The Seagate Forecast now assumes 40–50% annual HDD demand growth through 2028, while supply expands only 30–35%, creating a 10–15% supply deficit in 2026.

How Does Seagate Compare to Memory Peers?

While NVIDIA dominates AI compute and Micron leads in DRAM, Seagate Technology Holdings plc is capturing outsized gains in the storage layer — a segment Wall Street previously undervalued. The Roundhill Memory ETF (MEMX), up 134% since launch, includes both Seagate and Western Digital alongside Micron (28% weight), SK Hynix, and Samsung. Unlike pure-play memory firms, Seagate’s differentiated HAMR technology enables >30TB drives — essential for AI training clusters where cost-per-terabyte remains decisive. With HDD pricing at $14.30–$14.90/TB today and targeting $25–$30/TB by 2027–2028, Seagate’s margin trajectory outpaces peers like Western Digital and even memory leaders facing DRAM oversupply risks.

What’s Holding Seagate Forecast Back?

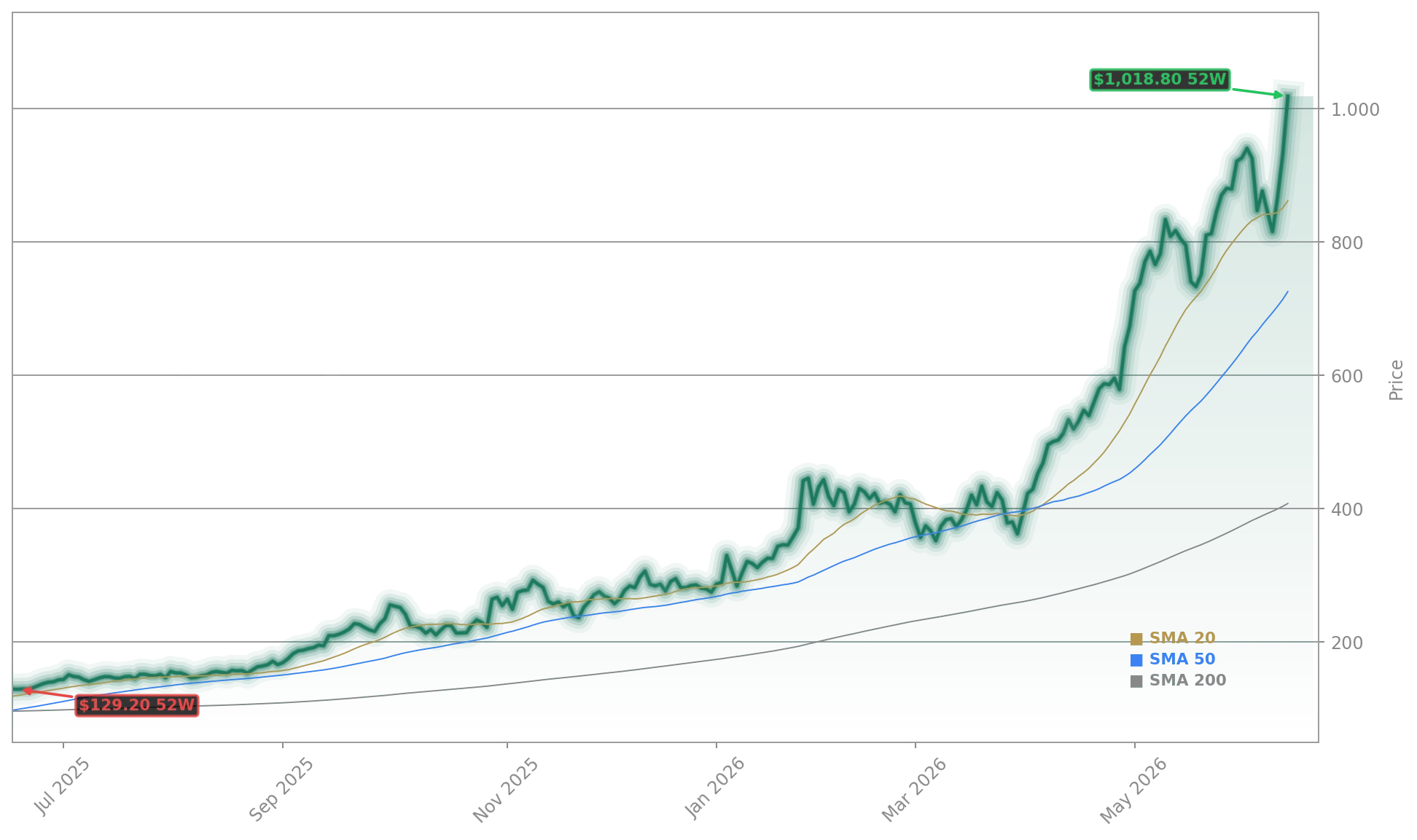

Despite bullish fundamentals, the Seagate Forecast faces near-term headwinds. Shares are trading 9% below their $966.80 52-week high — a consolidation phase after a 647.88% surge over 12 months. A beta of 2.083 amplifies volatility, and insider selling has dominated recent transactions (177 trades, majority sell). Wall Street consensus remains anchored at $877.68 — $53 below current price — reflecting lagging models. Yet Morgan Stanley’s upgrade joins a broader analyst shift: 83% of coverage is Buy or Strong Buy, with only one Strong Sell. The real risk isn’t fundamentals — it’s hyperscaler capex digestion. A pause in AI infrastructure spending would pressure valuations, though Q4 FY26 guidance ($5 EPS, $3.45 billion revenue) signals continued momentum.

Is $1,000 Per Share Realistic?

Yes — and it’s mathematically close. At $931.04 and forward EPS of $18.62, Seagate Technology Holdings plc trades at ~50x forward P/E. Hitting $1,000 requires just 7.4% appreciation — or ~4x P/E expansion to 54x. That’s manageable given gross margin expansion (36.2% → 47%) and EPS growth ($2.59 in Q4 FY25 → $4.10 in Q3 FY26 → $5 guided for Q4). Morgan Stanley’s $1,035 target implies $1,039.94 in its bull case, modeled for October 13, 2026. Three catalysts must align: Q4 earnings beat, volume ramp of HAMR drives in H2 2026, and constructive hyperscaler capex commentary. Absent a broad AI spending pullback, the path is clear.

What Does This Mean for S&P 500 and NASDAQ Investors?

For U.S. portfolios, Seagate Technology Holdings plc represents a rare high-beta, high-conviction AI infrastructure play outside the usual chip and cloud software cohorts. Its 6,092% 10-year return dwarfs the S&P 500’s ~150% and NASDAQ’s ~420% over the same period. With a $226.32 billion market cap, Seagate is no small-cap story — it’s a core holding for AI infrastructure exposure. Its performance also lifts memory-related ETFs like MEMX and influences broader semiconductor and data center supply chain sentiment. As hyperscalers like Meta and Microsoft expand AI training clusters, Seagate’s role — alongside Tesla and Apple data center initiatives — grows more strategic. This isn’t cyclical; it’s a multi-year storage inflection.

Related coverage: Seagate’s early redemption of convertible notes signals strengthening balance-sheet confidence amid surging AI demand — read more in Seagate Convertible Notes +6.7% Surge as AI Demand Builds. Meanwhile, AMD’s recent acquisition aims to solve AI memory bottlenecks — a complementary development that reinforces the broader data infrastructure theme explored in AMD Acquisition +7.1% as Mext Deal Fuels AI Memory Push.

Seagate Technology Holdings plc remains on track to redefine storage’s role in the AI stack. For investors, the Seagate Forecast is no longer speculative — it’s quantified, catalyst-driven, and accelerating. The next quarterly earnings report will confirm whether HAMR volume orders are scaling as expected. For aggressive growth portfolios, this is a defining infrastructure position to hold.

Seagate is entering a new era of structural growth as AI applications amplify data creation and support sustained storage demand.— Dave Mosley, CEO of Seagate Technology Holdings plc

Fazit folgt.