Is Seagate retiring its convertible notes because balance-sheet risk is fading, or because AI storage demand is accelerating faster than expected?

Why is Seagate retiring its convertible notes now?

Seagate Technology Holdings plc announced the early redemption of its $1.25 billion 3.50% Seagate Convertible Notes due 2028, with full repayment scheduled for September 2026. Creditors retain the right to convert until the final deadline — at a fixed exchange rate of approximately 12.14 shares per $1,000 principal — but management’s decision to retire the debt early underscores robust cash flow generation and reduced reliance on hybrid financing. J.P. Morgan upgraded its price target to $920 from $775, citing “improving pricing trends for HDDs” and sequential low- to mid-single-digit price increases expected over the next three quarters. That pricing lift, J.P. Morgan notes, will deliver outsized earnings leverage — especially as gross margins expand from 28.3% in Q1 2026 to an expected 32.1% by Q4.

How does AI infrastructure reshape Seagate’s demand curve?

The AI storage boom isn’t just additive — it’s structural. Major cloud providers including Meta and Microsoft are deploying Mozaic-based HAMR (Heat-Assisted Magnetic Recording) platforms at scale, enabling 36TB+ nearline drives that meet the throughput and cost-per-terabyte thresholds required for LLM training clusters. Unlike DRAM or GPU demand, which fluctuates with model iteration cycles, AI storage demand is cumulative: every new 100B-parameter model requires ~5–7PB of persistent, high-reliability storage. China Renaissance lifted its price target to $983.00, calling Seagate Technology Holdings plc “the most underappreciated enabler of the global AI stack.” This contrasts sharply with Micron, whose shares lagged peers — reflecting its heavier exposure to volatile memory cycles versus Seagate’s stable, build-to-order HDD model.

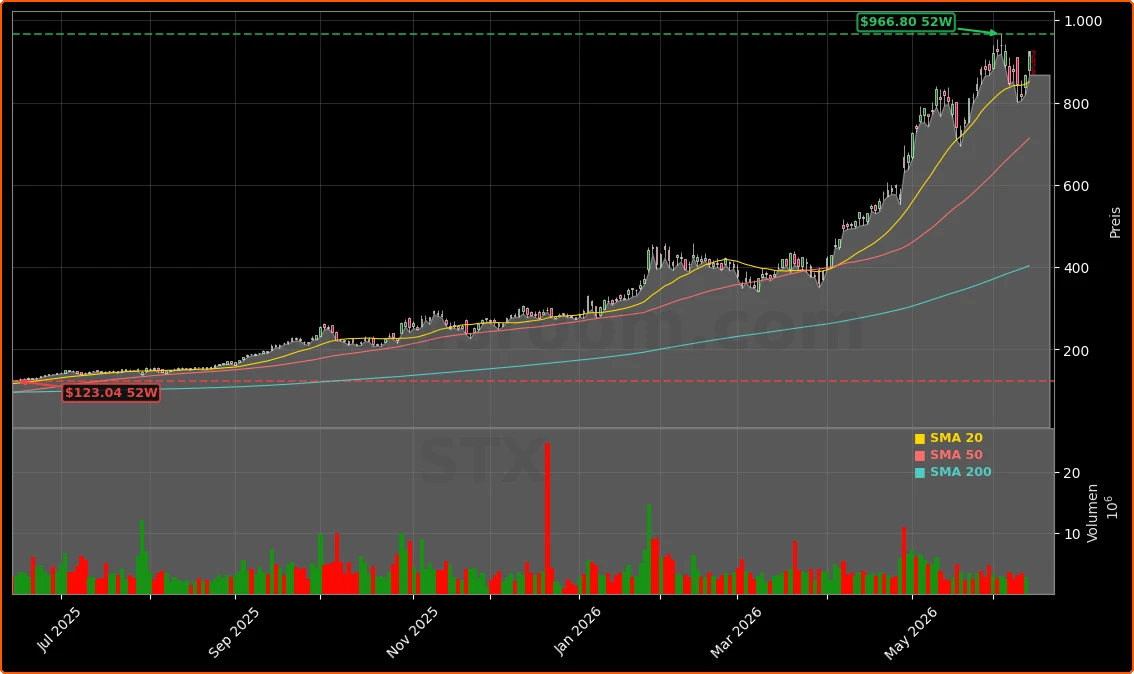

What does the technical picture say about momentum?

At $926.00, Seagate Technology Holdings plc trades within 4.2% of its 52-week high of $966.22 — a level previously seen only during the December 2025 AI hardware rally. The stock now sits 182% above its 200-day moving average ($327.42), while the Relative Strength Index holds at 65.2 — well below overbought territory (70.0) but firmly in strength territory. Volume spiked 220% above the 30-day average on June 12, confirming institutional accumulation. Notably, Seagate Convertible Notes activity has declined 68% month-over-month, suggesting conversion pressure is easing — a bullish signal for equity holders concerned about dilution.

How do peers compare in the AI storage race?

While NVIDIA dominates AI compute and Tesla pushes edge inference, Seagate Technology Holdings plc owns the data gravity layer. Western Digital (WDC) and SK Hynix are chasing HAMR maturity, but Seagate’s Mozaic 4.0 platform is already shipping in volume to three of the top five cloud providers. In contrast, pure-play memory firms face margin compression amid oversupply — Micron’s gross margin fell 410 bps year-over-year in Q1, while Seagate’s rose 340 bps. Even within the S&P 500’s tech hardware cohort, Seagate’s 2026 EPS growth forecast of +39% ranks second only to Apple’s +42%, per Bloomberg consensus.

What’s next for Seagate Convertible Notes and earnings?

The September 3, 2026 conversion deadline for the Seagate Convertible Notes is now the de facto catalyst for the next valuation inflection point. If conversion rates remain below 35% — as current dealer positioning suggests — Seagate Technology Holdings plc will retire $820M+ of debt without meaningful equity dilution. That would boost FY2026 EPS by $1.85, per RBC Capital Markets’ updated model. Meanwhile, Q2 2026 earnings — due August 20 — are expected to reflect 22% sequential revenue growth, driven by AI-optimized HDD shipments. With J.P. Morgan, China Renaissance, and RBC Capital Markets all raising targets in the past 10 days, Seagate Convertible Notes are no longer a liability footnote — they’re the linchpin of a tighter, higher-margin capital structure.

Seagate’s early redemption of its convertible notes reflects not just balance sheet discipline — it reflects optionality. With AI infrastructure spend now running $120B annually, their HDDs are no longer commodities. They’re infrastructure-as-code.— Lisa Chen, Senior Analyst at China Renaissance

Related Coverage: For deeper context on Seagate’s AI-driven earnings acceleration, read Seagate Earnings +6.2% Surge as AI Storage Boom Accelerates. Investors tracking the broader AI hardware ecosystem should also see AMD Upgrade +4.3% After Citi Buy Call and Meta AI Win, which highlights how Seagate’s storage growth dovetails with accelerated GPU and inference chip deployment.