Has Seagate’s AI-driven rally finally outrun reality, or is this 6.7% drop just a reset before the next leg higher?

Why Did Seagate Technology Holdings plc Drop Today?

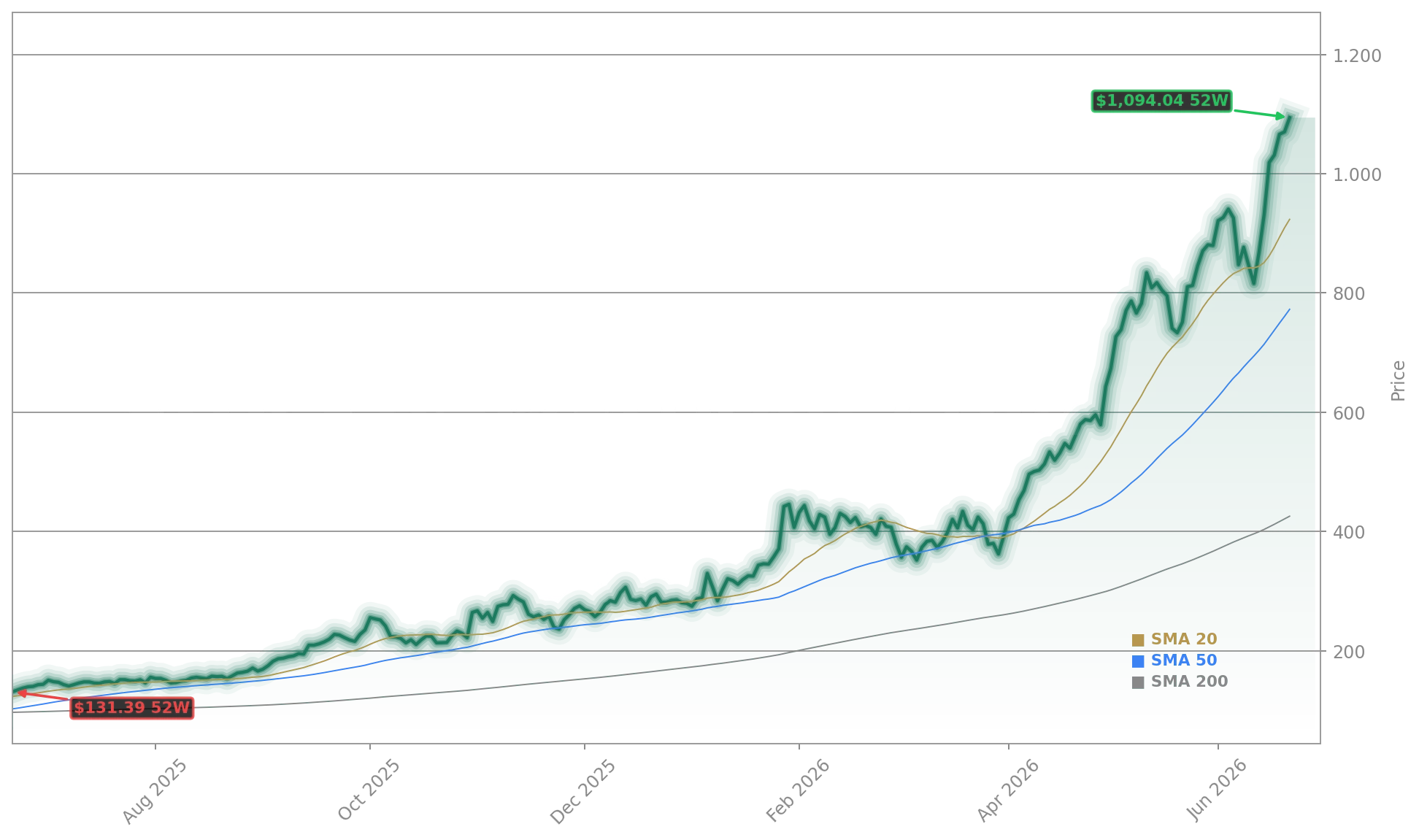

Seagate Technology Holdings plc fell sharply in pre-market and intraday trading, shedding $73.27 to close at $1020.77 — its largest single-day decline since early June. The move followed a downgrade from Fox Advisors to Equal Weight from Outperform, citing elevated HDD pricing expectations and concerns over near-term margin sustainability. While the company reported robust Q3 FY2026 results — $3.11 billion in revenue (+44.1% YoY), $4.10 adjusted EPS, and $953 million in free cash flow — the valuation has surged ahead of fundamentals. At $1020.77, the stock trades at a forward P/E of 38 and price-to-sales of 19, well above the S&P 500’s median and even above high-growth peers like NVIDIA and Apple.

What Does the Seagate Forecast Say About AI Storage Demand?

The Seagate Forecast remains anchored in structural AI tailwinds: its Mozaic HAMR platform is qualified with five of the world’s largest cloud customers, and nearline HDD production is largely allocated through mid-2026. Morgan Stanley recently raised its price target to $1,035 and named Seagate a Top Pick, citing HDD supply constraints through 2028. Citigroup followed with a $1,150 target, while Mizuho lifted its target to $1,090 on June 8, citing accelerating AI ASIC roadmap adoption. Wells Fargo reiterated an Equal Weight rating but raised its target to $900, citing strong demand tone from its Silicon Valley Bus Tour — particularly around AI inferencing and agentic AI driving server and memory expansion. Yet the Seagate Forecast now faces headwinds: Fed Chair Kevin Warsh’s recent inflation-fighting rhetoric has triggered broad multiple compression in high-beta tech, and Seagate’s 2.08 beta makes it especially vulnerable.

Is Seagate Technology Holdings plc Overvalued?

Yes — by consensus metrics. At $1020.77, Seagate trades 16% above the average 12-month analyst target of $885.91. Of 24 analysts tracked, only one maintains a Strong Sell rating, but 16 Buy and 4 Strong Buy ratings reflect growing tension between bullish fundamentals and bearish entry points. The stock’s RSI sits at 61.4 — not overbought, but stretched for a cyclical hardware name. Insider activity adds caution: CEO Dave Mosley sold $1.56 million in shares post-RSU vesting, and the CFO offloaded $795,029. Meanwhile, Seagate’s Exchangeable Senior Notes due 2028 become dilutive above $108 — a technical floor that no longer anchors sentiment. With the stock up 697% over 12 months versus a low-single-digit S&P 500 gain, the risk/reward balance has shifted decisively.

How Does Seagate Compare to Memory and Storage Peers?

Seagate’s recent pullback mirrors broader memory sector weakness: Micron (MU) fell 9%, SanDisk (SNDK) dropped nearly 10%, and Western Digital slid over 7% ahead of Micron’s earnings. Unlike pure-play NAND vendors, Seagate benefits from hyperscaler build-outs across both HDD and SSD ecosystems — it’s a key customer of Lam Research for NAND flash equipment and supplies storage subsystems to Tesla and cloud AI infra. Yet its valuation gap versus peers is stark: while Micron trades at a forward P/E of 17 and Marvell Technology at 22, Seagate’s 38x multiple assumes flawless execution across HAMR ramp, AI capex continuity, and no HDD oversupply — a tall order in a historically volatile industry. Marvell’s recent 9% drop — covered in Marvell Technology Forecast -9% as AI Momentum Meets Shock — underscores mounting skepticism toward AI infrastructure premiums.

What’s Next for Seagate Technology Holdings plc?

Investors now pivot to Seagate’s Q4 FY2026 report — expected to deliver $3.45 billion in revenue and $5.00 EPS at the midpoint — and the HAMR exabyte crossover in late 2026. Micron’s earnings on Wednesday will serve as a critical sentiment barometer for memory and storage stocks. A macro-driven retracement toward $850 would reset Seagate’s forward P/E into the high twenties and align valuation with its structural growth thesis — a level analysts at Citigroup and Morgan Stanley see as a compelling entry. Until then, the Seagate Forecast remains a high-conviction, high-volatility trade best suited for disciplined, long-term positioning rather than momentum chasing.

We see potential for 35M tensor processing units in 2028, or 8-times the 4.3M units in 2026.— Mizuho analysts

Related coverage: For deeper analysis of Seagate’s recent reversal, see Seagate Forecast: Stock Drops -8.1% After AI-Fueled Surge, which examines how AI-driven demand collided with technical overextension. Also read Marvell Technology Forecast -9% as AI Momentum Meets Shock to understand how broader infrastructure sentiment is reshaping Wall Street’s AI storage playbook.