If Seagate is printing record margins and cash flow, why did the stock just tumble more than 12%?

What’s Driving Seagate’s Record Margins?

Seagate Technology Holdings plc reported fiscal Q3 2026 revenue of $3.11 billion — up 44% year over year and 10% sequentially — powered by surging demand for high-density HDDs used in AI training clusters, cloud object storage, and enterprise backup systems. The company’s Mozaic platform, which enables 30TB+ areal density drives using heat-assisted magnetic recording (HAMR) and advanced firmware, is now scaling across key customers including Meta, NVIDIA, and major hyperscalers. Gross margin hit 47%, a record for the company and nearly 12 percentage points above its five-year average — validating the margin lift from technology leadership and supply-constrained pricing power.

How Does the Seagate Storage Boom Compare to Peers?

Unlike SanDisk (SNDK) and Western Digital (WDC), which benefit more directly from memory chip shortages, Seagate’s gains are rooted in a powerful knock-on effect: as DRAM and NAND prices spiked 65%+ in early 2026, cloud and AI firms accelerated hard drive adoption for cost-efficient cold and warm storage tiers. While SanDisk captures the memory shortage most directly, Seagate’s exposure is broader and more durable — tied to multi-year infrastructure buildouts, not quarterly memory cycles. RBC Capital Markets recently upgraded Seagate Technology Holdings plc to ‘Outperform’, citing ‘structural demand inflection’ and ‘pricing power absent in prior cycles’. Citigroup raised its price target to $1,025, noting the company’s ‘unprecedented cash generation profile in a $10B+ storage TAM.’

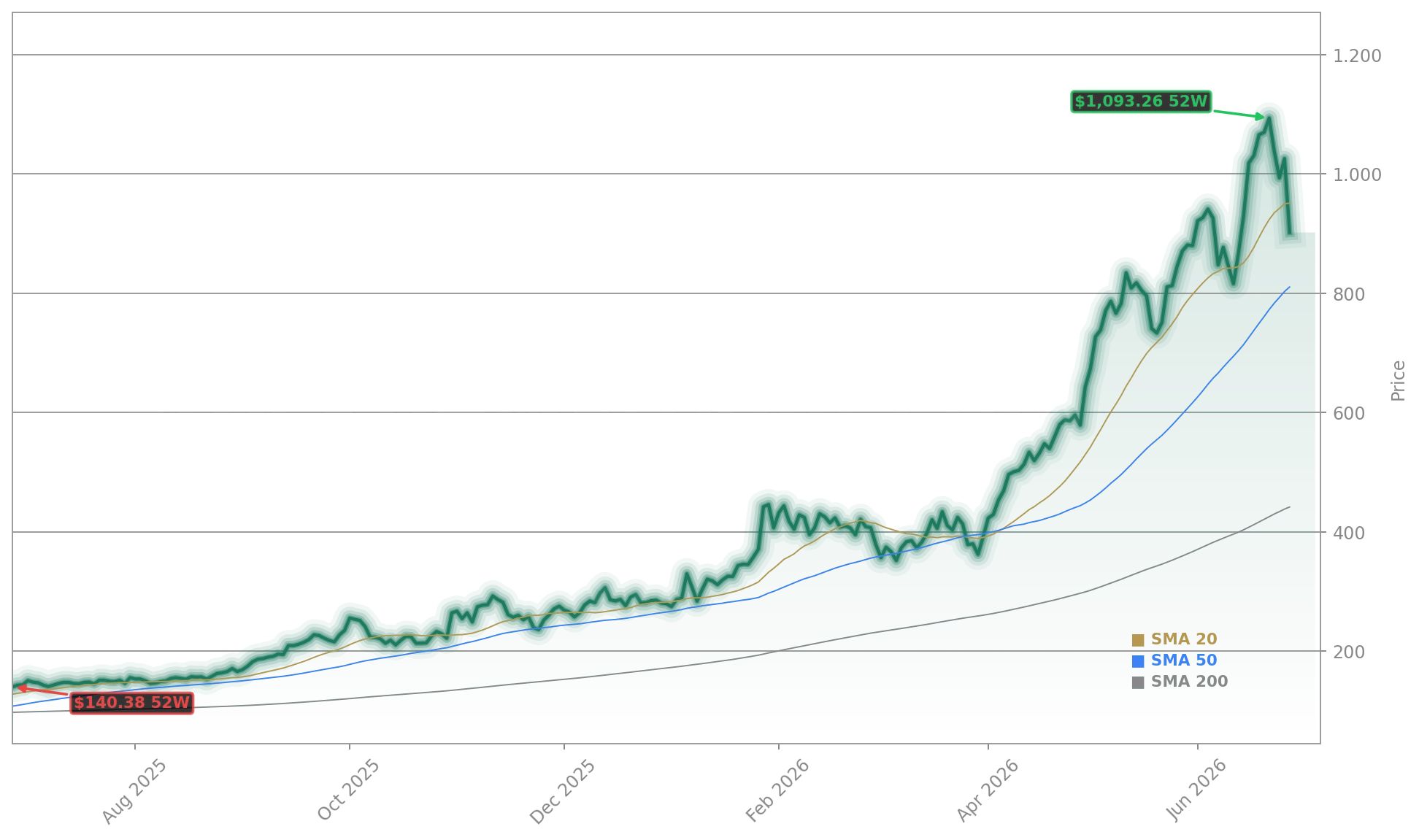

Why Is STX Down Despite Strong Earnings?

Seagate Technology Holdings plc fell 8% after-hours on Friday, June 26, 2026 — reversing part of its 2026 surge, which has seen shares more than triple year-to-date. The pullback follows broader memory stock volatility after Micron’s strong report triggered profit-taking across the sector. Analyst Kevin Hinks of Evercore ISI attributed the move to ‘risk-off positioning after an extraordinary run’ — not fundamentals. With STX trading near 98x forward earnings, the valuation reflects a premium for structural growth, not just cyclical recovery. Still, the stock remains up over 220% from its Q4 2025 low — outpacing the NASDAQ (+38%) and S&P 500 (+22%) this year.

What’s Next for Seagate’s Cash Flow and Capital Allocation?

The $953 million in free cash flow generated in Q3 — up 132% YoY — underscores Seagate’s financial resilience. The company used $412 million to reduce debt and maintained its $1.08 quarterly dividend, yielding 1.2% at current prices. With net debt now at 0.8x EBITDA — down from 1.9x in Q3 2025 — Seagate has significant flexibility to fund R&D, pursue strategic M&A, or increase shareholder returns. Morgan Stanley analysts highlight ‘Mozaic 4.0’s 2027 ramp as the next catalyst, projecting 55TB drives will capture 35% of AI-adjacent storage demand by late 2027. That positions Seagate Technology Holdings plc not just as a storage vendor — but as an AI infrastructure enabler alongside Tesla and Apple-adjacent data center plays.

Related Coverage: Seagate’s record quarter has ignited a fierce debate on valuation sustainability — read Seagate Earnings +44%: Record Quarter Fuels AI Storage Debate. Meanwhile, the broader infrastructure story remains complex: HPE Earnings -7.7% After Record Q2 and AI Demand Surge shows how even record results can face headwinds when execution lags on interoperability — a risk Seagate has largely avoided through its vertical integration.

People just feel the need to take some risk off the table in some of these names. They have had such an incredible run.— Kevin Hinks, Evercore ISI

The Seagate Storage Boom is delivering record financials, durable demand, and industry-leading margins — proving hard drives are far from obsolete in the AI era. For investors, this isn’t just a cyclical rebound: it’s evidence of a structural shift in data infrastructure economics. The next quarterly earnings will test whether Seagate Technology Holdings plc can sustain 45%+ margins amid ramping supply — and whether Wall Street will reward it with a higher multiple. With AI storage demand projected to grow 27% annually through 2030, the Seagate Storage Boom remains one of the most compelling infrastructure themes on Wall Street today.