Can Verizon Joint Venture losses and a Dow exit mark a smart reset, or are they warning signs of deeper telecom weakness?

Why did Verizon Joint Venture trigger a $800M loss?

Verizon Communications Inc. confirmed it will contribute its international enterprise wireline and managed network services businesses into a new 50/50 joint venture with BT Group plc — to be named NewCo. Under U.S. GAAP, Verizon classifies these contributed assets as ‘held for sale,’ requiring an impairment charge. The company now expects a $700 million to $800 million loss in Q2 2026 — a non-cash, one-time accounting impact. While the Verizon Joint Venture is expected to be accretive to adjusted EBITDA for Verizon Business Group, the upfront hit weighed heavily on sentiment. Analysts at RBC Capital Markets noted the move ‘accelerates Verizon’s strategic refocusing on domestic wireless and fiber — but at near-term earnings cost.’

What does Dow removal mean for U.S. index funds?

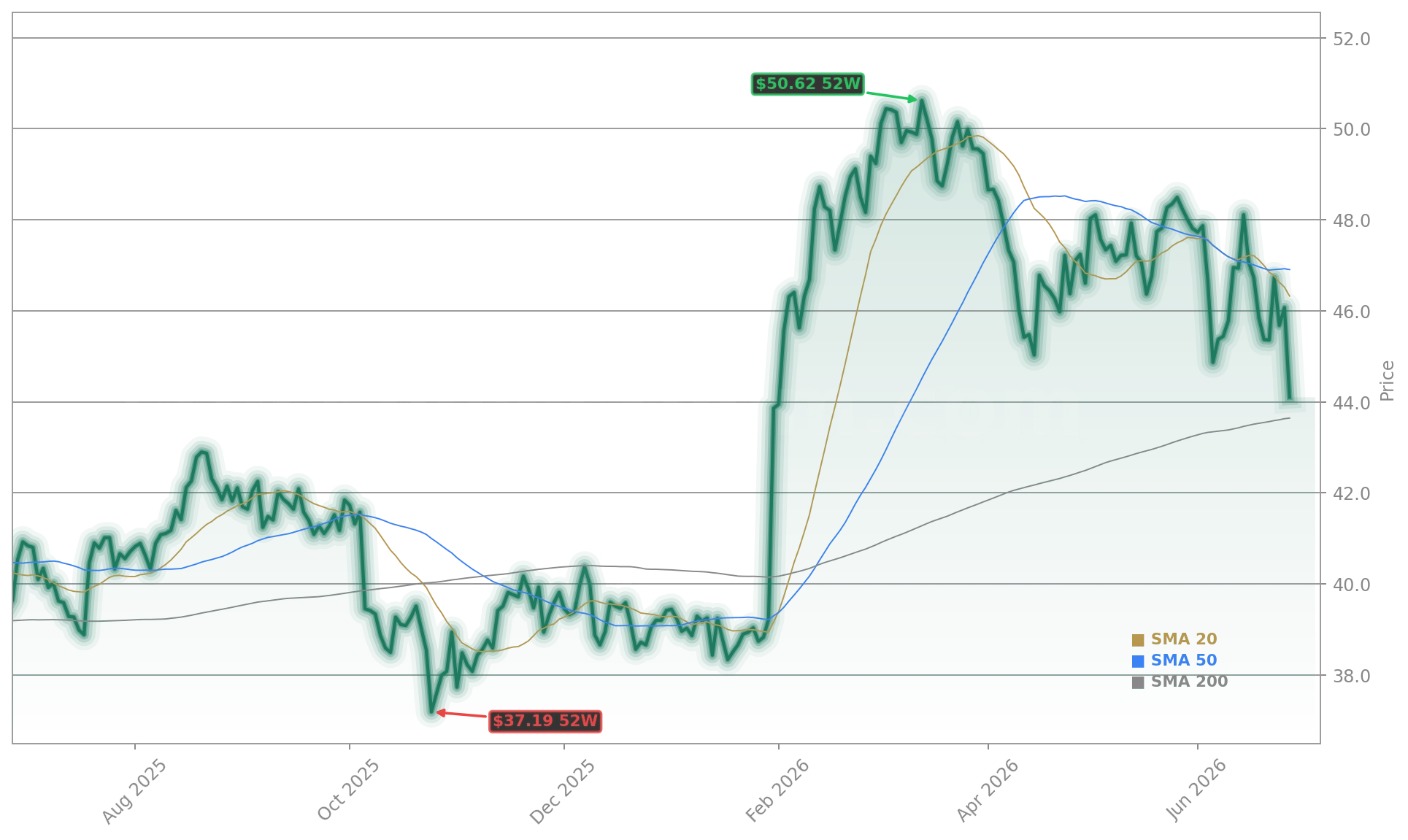

Verizon Communications Inc. exited the Dow Jones Industrial Average on Monday, replaced by Alphabet — a symbolic pivot toward digital infrastructure and AI. Because the Dow is price-weighted and Verizon’s share price hovered near $44, its influence on the index was minimal — just 0.5% — yet its removal triggered rebalancing pressure. Passive funds tracking the Dow were forced to sell VZ shares and buy GOOGL/GOOG, contributing to the stock’s 5.8% intraday decline. In contrast, Alphabet added $168 billion in market value on its first Dow day — more than Verizon’s entire $171 billion market cap. The shift underscores how Wall Street increasingly values scalable, high-margin tech platforms over capital-intensive telecom infrastructure.

How are rivals reshaping the telecom landscape?

Verizon’s challenges extend beyond internal restructuring. Comcast announced plans to split its broadband/mobile infrastructure from NBCUniversal and Sky — a move analysts at Citigroup called ‘a direct threat to Verizon’s enterprise and wholesale positioning.’ Meanwhile, Charter Communications and SpaceX are reportedly negotiating a mobile service powered by Starlink’s low-earth-orbit satellites — potentially disrupting rural and underserved markets where Verizon holds pricing power. Though Charter currently relies on Verizon’s network for its mobile offerings, a future standalone service could erode wholesale revenue. Notably, shares of Comcast (CMCSA) and Charter (CHTR) rose over 5% and 8%, respectively, while VZ fell — suggesting portfolio rotation toward higher-growth, lower-valuation peers.

Do fundamentals still support the 6.1% dividend?

Yes — but with rising caveats. Verizon Communications Inc. reaffirmed its full-year 2026 EPS guidance and declared its latest quarterly dividend of $0.7075 — sustaining an attractive 6.1% annualized yield. Institutional investors remain committed: Diamant Asset Management increased its stake by 4,771.9%, and Fort Washington Investment Advisors added 67,162 shares. Yet the dividend is increasingly viewed as compensation for stagnation. With wireless subscriber growth flat and fiber expansion slowing, Verizon’s core businesses face margin pressure from rising spectrum and network investment costs. Goldman Sachs maintains a ‘Neutral’ rating with a $50.59 price target — acknowledging the yield appeal but flagging ‘limited upside without meaningful new growth vectors.’

What’s next for Verizon Communications Inc.?

The Verizon Joint Venture is not just a financial transaction — it’s a strategic admission that international enterprise services no longer fit Verizon’s capital allocation priorities.— RBC Capital Markets

Verizon Joint Venture closes in Q4 2026, with integration and cost synergies expected to drive EBITDA growth in 2027. Meanwhile, Verizon Business Internet — offering fiber plus 4G/5G failover for SMBs — remains a key recurring-revenue pillar. The company also recently secured $1 billion in new FCC spectrum licenses, reinforcing its 5G leadership. But Wall Street’s patience is thinning: VZ now ranks as the weakest performer in the S&P 500 Telecommunication Services Index. With institutional ownership at 62.06% and analyst consensus leaning ‘Moderate Buy,’ the next catalyst will be Q2 earnings — due August 1 — where investors will scrutinize adjusted EBITDA trends, churn metrics, and guidance clarity on the joint venture’s long-term impact.