Can blockbuster Visa Earnings and a fresh buyback spree finally flip Wall Street’s bearish narrative on card networks?

How did Visa Earnings surprise Wall Street?

Visa Inc. comfortably topped analyst forecasts for its fiscal second quarter, underscoring the strength of its global payments network even as markets worry about consumer fatigue. Adjusted earnings came in at $3.31 per share, up from $2.76 a year earlier and ahead of the roughly $3.10 consensus. Net revenue climbed 17% to $11.2 billion, also beating expectations around $10.75 billion.

Growth was broad-based. Total payment volume increased 9%, while cross‑border volume – a key profit driver tied to travel and e‑commerce flows – rose 12%. Processed transactions also advanced 9%, highlighting that consumers and businesses are still actively using cards and digital payment credentials despite inflation, higher interest rates and geopolitical tensions. On the earnings call, finance chief Christopher Suh pointed to an 8% year‑over‑year increase in US payment volume, calling it evidence of “resilience in consumer spending.”

The latest Visa Earnings report reinforces the company’s long‑standing bull thesis: powerful network effects, strong pricing power and high incremental margins. With its scale across consumer payments, business solutions, money movement and value‑added services, Visa continues to convert modest volume growth into outsized profit gains.

How is the stock reacting on Wall Street?

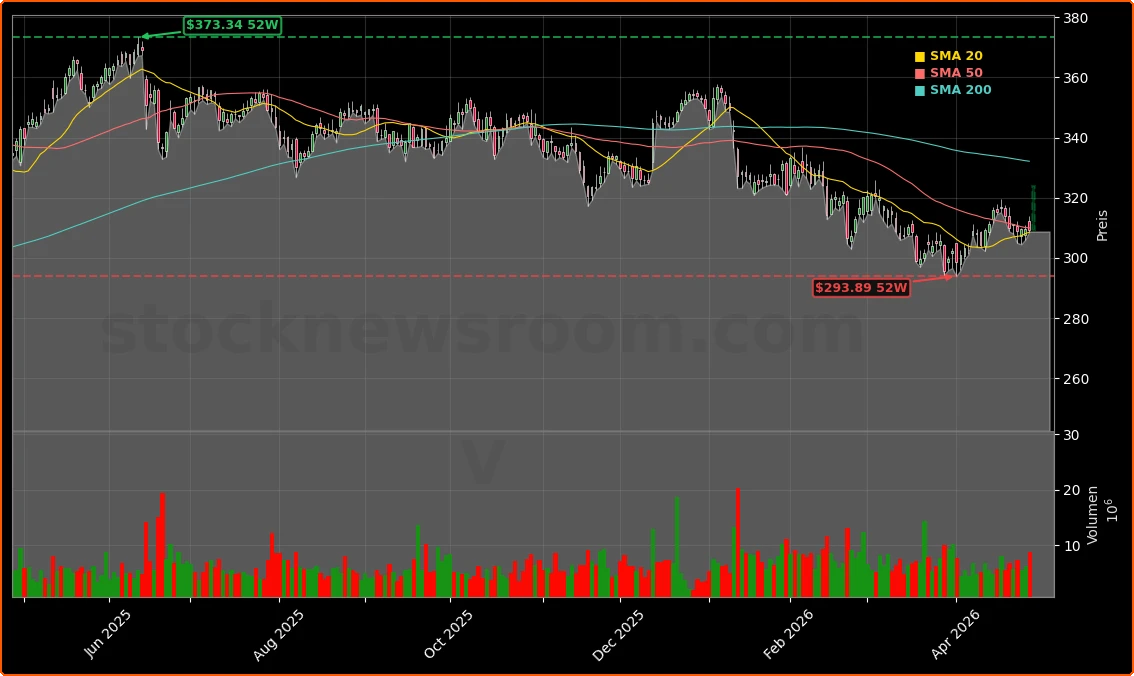

Investors initially punished the stock earlier in the week, but the earnings release has clearly shifted sentiment. On Tuesday, Visa closed at $325.00 and edged 0.11% lower to $309.30 during the prior session’s trading, leaving the shares roughly 12% lower year‑to‑date and lagging the S&P 500. Following the earnings beat, the stock jumped in late‑Tuesday US trading and is quoted at about $323.72 in early Wednesday pre‑market action, up roughly 4.7% from the previous close.

The move mirrors broader after‑hours reactions across large‑cap earnings names. Companies like Apple and NVIDIA have shown in recent quarters that clean beats on both revenue and EPS, coupled with solid outlook commentary, can quickly reset investor expectations even for mega‑cap incumbents. Visa’s rally suggests that investors had grown overly cautious on the card networks amid headlines about stablecoins and regulatory pressure on interchange fees.

Beyond the headline numbers, the board also underscored confidence in long‑term cash generation by authorizing a new $20 billion multi‑year share repurchase program and maintaining a quarterly cash dividend of $0.67 per share. For income‑oriented portfolios and total‑return investors alike, that capital return profile remains a key part of the investment case.

How do Visa Earnings stack up against rivals?

The payments sector has been a paradox in 2026. Visa Inc., Mastercard and American Express have all delivered solid results yet trade well below recent highs as investors reassess the durability of card economics. Double‑digit revenue and profit growth at Visa stands in contrast to the double‑digit stock price declines the group has posted this year, creating a valuation gap that some long‑term investors may see as an opportunity.

While the latest Visa Earnings beat highlights the company’s operational strength, it also sharpens the comparison with secular growth names in technology. Digital enablers such as NVIDIA or platform companies like Apple often command higher earnings multiples, but Visa’s cash‑rich model, relatively low capital intensity and consistent buybacks offer a very different, more cash‑flow‑driven profile. For diversified US portfolios balancing growth and quality, the stock now sits at the intersection of both themes.

Institutional ownership patterns also tell a story. Some quality‑focused funds have taken profits or rotated away from payment networks in recent years, but the underlying business momentum suggests those exits were more about portfolio construction than a collapse in fundamentals. The latest quarter could prompt fresh comparisons between card networks and leading fintechs battling for transaction flows.

What are the main risks for investors now?

Despite an impressive quarter, Visa is far from risk‑free. Stablecoins and alternative payment rails remain the most talked‑about structural threat. Blockchain‑based solutions promise lower transaction fees and faster settlement for merchants, potentially eroding the premium economics that card networks enjoy. New products like Bitcoin‑backed Visa cards show how crypto and traditional rails are increasingly intersecting, underscoring both opportunity and disruption risk.

Regulation is another overhang. Proposals in Washington to limit credit‑card interest rates and ongoing scrutiny of interchange fees could pressure revenue growth or margins over time. Any material rule changes from US regulators, or from authorities in Europe and other major markets, would likely trigger multiple compression across the sector regardless of near‑term performance.

Macro headwinds are a further wildcard. Rising oil prices, geopolitical instability and the risk of a US or global recession could weigh on consumer discretionary spending. Some banks, including Wells Fargo, have already flagged early signs of softer card spending trends. If that accelerates, the volume engine that powered this quarter’s beat could slow just as regulatory and competitive pressures intensify.

Our results reflect resilience in consumer spending and the strength of our global network.— Christopher Suh, Chief Financial Officer of Visa Inc.

For now, though, Visa’s execution is clearly outpacing these concerns. The network continues to extend into new flows, business‑to‑business payments and value‑added services, reinforcing its relevance even as digital wallets and fintech challengers proliferate. Compared with more cyclical names like Tesla, Visa’s revenue stream is diversified across regions and categories, offering some resilience even in choppy markets.