Can Alibaba AI Strategy outrun geopolitics and weak consumer demand before Wall Street loses patience?

Why Is Alibaba AI Strategy Accelerating Now?

Alibaba Group Holding Limited is executing a full-stack AI build — from proprietary chips like the Yitian 710 and Pingtouge foundation models to AI-native logistics robots like ZeeBot, which climbs warehouse racks at 4 meters per second. Chairman Joe Tsai, speaking at VivaTech in Paris, affirmed the company’s $50 trillion total addressable market thesis and emphasized intentional breadth over early bets: ‘Figure out the winners later.’ This contrasts sharply with NVIDIA’s hardware-led dominance and Meta’s application-first rollout. Crucially, Alibaba’s token costs are estimated at roughly one-tenth of Western hyperscalers — a structural advantage in capital efficiency that could amplify margins if adoption scales. Yet the timing coincides with a Pentagon blacklist expansion on June 8, adding Alibaba to its 1260H list of alleged military-linked entities — a move Beijing’s Commerce Ministry has formally opposed.

How Is Wall Street Reacting to Alibaba AI Strategy?

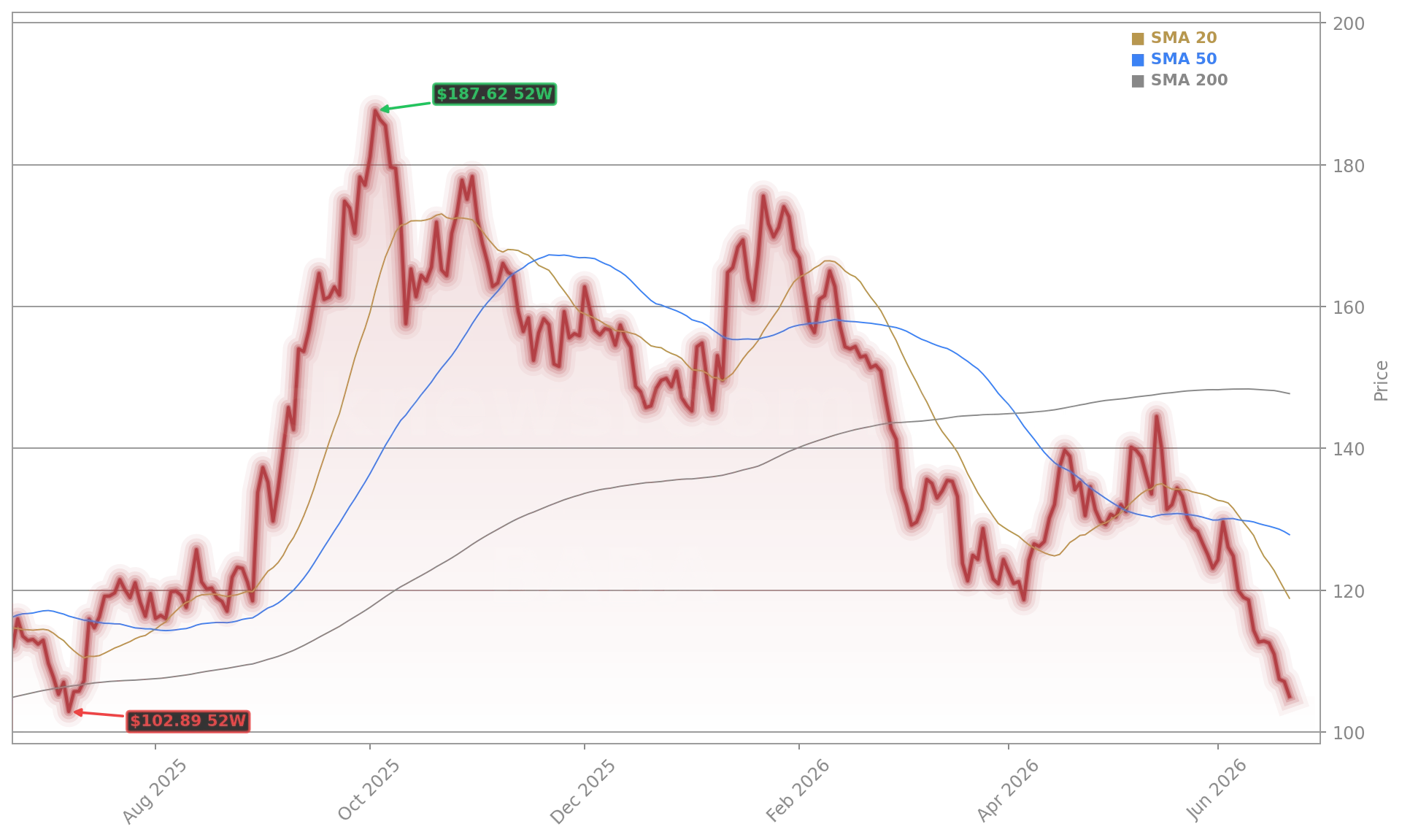

Investor sentiment remains split. While Goldman Sachs maintains its ‘Buy’ rating and highlights Alibaba as its top China internet stock for H2 2026, Citigroup has downgraded near-term e-commerce sales forecasts and sees muted 6- and 18-month revenue visibility. The stock’s five-day losing streak — including a 1.9% drop in Hong Kong trading — underscores skepticism. That divergence is stark against broader market action: the NASDAQ fell just 0.58% on June 22, while Alibaba underperformed even as six S&P 500 sectors advanced. Analysts point to two countervailing forces: Alibaba’s position atop China’s K-shaped recovery (strong exports, tech, and AI infrastructure) versus persistent weakness in domestic consumption and real estate — sectors that still weigh on overall MSCI China earnings, down 8% in Q1.

What Does the K-Shaped Recovery Mean for U.S. Portfolios?

For U.S. investors, Alibaba Group Holding Limited represents both a concentrated AI infrastructure play and a barbell risk. At 2.26% weight in the Vanguard FTSE Emerging Markets ETF — the largest China holding after Taiwan Semiconductor — BABA is a key conduit for passive exposure to Chinese tech’s AI acceleration. Yet its exposure is asymmetrical: while Western hyperscalers like Apple and Microsoft face capex headwinds, Alibaba’s lower-cost AI stack is insulated from those pressures. That structural decoupling matters. If U.S. cloud capex slows, Alibaba’s growth trajectory may remain intact — a dynamic not priced in by current valuations. With a forward P/E of 16.4x and EPS estimates rising to $2.51 for Q2 (up 22% YoY), the valuation looks reasonable — but only if geopolitical overhangs ease before the August 28 earnings report.

How Is Alibaba AI Strategy Driving Real-World Innovation?

Beyond rhetoric, Alibaba’s AI integration is tangible. Its Cainiao logistics unit deployed over 120 ZeeBot climbing robots in Dongguan — doubling labor productivity and improving efficiency 20–30% over legacy automation. Projects are now underway in the Netherlands, Spain, Guangzhou, and Hong Kong, with U.S. and Japanese pilots in discussion. This isn’t theoretical AI — it’s ROI-positive physical AI deployed at scale. Meanwhile, internal team-building rituals, like executives planting rice seedlings in symbolic alignment with ‘endure when it’s time to endure,’ signal cultural commitment to long-horizon bets. The message is clear: Alibaba AI Strategy isn’t just about models — it’s about reengineering operations, supply chains, and labor economics across its $25 billion e-commerce core to fund the next frontier.

What’s Next for Alibaba Group Holding Limited?

The laws of the fields are very simple: when the season arrives, you must plant when it’s time to plant, and endure when it’s time to endure.— Liu Zhenfei, Alibaba partner and chairman of Amap

The immediate catalyst is the August 28 Q2 2026 earnings report — the first to reflect meaningful AI infrastructure spend and early monetization signals. Goldman Sachs expects earnings inflection; Citigroup remains cautious on near-term sales. Meanwhile, Beijing’s retaliatory export controls on ten U.S. firms — including MP Materials and Oshkosh Defense — signal escalating friction, though analysts at The Asia Group describe the move as largely symbolic. For U.S. investors, the key question isn’t whether Alibaba’s AI strategy is credible — it is — but whether the market will reward execution before geopolitical risk recedes. With Q2 revenue estimates at $38.72 billion and a 12.5% YoY jump, the data may finally tip sentiment.