Can AT&T’s $45 billion capital return plan finally turn a cheap telecom giant into a serious income story again?

What Does $45 Billion Mean for AT&T Shareholder Returns?

AT&T Inc. has formally committed to returning $45 billion or more to shareholders from 2026 through 2028 — a figure that includes $8 billion in stock buybacks in 2026 alone. That commitment, reiterated during its Q1 2026 earnings call, marks a strategic pivot toward capital discipline after years of M&A-driven expansion. Unlike peers such as Verizon Communications — which maintains a lower yield and slower buyback pace — AT&T Inc. is now deploying free cash flow with surgical precision: $18 billion expected in 2026, rising to $21 billion by 2028. Analysts at Citigroup raised their price target to $30.25, citing the ‘unusually high degree of visibility’ on both cash flow and shareholder returns. For investors in the S&P 500’s Utilities & Telecom sector, this isn’t just about yield — it’s about predictable, quantifiable value creation.

How Is Fiber Growth Fueling AT&T Shareholder Returns?

Q1 2026 wasn’t just about capital allocation — it was about proof of execution. AT&T Inc. added 584,000 Advanced Connectivity internet customers, its strongest first quarter ever and a 32% YoY improvement. That surge followed the February 2, 2026 close of the Lumen Mass Markets fiber acquisition, expanding AT&T’s fiber footprint to over 37 million locations — up from 22 million just 18 months ago. With a clear path to 60 million by 2030, AT&T is now competing head-to-head with Verizon and T-Mobile not on spectrum alone, but on infrastructure density. This fiber flywheel supports pricing power, margin expansion, and — critically — stable, high-margin recurring revenue that funds AT&T Shareholder Returns without sacrificing investment grade credit. Morgan Stanley notes the fiber build is now ‘self-funding,’ reducing reliance on debt for future growth.

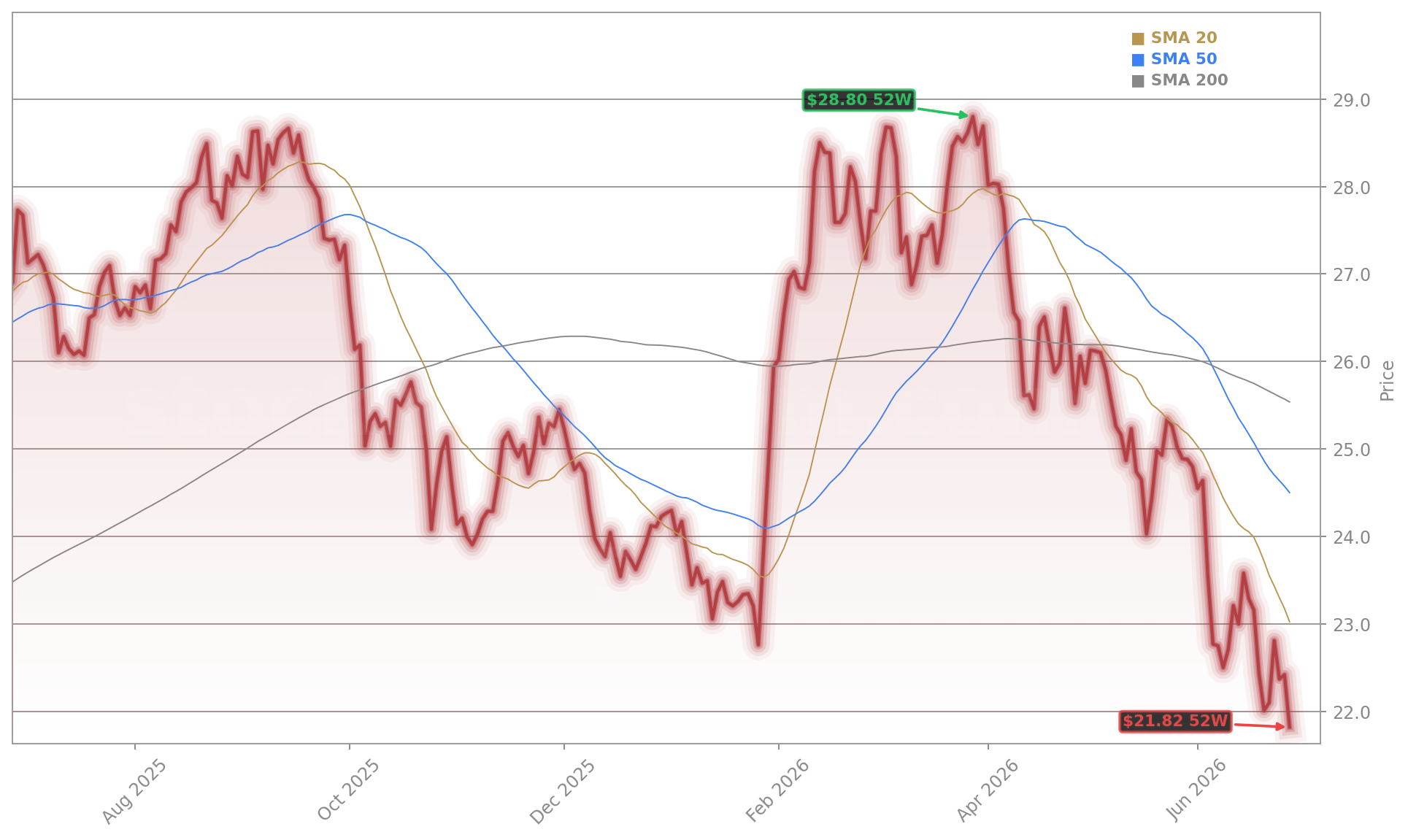

Why Is the Valuation So Compelling Now?

AT&T Inc. shares trade at $20.73 — down 17% year-to-date and near their 52-week low — despite a trailing P/E of just 8 and a forward P/E of 10. That’s well below the S&P 500 telecom average of 14.5 and even cheaper than legacy infrastructure peers like Cisco or Crown Castle. The dividend yield stands at 5.3%, backed by a $0.2775 quarterly payout unchanged since 2022 — a rarity in today’s inflationary environment. RBC Capital Markets upgraded AT&T Inc. to ‘Outperform’ in mid-June, highlighting ‘the confluence of yield, valuation, and execution clarity.’ With net debt-to-EBITDA at 2.71x — expected to rise modestly post-EchoStar integration — the balance sheet remains investment-grade, enabling continued buybacks even amid rising interest rates. This isn’t distressed value — it’s disciplined, infrastructure-backed income.

What Are the Risks to AT&T Shareholder Returns?

Not all market sentiment is bullish. Reddit’s r/wallstreetbets shifted bearish on June 26–27, citing concerns over SpaceX’s Starlink mobile expansion and legacy wireline revenue declines of over 20% annually. While Starlink remains a long-term wildcard — not yet a material revenue threat — AT&T Inc. is responding with aggressive fiber densification and bundling. More pressing is leverage: net debt-to-EBITDA is projected to approach 3.2x by late 2026. Still, with $18 billion+ in expected 2026 free cash flow, AT&T Inc. retains ample capacity to meet its $45 billion commitment. Goldman Sachs maintains its ‘Buy’ rating, emphasizing that ‘the risk-reward profile remains asymmetrically positive for income-focused portfolios.’

How Do Competitors Compare on Shareholder Returns?

Compared to peers, AT&T Inc. stands out for consistency and scale. Verizon Communications offers a 6.1% yield but has slowed buybacks amid 5G SA rollout costs. T-Mobile US (TMUS) prioritizes growth over returns, with no meaningful buyback program and a yield under 1%. Meanwhile, AT&T Shareholder Returns are backed by a $19 billion 2027 FCF target and a multi-year, board-approved framework — a level of transparency rarely seen outside of Apple or NVIDIA-backed tech giants. For U.S. investors seeking yield without sacrificing capital preservation, AT&T Inc. delivers a rare hybrid: infrastructure stability with optionality.

Related Coverage: For deeper context on recent earnings pressure, read AT&T Earnings -3.2% Plunge: Momentum at Risk?, which analyzes how Q1 2026’s strong results contrast with investor concerns over segment restructuring and integration risks. The article underscores that while earnings momentum remains intact, execution on the $45 billion return plan will be the true catalyst for valuation re-rating.

The best first quarter ever for Advanced Connectivity internet customer net additions.— John Stankey, CEO of AT&T Inc.

AT&T Shareholder Returns are now the centerpiece of the company’s market narrative — and for good reason. With record fiber growth, disciplined capital allocation, and a valuation that prices in worst-case scenarios, AT&T Inc. offers a compelling income-and-upside proposition for U.S. portfolios. The next quarterly earnings report will test whether momentum sustains into Q2 — and whether Wall Street begins repricing the stock toward its $30.25 consensus target. For dividend investors and long-term holders alike, the opportunity is now actionable.