Can the Intel SpaceX Partnership and AI inference boom really justify a 400% stock surge and a rich new valuation?

How is the Intel SpaceX Partnership moving the stock?

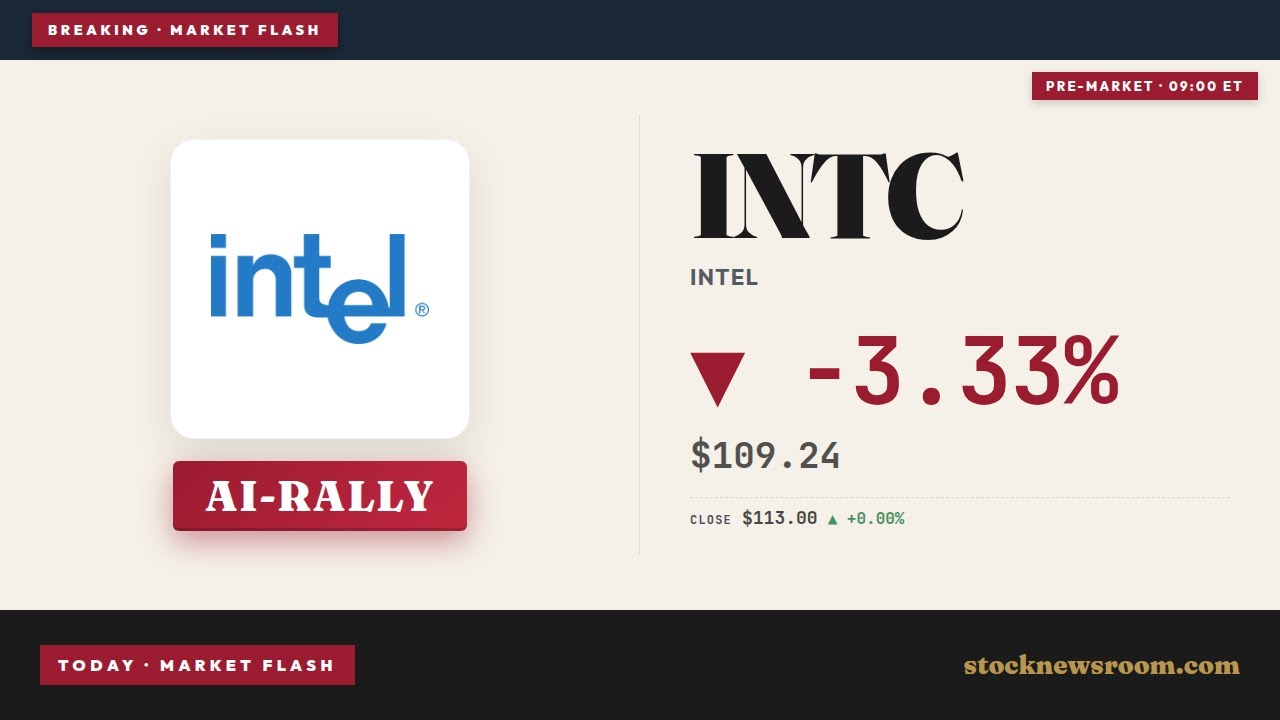

Intel Corporation (INTC) is up about 4.5% to $113.01 compared with Wednesday’s close of $111.01, even as pre-market quotes earlier in the day pointed to some profit-taking near $109.39. The move caps a spectacular run that has seen the stock surge more than 400% over the past year, turning Intel into one of the standout gainers in the S&P 500 and on the NASDAQ. The latest catalyst is the Intel SpaceX Partnership around a massive new chip plant in Texas, which adds another high-profile AI and foundry pillar to the bull case.

Despite the rally, Wall Street is cautious. Jefferies, Mizuho Securities and Robert W. Baird all currently sit at a “Hold” consensus on Intel, with an average price target that implies roughly 20% downside from current levels. That disconnect between a skeptical sell-side and euphoric price action is forcing US investors to ask whether Intel’s AI and Musk-linked projects truly justify the new valuation.

What does the Terafab deal mean for Intel?

At the heart of the Intel SpaceX Partnership is “Terafab,” a planned chip factory in Texas that SpaceX expects will cost an initial $55 billion and could ultimately reach about $119 billion as it scales out. The plant is designed to manufacture computer chips for SpaceX, electric-vehicle maker Tesla, AI developer xAI and other companies within Elon Musk’s empire, aiming to reduce dependence on Asian foundries like TSMC and Samsung.

Intel is contributing its advanced 14A manufacturing technology to Terafab, even though it has not yet deployed that node in its own mainstream production. The arrangement underscores Musk’s need for a US-based, leading-edge manufacturing partner and highlights Washington’s broader push to onshore semiconductor capacity. For Intel, the partnership positions its foundry unit at the center of one of the most ambitious private industrial projects in the country, potentially creating a long-lived, high-volume customer base across rockets, EVs and AI systems.

The Intel SpaceX Partnership also dovetails with Intel’s ongoing foundry reorganization. The company has carved out its manufacturing arm as a more independent operation, freeing capital and management focus to accelerate process development. Management is already ramping its 18A node with back-side power delivery, and internal data suggest usable chip yields are improving by roughly 7% per month. Terafab and 14A extend that roadmap, giving Intel a high-visibility proving ground for its next generation of process technology.

Is AI inference really a turning point for Intel?

Beyond the Intel SpaceX Partnership, Intel’s core AI thesis rests on a structural shift from model training to inference. After years of GPU-heavy build-outs, major cloud providers are now spending more on infrastructure that can run large language models and agentic systems on real-world data in real time. Deloitte expects inference to account for about two-thirds of AI compute by 2026, up from roughly half last year, which favors more balanced architectures anchored by CPUs and custom accelerators.

Intel still controls just over 70% of the server CPU market, and management argues that CPUs are once again becoming the “indispensable foundation” of AI data centers. In many deployments, the GPU-to-CPU ratio is falling toward four-to-one, and complex multi-agent or physical AI systems can approach parity. That shift already shows up in Intel’s data center and AI segment, where revenue grew about 22% at the start of the year.

At the same time, Intel is rapidly scaling its ASIC and custom accelerator business. ASIC revenue nearly doubled year over year in the latest quarter, with sequential growth around 30%, and the business has passed a $1 billion annual run rate. Google’s cloud division has signed a multiyear contract for Intel Xeon CPUs and custom accelerators, while even GPU leader NVIDIA is integrating Intel Xeons into its Rubin rack-scale systems. If inference workloads grow as projected, Intel could capture a larger slice of AI spending than the current market narrative suggests.

How stretched is Intel’s valuation after the rally?

Even Intel bulls concede that the stock is no longer cheap. The shares trade on a sales multiple near 8–9 times, and some market observers flag a headline P/E ratio that has compressed to low single digits mainly because earnings have snapped back from depressed levels. While that rerating reflects genuine progress in AI, foundry and US industrial policy support, it also leaves little room for execution missteps around the Intel SpaceX Partnership, 18A rollout, or upcoming 1.4-nanometer-class process kits that will be showcased at Computex in early June.

For US investors, the risk-reward now hinges on whether Intel can sustain double-digit revenue growth beyond 2026 while lifting margins from the high-30% range into the 40s as scale improves. The foundry unit is still burning cash, and large capex commitments across the US and Europe will pressure free cash flow in the near term. Shorting the stock has proven dangerous in this momentum phase, but new long positions at current levels require conviction that Terafab, AI inference and potential wins with customers like Apple will translate into durable earnings power.

Related Coverage

Investors looking for more detail on Intel’s manufacturing strategy and the role of Terafab can read Intel Foundry +3.9% Surge: Can AI and Terafab Deliver?, which dives deeper into the company’s foundry turnaround and its bets on Apple and other major customers. That analysis complements today’s focus on the Intel SpaceX Partnership by exploring whether Intel’s AI-driven foundry push can support the stock’s dramatic rerating.

In summary, the Intel SpaceX Partnership, rising AI inference demand and a revitalized foundry strategy are transforming Intel into one of Wall Street’s most controversial high-growth semiconductor names. For American portfolios, the stock is now a leveraged bet on US onshoring, Musk’s industrial ambitions and a CPU-centric AI architecture. The next few quarters, including updates on Terafab and Intel’s advanced process nodes, will determine whether today’s premium valuation is the start of a new era or the peak of an AI-driven boom.