Can the new Oracle Defense Contract and booming AI cloud demand finally close the gap between Oracle’s growth and its valuation?

How is the Oracle Defense Contract moving the stock?

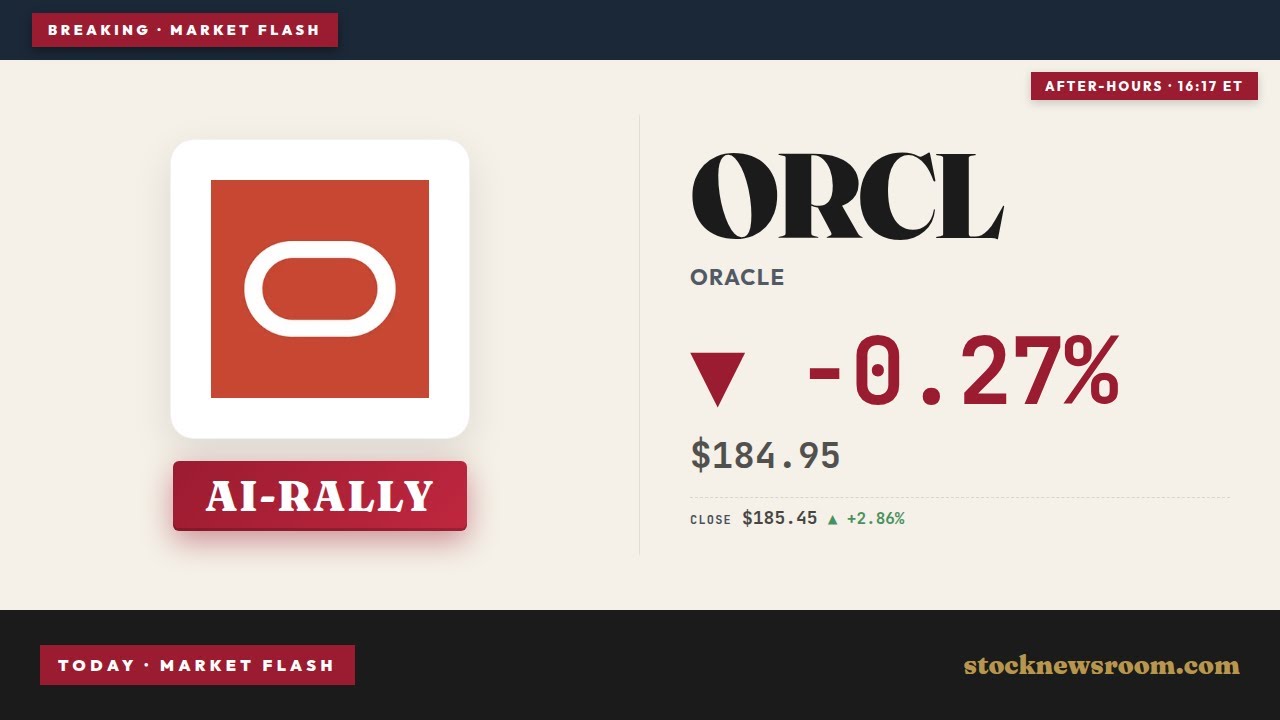

Oracle Corporation shares climbed about 2.9% to $185.46 on Tuesday, after gaining nearly 5% on Monday, putting them roughly 15% higher over the last month but still well below the 52‑week high near $345. The latest leg up follows confirmation that Oracle has secured a classified artificial intelligence deal with the U.S. Department of Defense, widely referred to as the Oracle Defense Contract. The agreement will deploy Oracle’s AI capabilities onto classified networks to support military decision‑making and national security use cases, reinforcing its push into high‑performance government cloud infrastructure.

Traders also pointed to options activity as a sign of heightened positioning. A notable call sweep at the $190 strike expiring May 15 involved 66 contracts and thousands of additional trades at that line, suggesting active hedging or profit‑taking as shares approach technical resistance near $189. Despite a small dip to around $185.35 in the after‑hours session, technical momentum remains constructive with the price well above its 20‑ and 50‑day moving averages, even as it sits below the 200‑day trend line.

Is Oracle now a core AI infrastructure play?

The Oracle Defense Contract lands on top of a broader AI infrastructure boom that is reshaping the company’s profile in the S&P 500 technology cohort. In its fiscal Q3 2026 (ended Feb. 28), Oracle reported 22% total revenue growth to $17.2 billion, driven by a 44% surge in cloud revenue to $8.9 billion. Infrastructure‑as‑a‑service, the segment that rents out raw compute for AI training and inference, grew 84% year over year, with AI‑specific infrastructure revenue up an eye‑catching 243%.

Behind those numbers is a massive contract backlog, or remaining performance obligations (RPO), that has swelled to about $553 billion – more than Oracle’s roughly $525 billion market cap. A cornerstone is the roughly $300 billion, five‑year compute agreement with OpenAI tied to the Stargate joint venture. While some investors worry that OpenAI’s own revenue volatility could ripple back to Oracle, several Wall Street firms, including Wedbush, argue that demand from OpenAI and other hyperscale customers remains robust and that concerns are overdone in the near term.

Oracle’s AI buildout is also rippling into the broader economy. Utilities like DTE Energy are signing multi‑gigawatt data‑center load contracts with Oracle and Google, underpinning multi‑year capital programs in power infrastructure. At the same time, Oracle remains a major customer for AI‑server vendors such as NVIDIA’s ecosystem partners, even as reports of at least one contract loss for Super Micro Computer underscore how fierce the competition for hyperscale AI deployments has become.

How does Oracle stack up against cloud rivals?

From a Wall Street perspective, Oracle’s AI and government‑cloud push is increasingly being compared to heavyweights like Apple’s services engine and the cloud franchises of Amazon, Microsoft and Alphabet. While those peers are hitting fresh highs on the NASDAQ and driving much of the S&P 500’s tech leadership, Oracle’s stock is still down more than 6% year to date, highlighting a disconnect between operating momentum and equity valuation.

Analysts at Morgan Stanley recently lifted their estimate for AI‑related capital expenditures to around $800 billion in 2026 and up to $1.1 trillion in 2027 across Amazon, Microsoft, Meta, Alphabet and Oracle, underscoring the scale of the opportunity. In parallel, MarketBeat highlighted that Oracle has secured roughly $16 billion in financing for a Michigan AI data center and is partnering with Bloom Energy’s Project Jupiter for on‑site fuel cells – steps designed to ensure reliable power and lower long‑term operating costs for energy‑hungry AI campuses.

For investors, the key question is whether Oracle can convert its towering backlog into high‑margin, recurring earnings fast enough to close the performance gap with AI beneficiaries like NVIDIA and Tesla. So far, profitability trends are encouraging: non‑GAAP EPS rose 21% in Q3 to $1.79, cloud infrastructure gross margin hit 32% versus 30% guidance, and management nudged its fiscal 2027 revenue target to $90 billion. Many portfolio managers now see Oracle as a late‑cycle, more value‑oriented way to gain AI exposure compared with premium‑valued chipmakers and megacap cloud leaders.

What are the main risks for Oracle investors?

The bullish case built around the Oracle Defense Contract and AI infrastructure comes with notable risks. Oracle is on track to spend roughly $50 billion in capex in fiscal 2026, more than double the prior year, and is leaning heavily on debt to fund the buildout. Long‑term debt stands around $125 billion, and trailing 12‑month free cash flow has swung deeply negative as the company fronts data‑center investments ahead of associated revenue streams.

While executives emphasize that a substantial portion of capacity is supported by customer prepayments or even customer‑supplied chips, the strategy contrasts with cloud rivals like Amazon and Alphabet, which primarily fund AI investments from internal cash flows. It also differs from chip suppliers such as NVIDIA and Broadcom, which sell into the AI wave without the same balance‑sheet strain. If large anchor customers like OpenAI fail to fully utilize or pay for their contracted capacity, or if government budgets tighten after the initial ramp of the Oracle Defense Contract, Oracle’s leverage could become a bigger overhang.

That said, sentiment is starting to improve. Wedbush recently reiterated an Outperform rating and a $225 price target on the stock, explicitly pushing back against fears that growth is slowing or that OpenAI’s challenges will derail backlog conversion. Other bullish voices highlight that Oracle has already secured around $30 billion in external funding and $29 billion in customer‑prepaid contracts tied to the AI buildout, which partially de‑risks future cash flows.

Related Coverage

Investors looking for a deeper dive into the Pentagon opportunity can revisit our earlier analysis, “Oracle Defense Deal +6.2% Surge: Pentagon Win Shocks Wall Street”, which explores how classified AI workloads could reshape Oracle’s competitive position in the cloud wars and what the initial stock reaction revealed about positioning on Wall Street.

Overall, the Oracle Defense Contract crystallizes Oracle’s shift from legacy database champion to critical AI and government‑cloud infrastructure provider, even as heavy leverage and customer concentration keep risk high. For U.S. and global investors seeking diversified AI exposure beyond the usual mega‑cap leaders, Oracle now offers a blend of growth and value that hinges on successful execution of its record backlog. The next few quarters – including further updates on OpenAI demand, hyperscaler capex and follow‑on government awards – will determine whether the Oracle Defense Contract becomes a durable catalyst for long‑term outperformance.