Are Rocket Lab Earnings strong enough to justify a soaring valuation even as the stock suddenly drops nearly 10%?

How are Rocket Lab Earnings reshaping the story?

Q1 2026 Rocket Lab Earnings marked a clear inflection point in the company’s business mix and growth narrative. The company posted revenue of about $200.35 million, roughly 5% above consensus estimates near $189.7 million and more than 60% higher year over year. Adjusted EPS came in at −$0.07, matching Wall Street expectations and underscoring that profitability remains a medium‑term goal rather than an immediate reality.

The key headline inside these Rocket Lab Earnings is the dominance of the Space Systems segment. Space Systems generated roughly $136.7 million in Q1 revenue, while Launch Services contributed about $63.7 million. For a company long viewed as a small‑satellite launch specialist, the fact that scalable components like reaction wheels, power systems, propulsion and optical communications now drive the majority of revenue is a structural shift that matters for valuation and risk.

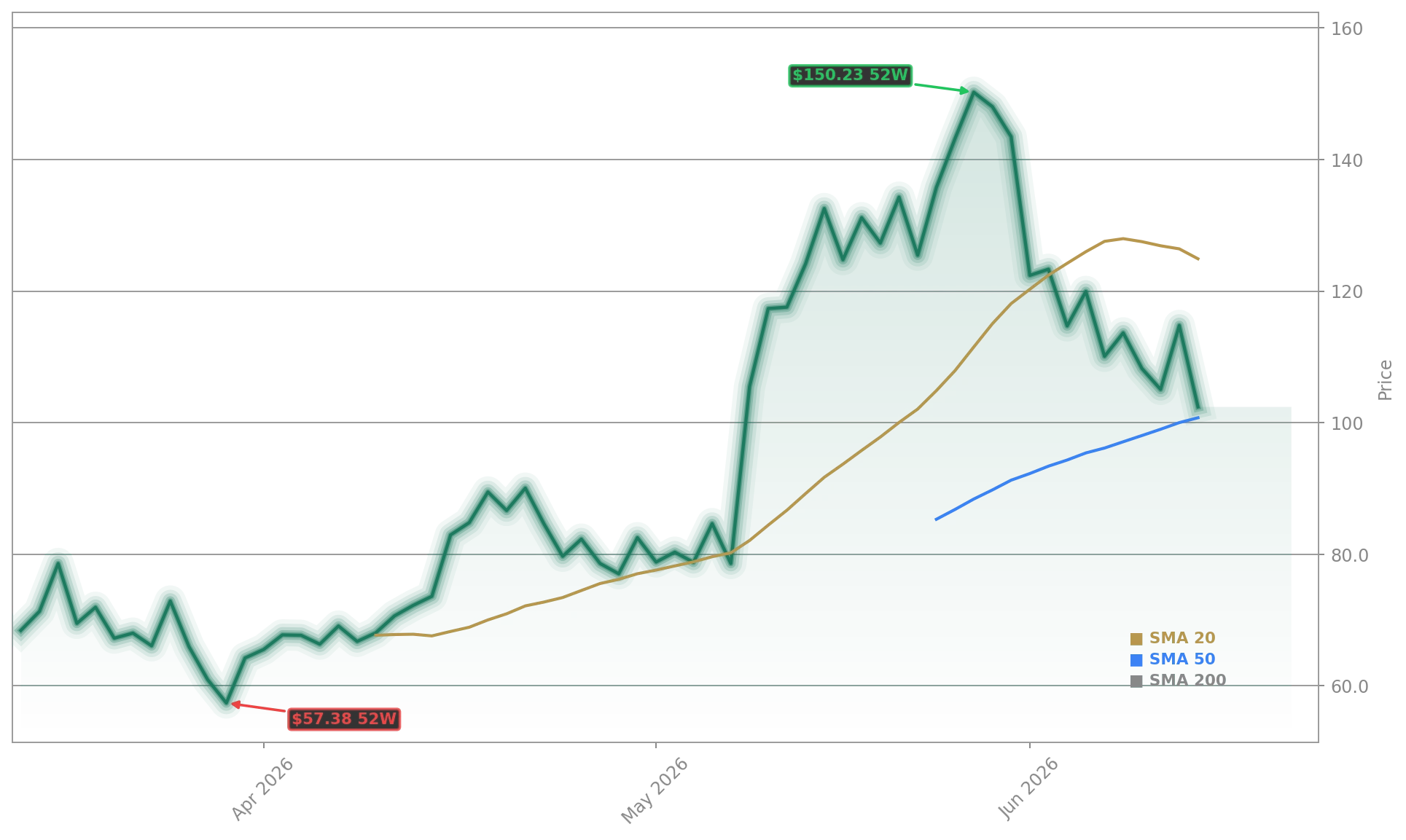

Management also highlighted a record $2.2 billion backlog and access to more than $2 billion in liquidity, giving Rocket Lab room to fund R&D on the Neutron heavy‑lift rocket and pursue selective M&A. Still, with the stock recently hitting an all‑time high of $136.45 and today’s market value above $70 billion, investors are increasingly focused on whether this level of growth can be sustained without repeated capital raises or execution missteps.

Why is Space Systems now the growth engine?

The pivot toward a vertically integrated space and defense platform is central to interpreting these Rocket Lab Earnings. Space Systems products — satellite buses, solar arrays, avionics, propulsion and related technologies — are inherently more scalable than launch capacity, which is constrained by infrastructure, cadence and regulatory oversight. This is where Rocket Lab is trying to follow the high‑margin playbooks of companies like NVIDIA and Apple, which dominate critical parts of their ecosystems rather than competing purely on hardware volume.

Recent strategic acquisitions, including the purchase of Motiv Space Systems, deepen Rocket Lab’s capabilities in robotics and satellite subsystems. At the same time, new defense and hypersonic test contracts, along with work on missile warning architectures tied to Washington’s so‑called “Golden Dome” strategy, are pulling the company further into the defense budget stream. Visits from U.S. Space Force officials and fresh hypersonic launch awards underscore that this is not just a commercial satellite bet; it is increasingly a national security contractor story as well.

Sector tailwinds help. Anticipation of an eventual SpaceX IPO and rising investor appetite for space infrastructure have lifted comparable names and contributed to RKLB’s sharp rerating. A 12‑month gain north of 400% and annualized volatility around 125% show how quickly sentiment has shifted — and how violent any future corrections could be if growth stalls or Neutron slips.

How are analysts reacting to Rocket Lab Earnings?

The bullish response from Wall Street research desks has reinforced the earnings‑driven narrative. Deutsche Bank recently raised its price target on RKLB from $73 to $120 while maintaining a Buy rating, citing strengthening demand trends across both launch and space systems. The new target sits just above today’s intraday price, signaling that at least one large bank believes fair value is now in sight after the blistering rally.

Clear Street also boosted its target, moving from $88 to $98 with a Buy rating and emphasizing “record Q1 revenue” plus momentum in the Neutron program and the expanding backlog. Some quantitative platforms, meanwhile, flag RKLB as potentially overbought and richly valued relative to current cash flows, a view echoed by skeptics worried about ongoing losses, dilution risk and the capital intensity of Neutron.

Insider activity is another stress point for some investors. A director‑linked entity recently sold about 100,000 shares in open‑market transactions worth roughly $11.8 million, while donating 10,000 shares to charity. While not unusual after such a steep run, these sales add fuel to the debate over whether management and early backers are taking advantage of exuberant pricing.

What do Rocket Lab Earnings mean for US investors?

For American growth investors comparing RKLB with other high‑beta innovators like Tesla or leading AI beneficiaries such as NVIDIA, the message from recent Rocket Lab Earnings is mixed but powerful. On the positive side, Rocket Lab combines rapid top‑line expansion, diversification away from binary launch risk and growing exposure to defense budgets — a combination that many NASDAQ names cannot match. The record backlog and upcoming missions, including an Electron launch for Synspective and a NASA‑backed cryogenic fuel storage test, provide visible catalysts into 2026 and beyond.

On the risk side, RKLB is not yet profitable, trades at a premium multiple versus many space peers and faces execution risk on Neutron, where delays or cost overruns could hit sentiment hard. Compared with mega‑cap platforms like Apple or software‑heavy AI plays, Rocket Lab sits much higher on the risk spectrum, closer to an early‑stage defense contractor than a mature tech bellwether.

Portfolio construction therefore matters. For investors heavily exposed to cyclical or value segments of the S&P 500, a small RKLB allocation can add uncorrelated growth and space‑defense upside. For traders already concentrated in speculative tech, today’s 9% intraday drop from a recent peak may be less of a screaming bargain and more of a reminder that volatility cuts both ways.

Related coverage: Is the space boom just starting?

Investors looking to place today’s Rocket Lab Earnings in a broader context may want to revisit the recent analysis “Rocket Lab SpaceX IPO: +1.8% Surge as Hype Meets Growth”. That piece, available at Rocket Lab SpaceX IPO: +1.8% Surge as Hype Meets Growth, explores how speculation around a future SpaceX listing is feeding into RKLB’s valuation and what that might mean for the next phase of the space cycle. Taken together, the IPO hype and the latest quarterly numbers frame Rocket Lab as one of the key public proxies for investors who want exposure to the emerging new‑space ecosystem without waiting for private giants to hit the NASDAQ.

In summary, the latest Rocket Lab Earnings confirm that Space Systems has overtaken launch as the primary growth engine while the backlog, liquidity and analyst upgrades support the long‑term bull case. For US investors, RKLB offers a high‑risk, high‑reward way to play the convergence of commercial space and defense at a time when Wall Street is actively hunting for the next structural growth story. The next few quarters — especially milestones on Neutron and additional defense wins — will show whether today’s valuation and volatility are a launchpad for further gains or a ceiling for this phase of the rally.