Is Shopify’s latest pullback a warning sign, or the kind of setup bullish investors wait for before earnings?

Why Is Shopify Forecast Turning Bullish Now?

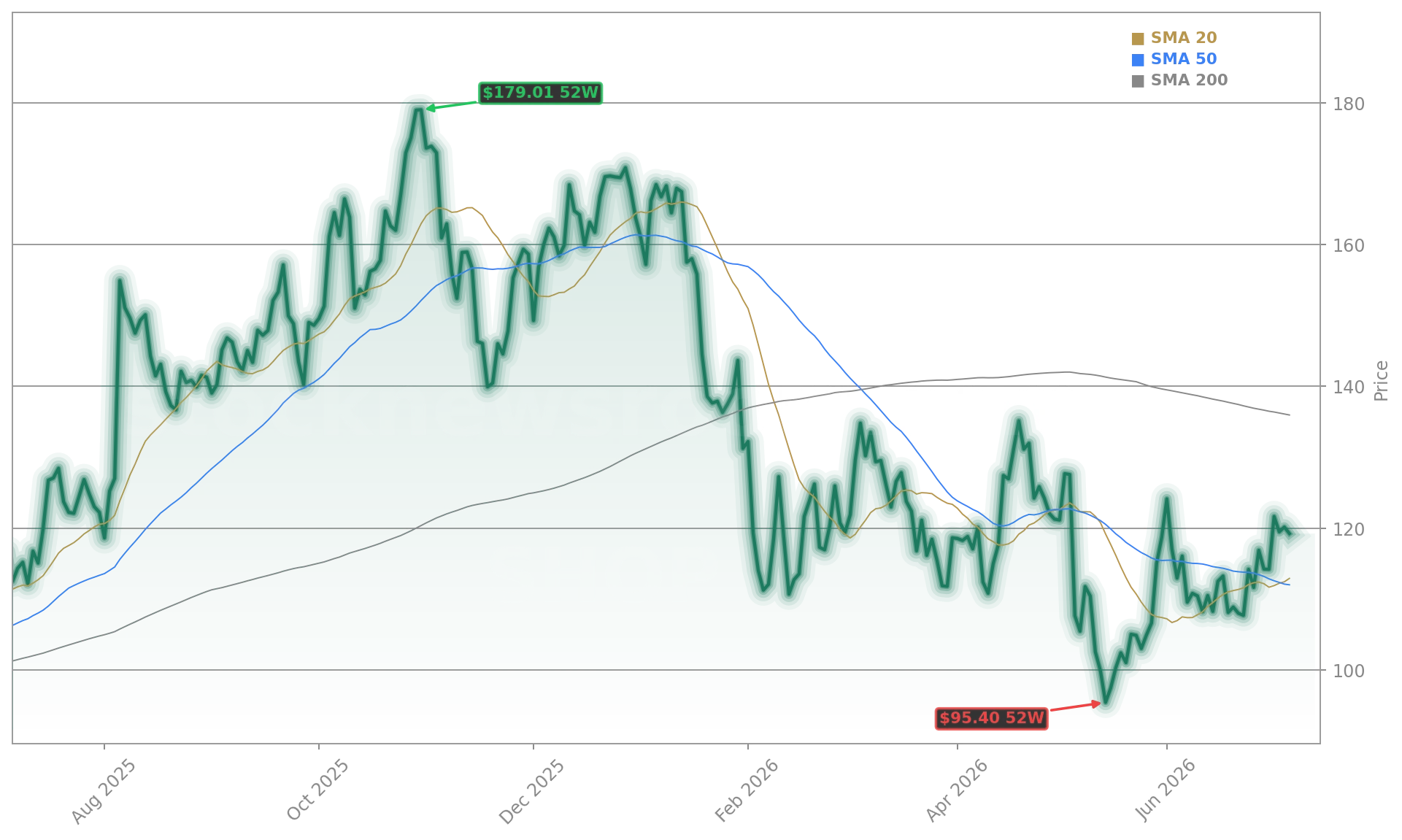

After a challenging first half — marked by a copyright settlement and a brief administrative outage — Shopify Inc. is regaining Wall Street’s confidence. CIBC’s Todd Coupland notes that Q2 2026 presents a “beatable bar,” with positive trends across payments volume, new merchant acquisition, European growth, and alternative data confirming strength. Shopify Plus traffic surged 28% year over year, outpacing last quarter’s 20% gain and aligning closely with FactSet’s gross merchandise volume (GMV) expectation of +28% YoY. That momentum, Coupland argues, signals upside potential ahead of the July earnings print — especially as AI integration begins delivering tangible transaction-layer leverage. The stock’s 5% decline Wednesday to $117.83 reflects broader tech volatility, not deteriorating fundamentals.

How Does Shopify Forecast Compare to Amazon and Peers?

While Amazon.com remains the e-commerce revenue titan — reporting $181.5 billion in Q1 2026 versus Shopify Inc.’s $3.2 billion — the Shopify Forecast emphasizes divergent growth vectors. Shopify’s 34% YoY revenue growth in Q1 2026 dwarfs Amazon’s 17%, underscoring its higher-beta positioning in the SMB and mid-market segments. Crucially, Shopify’s focus on AI-native infrastructure — rather than building foundational models like Amazon — positions it as a beneficiary, not a casualty, of agentic commerce. Bank of America explicitly refutes fears of disintermediation, stating, “Shopify could be a core beneficiary of the shift toward AI-driven, agentic commerce.” Its valuation premium (13x price-to-sales vs. Amazon’s 4x) reflects that strategic optionality — and growing investor comfort with its path to margin expansion.

What’s Driving the Shopify Forecast Upside?

Three structural catalysts anchor the improved Shopify Forecast: international scale, enterprise adoption, and partner-led upmarket expansion. International GMV grew 45% YoY in Q1 2026, while non-U.S. payments volume jumped over 70%. Non-U.S. revenue now accounts for 37% of total revenue — a key diversification win. Meanwhile, Shopify Plus revenue rose 20% YoY, with merchants exceeding $25 million in GMV growing fastest. Deutsche Bank calls Shopify’s new partner model — launched in late 2025 and refined this quarter — a “modest positive,” offering agencies stronger economic incentives to onboard and retain complex, high-GMV merchants across Plus, POS, and B2B use cases. Early feedback is positive, and Deutsche Bank expects any incremental sales and marketing spend to be more than offset by GMV and revenue gains.

Is the Shopify Forecast Sustainable Through 2027?

Bank of America’s long-term Shopify Forecast projects 24%–28% revenue growth from fiscal 2026 through fiscal 2028, with gross margins holding in the mid-to-high 40% range. Operating margins are forecast to expand from 17.1% in 2025 to 20.5% in 2028, while free cash flow margins rise from 17.4% to 20.3%. The $150 price target rests on a 22x EV-to-gross-profit multiple — above the peer average of 18.1x — justified by superior growth, margin trajectory, and infrastructure moat. That outlook gains credibility as Shopify’s payments business — now responsible for 68% of total GMV — deepens its role as a fintech enabler. Investors should watch how this evolves alongside broader AI infrastructure plays like NVIDIA and Apple, where AI-driven commerce stacks increasingly converge.

We believe Shopify could be a core beneficiary of the shift toward AI-driven, agentic commerce rather than being disintermediated by it.— Bank of America

Related coverage: Shopify Payments Strategy: 68% of Volume Fuels Fintech Push explores how its payments dominance strengthens its transaction-layer defensibility — a core pillar of the Shopify Forecast. Meanwhile, NVIDIA China +4% Surge as H200 News and BofA Lift Sentiment underscores how AI hardware momentum supports the broader ecosystem in which Shopify’s agentic commerce vision operates.