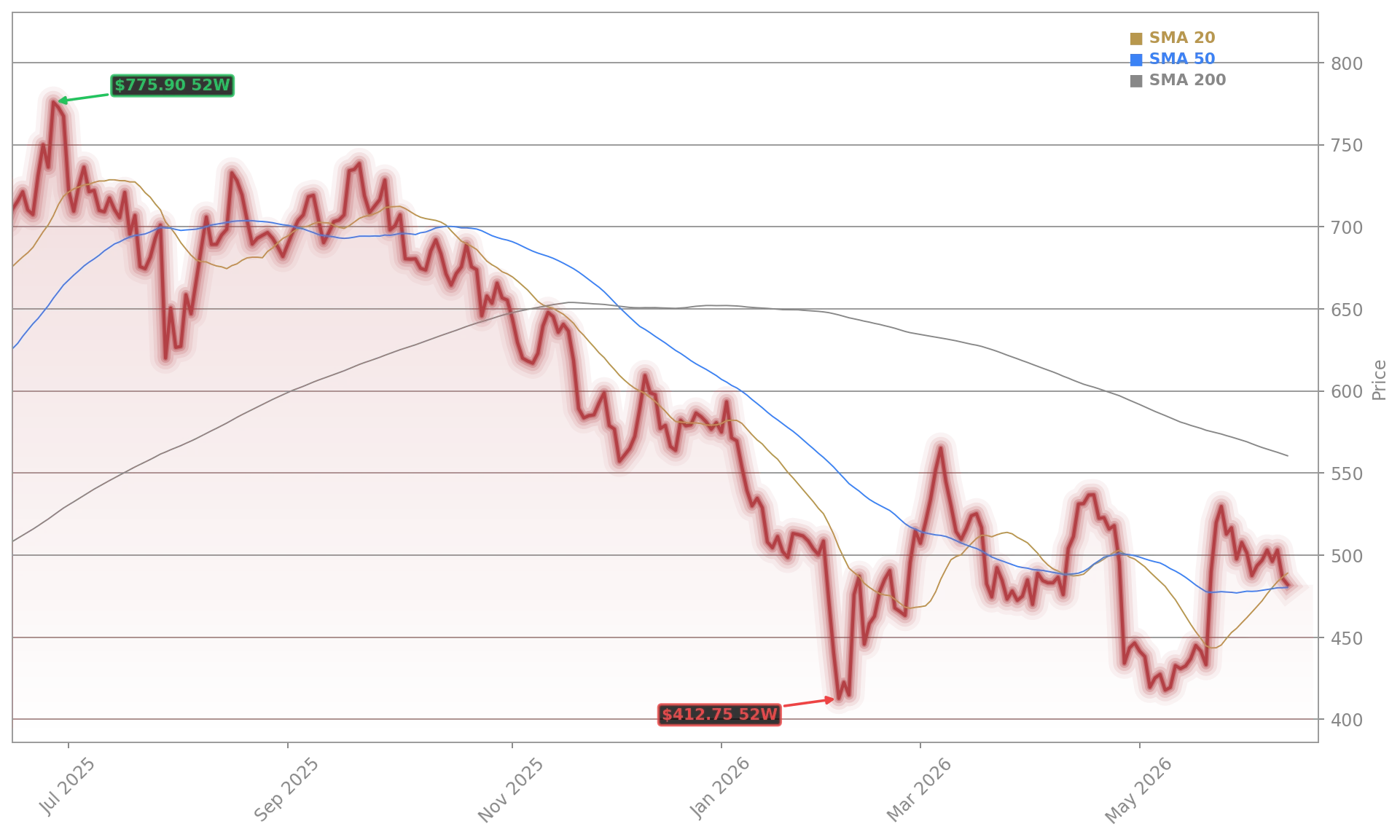

Can Spotify’s AI push and billion-user ambition finally convince investors that the streaming giant deserves a much higher valuation?

Why is Spotify AI Strategy driving shares?

Spotify Technology S.A. told investors it wants to reach 1 billion subscribers and $100 billion in revenue by 2030, while lifting gross margins from roughly 30% toward 35% to 40%. That long-range framework landed well with investors because it paired ambitious top-line targets with clearer monetization levers. The stock had already surged after Investor Day, and Friday’s move kept momentum alive as investors reassessed whether Spotify deserves a richer valuation multiple.

The new product slate was central to that reaction. Management introduced an AI remix offering developed with Apple Music rival Universal Music Group, a personalized AI podcast concept, and a superfan ticket reservation program called Reserved in partnership with Live Nation. Together, those initiatives suggest Spotify wants to become more than a streaming utility. It is aiming to be a discovery, fandom, and commerce platform across music, podcasts, and live events.

How is Spotify positioning against Apple?

For US investors, the competitive angle matters. Spotify has long battled Apple in subscription audio while also competing for attention with Amazon, Alphabet, and social platforms such as ByteDance. The Spotify AI Strategy is meant to answer a key market concern: that generative AI could weaken the value of music platforms by making content and recommendation tools more interchangeable. Instead, Spotify argues its proprietary taste graph, user history, and daily engagement signals can turn AI into a retention and monetization advantage.

That thesis gained support from fresh analyst commentary. Citizens raised its price target to $625 from $600 and kept a Market Outperform rating, highlighting Spotify’s expanding AI product set and its data advantage. Barclays reiterated an Overweight rating ahead of Investor Day with a $500 price target, stressing that management needed to articulate a credible AI monetization plan. Guggenheim also reiterated Buy with a $565 target before the event, focused on margin progress and updated long-term targets.

Can Spotify revive podcasts with profit?

Podcasting remains a key test. Spotify spent heavily to build the business, acquiring Gimlet and Parcast in 2019 as part of a roughly $1 billion push into the category. That expansion helped expose podcasting to millions of mainstream listeners, but it also created cost pressure and a later retrenchment as several in-house shows and studios were cut. The company has since shifted away from a pure studio model toward a more flexible mix of licensed content, creator tools, advertising, and personality-led formats.

Now management appears to be framing podcasts as part of a broader monetizable ecosystem rather than a stand-alone content gamble. The Spotify AI Strategy fits that reset by using personalization and automation to deepen engagement instead of simply adding more expensive originals. Combined with audiobooks and music tools, the bet is that cross-format listening can improve lifetime value and ad yield.

Related Coverage: Investors still remember how quickly sentiment swung after first-quarter guidance rattled confidence last month. Our earlier report, Spotify Earnings: -4.3% Plunge as Q2 Outlook Shocks Investors, examined why record results were overshadowed by a softer near-term outlook and why management’s long-term narrative suddenly became so important for the stock.

Those were the heady times for Spotify as it bulled and bullied its way into podcasting.— George Witt

The bigger picture is that Spotify is asking Wall Street to value it less like a mature streaming app and more like a scaled audio platform with multiple monetization engines. If execution matches the presentation, the Spotify AI Strategy could become the bridge between strong engagement metrics and a more durable premium valuation. The next milestones for investors are product rollout, margin follow-through, and proof that AI can lift growth without undermining the user experience.